In the “big picture” this writer continues to believe that central banks are becoming less important in the G7 world because the political reality is that they will not be able to tighten meaningfully if the return of inflationary pressures prove less transitory than still assumed by the Federal Reserve and many others.

Investors should never forget that the overwhelming empirical evidence remains that, at almost the first sign of risk-off action in the financial markets, the Fed’s so-called “hawks” usually turn silent.

Indeed the whole reason Fed governors have been able to engage in a somewhat academic debate in recent months about the merits of an earlier than previously expected tapering process is precisely because the stock market has been so calm.

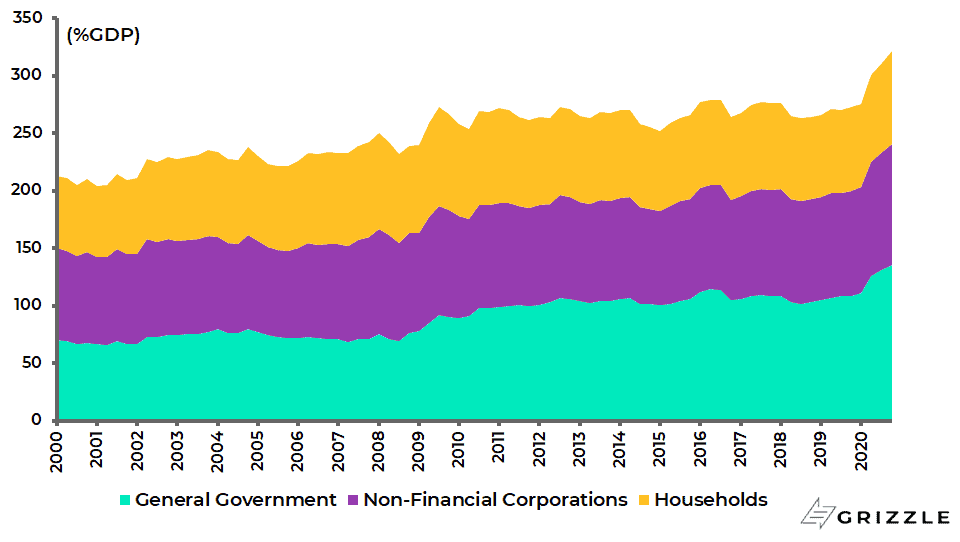

Neither Government’s or Corporations Can Afford Higher Interest Rates

Meanwhile, if it becomes clear in coming quarters that inflationary pressures are more entrenched than assumed, and only the passage of time can resolve this argument definitively, this writer would still expect the political pressures to lead to a practical severing of the link between interest rates and inflation in the G7 world via the introduction of a more formalised regime of financial repression, be it via yield curve control or some other mechanism.

Developed countries’ non-financial sector debt rose from 273% of GDP at the end of 2019 to 321% of GDP at the end of 2020, with government debt, household debt and corporate debt at 136%, 81% and 104% respectively.

Developed countries’ non-financial sector debt to GDP

But another reason is clearly the impact of higher bond yields on government budgets given the fiscal largesse triggered by the pandemic.

For it is evident that an enduring consequence of the pandemic will be a much greater tolerance in the G7 world for fiscal activism targeting politically fashionable causes.

In this respect, markets will again be focusing in coming weeks on the size of the Biden administration’s proposed fiscal stimulus.

This situation has been complicated by the machinations of Congressional politics, a legislative process which has been also exacerbated by the internal ideological divide within the Democratic Party.

Exploring the Politics behind $4.5 Trillion of Spending

The Senate passed the so-called US$1tn bipartisan infrastructure bill on 10 August.

The key question now is whether the House of Representatives will pass this bill since the position of House Speaker Nancy Pelosi from the outset has been that she will not pass it until after the so-called reconciliation bill is passed for the US$3.5tn “American Jobs Plan” pushed for by the likes of Democrat Senators Chuck Schumer and Bernie Sanders as well as their counterparts in the House.

It should be noted that the reconciliation process is a way to fast-track a bill related to spending and taxes.

This is because a reconciliation bill can be passed with a simple majority rather than the 60 votes normally required in the Senate.

This clearly matters given the Democrats’ extremely marginal control of the Senate.

