3M (NYSE: MMM) announced results that severely missed expectations.

Revenue came in at $8.11 billion, a slight miss to consensus of $8.12 billion while earnings per share of $1.66 missed the consensus estimate of $2.10 by 21% and were down 27% from the same quarter in 2018.

If a litigation charge of $0.29 and costs from the Acelity acquisition are removed, EPS of $2.16 ended up beating estimates by 3%.

The litigation charge is concerning as it demonstrates potential larger hidden costs from the cleanup of previously contaminated manufacturing sights.

Management as usual calls this charge one-time, but we see risks these lawsuit charges continue, dragging down earnings and cashflow.

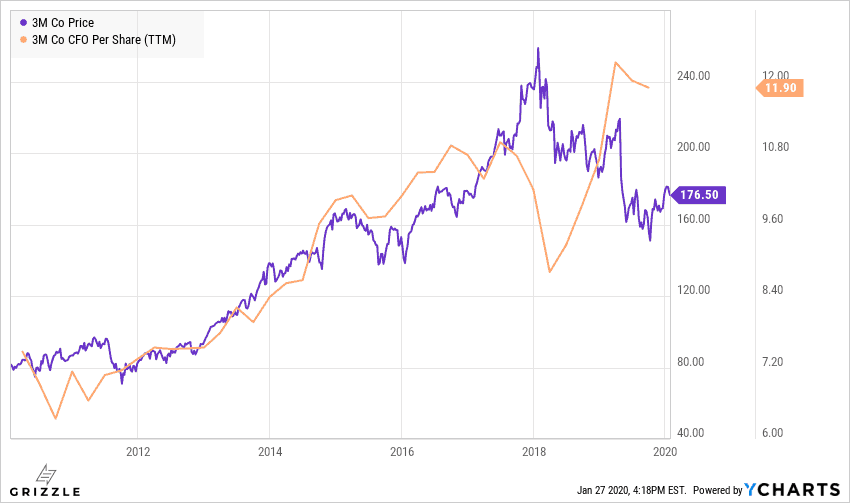

Overall the company still put up strong cashflow numbers. Cashflow was $2.3 billion in the quarter, an increase from $2 billion last quarter and $2 billion a year ago.

[su_panel background=”#ebebec” color=”#05011c” border=”px none ” shadow=”px px px ” radius=”4″ text_align=”center” class=”dw-editor-note”]If management can keep cutting costs in line with the revenue declines, investors are looking at a solid yield and cashflow returns for years to come, even taking into account topline weakness. The stock still looks like a buy. [/su_panel]

Operational Review

Management also committed to an accelerated restructuring timeline that cost $134 million in the quarter but will save $45 million in 2020 and $115 million a year thereafter.

2020 guidance of $9.30 to $9.75 was released as well, which is 1% below where consensus was as of yesterday.

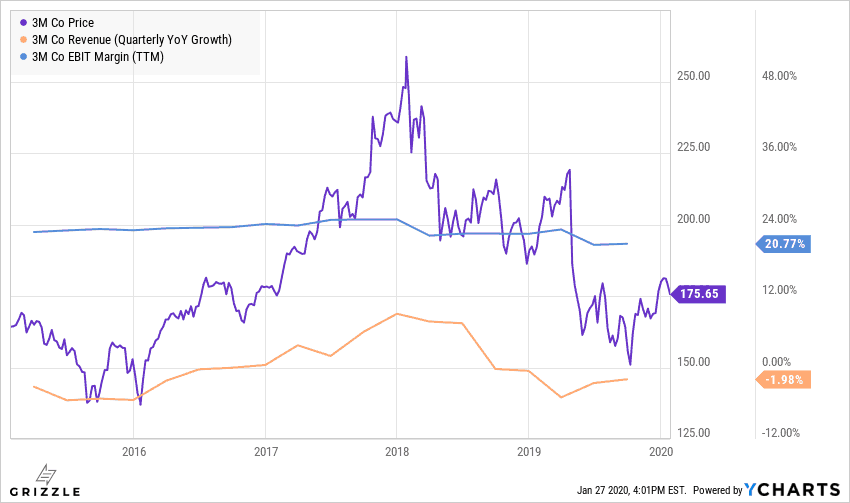

3M continues to suffer from declining sales which are dragging down overall results, but management is laser-focused on maintaining a healthy free cash flow level to support the dividend they are known for.

