Note: Grizzle subscribers get access to our full Casper IPO guide starting next week. Signup is free and gives you access to all of Grizzle’s best ideas and private weekly strategy email.

–

Fact 1: Casper’s Growth is Slowing

Casper (NASDAQ: CSPR) was one of the first, if not the first, online mattress companies to make a splash in cities across America.

I still remember seeing the company’s ads on the New York subway and wondering if the mattresses were actually that comfortable at such a great price point.

Fast forward to 2019 and the market is getting very crowded.

CNBC estimates there are over 150 online mattress sellers and most of them use the same few manufacturers.

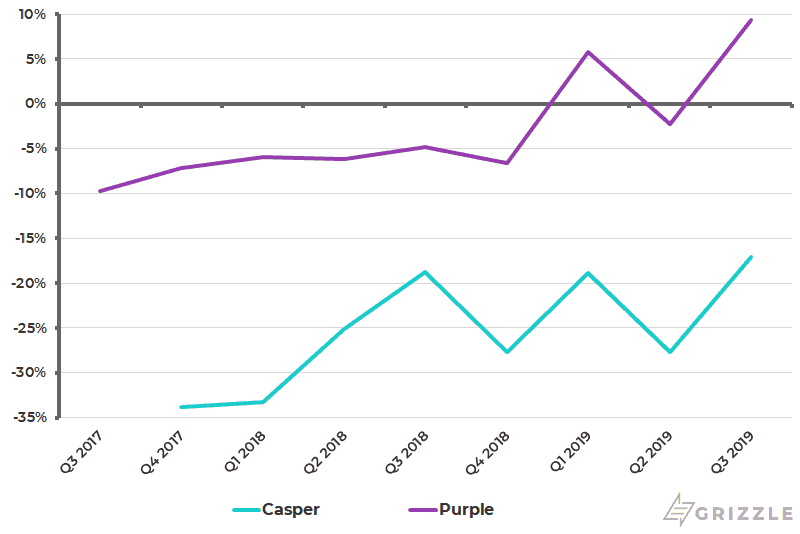

As a result of an increasingly competitive landscape and the company’s decision to raise prices, Casper’s once breakneck growth is slowing.

The company grew revenue by 48% in 2018, but growth has slowed to only 20% in the last nine months.

Online sales are growing less than that at 14%, while the in-store and wholesale channel is picking up the slack growing 65%.

Selling directly to consumers from your own website looks like a mature business especially with all the new competitors entering the field.

Online Sales Growth Falling but Wholesale Picking up the Slack

While Purple has seen exploding sales through Amazon, and other 3rd parties, Casper’s sales in the wholesale channel have been growing much more slowly.

Casper chose to open its own stores instead of going all-in on distributors and this decision is why revenue growth is slower than Purple.

Competition is fierce and revenue growth should continue to fall but Casper could reignite growth if it wanted to by partnering with more distributors and wholesalers.

But at the end of the day if the mattress industry is only growing at 3.5% and competition is increasing, it will be hard for Casper and peers to maintain 20%+ revenue growth for long.

We have likely seen peak growth for Casper.

U.S. Mattress Market Growing at only 3.6%

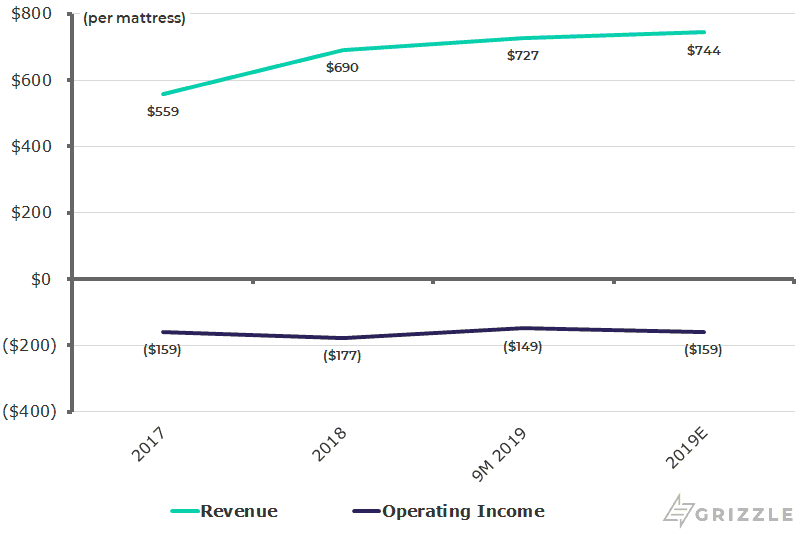

Fact 2: Casper Currently Loses $150 on every Mattress Sold

Casper operates a business model that requires big ongoing marketing spending to keep sales growing.