The Democrats currently have only 50 seats in the 100-member Senate, though Democratic Vice President Kamala Harris can break a tie, giving the party a majority.

There is then potentially US$4.5tn of additional fiscal stimulus in the works with the US$3.5tn American Jobs Plan massively more consequential financially and politically, in terms of both a dramatic increase in the size of the deficit as well as in the role of government, than the just passed bipartisan bill in the Senate.

This is because the latter focuses primarily on physical infrastructure whereas the former is much more about so called “human infrastructure” or what Europeans would describe as an expansion of the welfare state.

This is also where politics comes in.

Nine moderate Democrat members of the House sent a letter to Pelosi last month stating that they would not vote for the budget resolution until after the House approves the bipartisan infrastructure bill.

Pelosi responded by saying that she would now look to move the two legislative proposals forward concurrently which should be interpreted as a way of keeping her options open or what the Wall Street Journal described at the time as an effort “to balance the demands of her party’s ideological factions” (see Wall Street Journal article: “Pelosi Shifts Her Stance on Bills’ Timing”, 16 August 2021).

Clearly, the progressive wing of the Democratic Party, which is well represented in the House, wants to get all of its US$3.5tn programme on the statute books as soon as possible and certainly before the Democrats potentially risk losing control of the Congress in the mid-term elections in November 2022.

It should also be noted that, with a relatively slim majority (220-212) in the House, the Democrats can afford no more than three defections on legislation opposed by all Republicans.

All of the above will probably not be decided until well into the fourth quarter of this year.

The Stimulus Outcome is More Important for Markets Than When the Fed Will Raise Rates

There are also the additional complications of a potential government shutdown and breach of the government debt limit to add to the noise coming out of Washington in coming months.

One point is clear.

That is whether Washington passes all of this US$4.5tn of stimulus, or a much more watered-down version, is much more consequential than the exact timing of Fed tapering, assuming any tapering happens at all.

The current consensus is back to where it was at the start of the year.

That is a tapering announcement at the FOMC meeting in November with gradual balance sheet reduction expected to commence at the start of 2022.

Meanwhile, the passing of such a scale of stimulus will then cause attention to focus on how such spending will be financed, at which point pressure will rise on the Fed to play its part in the funding.

As to how big the eventual stimulus turns out to be, the key variable will probably be the swing votes of a handful of moderate Democrats in the Senate.

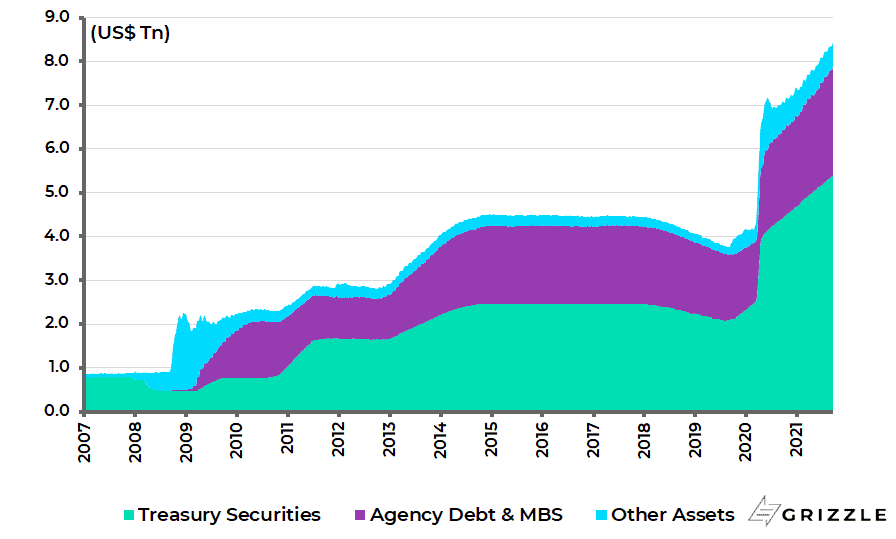

Federal Reserve Balance Sheet

The views expressed in Chris Wood’s column on Grizzle reflect Chris Wood’s personal opinion only, and they have not been reviewed or endorsed by Jefferies. The information in the column has not been reviewed or verified by Jefferies. None of Jefferies, its affiliates or employees, directors or officers shall have any liability whatsoever in connection with the content published on this website.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.