Sales in Asia continued to drag down results declining 2.9% this quarter driven by Japan. The U.S. was also a weak spot this quarter declining 2.9% from last year.

From a business line perspective, results were dragged down by the Transportation and electronics segment.

3M Revenue Growth and Margins Weakening

But Cashflow Per Share Still Going Up

What to Do with the Stock

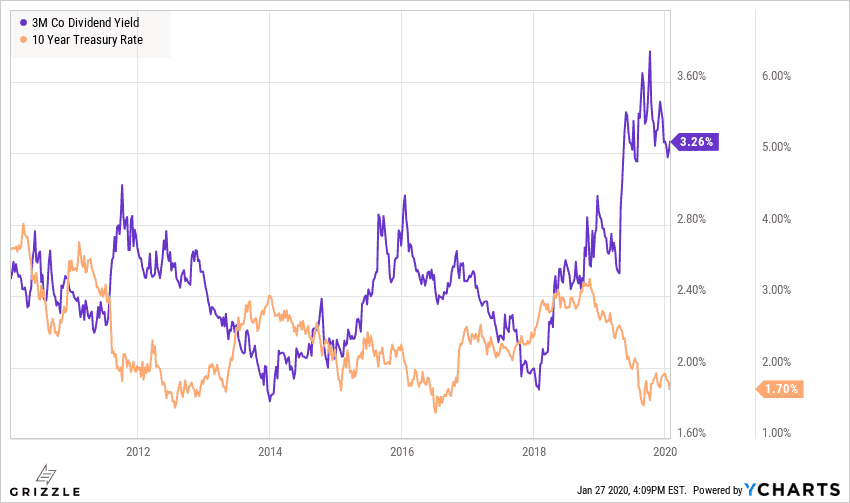

After a weak stock performance in 2019, 3M is yielding 3.3% which is the highest stock yield in 10 years.

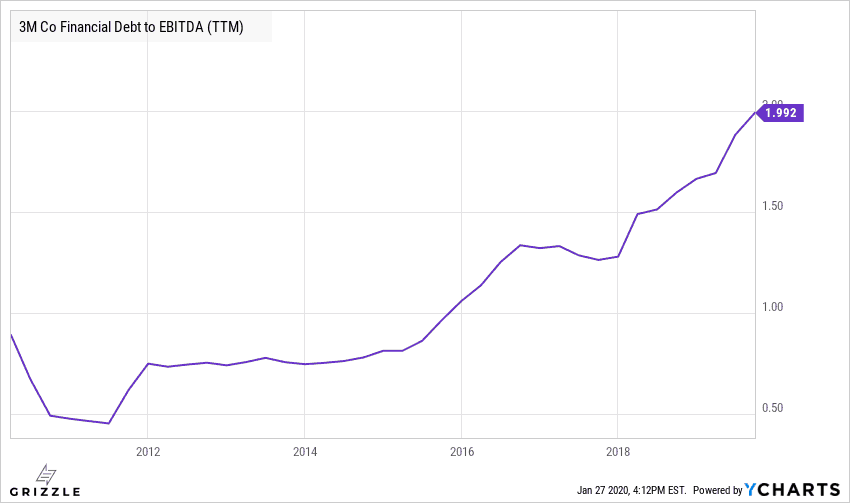

Yes, the debt is higher than normal due to the Acelity acquisition, but management is already restructuring to increase cashflow so they can pay down the debt back to the historical average over time.

Debt/EBITDA Higher than Usual

The higher than average dividend yield shows investors are more worried than usual, but fear creates opportunity.

If you believe the recent Acelity acquisition will pay off, the stock is looking like a bargain.

3M has been one of the most consistent and profitable companies in the stock market and short-term weakness in certain businesses is creating what looks like a buying opportunity.

Dividend Yield at 10-year High and Record Premium vs Treasuries

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.