80% of revenue still comes direct from the Casper website so Casper has to play the search engine game on Google to win over customers.

On top of marketing, the company is investing to build physical stores and ramping up the headcount, all adding up to a big cash burn.

In the nine months ended September 2019, Casper made $727 selling a mattress, but ended up losing $150 when all of its costs were taken into account.

[su_panel background=”#ebebec” color=”#05011c” border=”px none ” shadow=”px px px ” radius=”4″ text_align=”center” class=”dw-editor-note”]Even though the company has raised prices by 22% in the last two years, it still is losing just as much money. This raises questions about the company’s ability to scale and eventually generate a profit. [/su_panel]Per Mattress Economics of Casper

Looking at Casper vs its public competitor Purple, both companies generate the same level of sales but Casper has a far inferior margin profile.

Casper will have to find ways to sell more mattresses with fewer resources if it wants to have any chance of matching the profitability of Purple.

Operating Margin (Casper vs Purple)

Fact 3: The Company Needs Money

There are two obvious reasons why Casper chose early 2020 to go public.

- The company needs money

- Early investors want their payday

As of Sept. 30, Casper had $55 million of cash against annual spending of $90 million or about 7 months of cash left.

7 months is not a long runway and management was probably under pressure to either raise more money privately or go public to raise the needed cash.

This is where reason #2 comes in.

Early investors in the company’s 2014 and 2015 equity financings are now on year 4-5 of their investment.

This is the typical timeline when venture capital firms expect to cash out of an investment.

Casper could have found new private investors to keep the lights on, but management is likely being pressured by the board, which includes early investors, to go public so they have an option to sell out.

With a relatively healthy IPO market, a growth rate that is only going to go down and an uncertain road to profitability, Casper stakeholders are thinking now is the time to cash out.

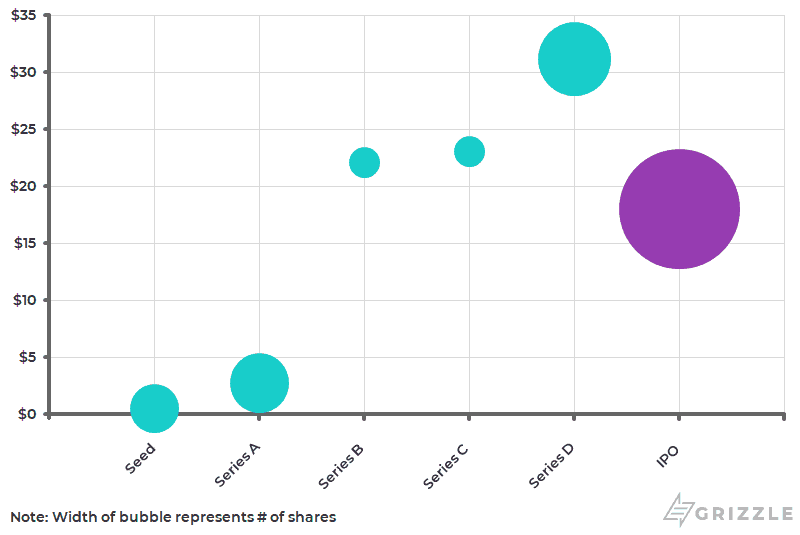

Fact 4: Insiders Bought Their Stock for $17.75 on Average

Understanding the size of gains insiders are sitting on is very important to forecast how strong their motivation to sell may be depending on how the stock trades in the first few months as a public company.

Unlike most of the recent IPOs we’ve reviewed, Casper shareholders are not sitting on meaningful gains.

The average price a current investor paid for their shares is $17.75, compared to the planned IPO midpoint of $18.00/sh.

20% of shares do have a cost basis below $3.00 for gains of 500%, but most investors who put money in are either sitting on losses or meaningless gains.

Even though some investors would take a loss by selling, there are many motivations that go into the decision to hold or sell IPO stock.

All else equal, the closer the IPO price is to the average cost basis of insiders, the less selling pressure there will be once the share lockup expires.

Cost Basis of Current Casper Investors

Fact 5: Competitor Purple’s Stock Fell 50% in the 6 Months After Going Public

The history of Casper’s only other publicly traded mattress competitor should give any investor pause.

Purple Innovations went public in early 2018 through a reverse merger of a publicly-traded shell company.

The deal originally valued Purple at $690 million, but things took a turn quickly.

Even with skyrocketing revenue, Purple’s market value fell over the next year, falling 60% before bottoming at $255 million.

The company’s share price has since been on the rise as Purple managed to turn a profit and has benefitted from all the hype around Casper’s 2019 fundraise and the impending IPO.

However, the stock performance of Purple could be a warning for any Casper investors.

Purple’s stock price is being bid up only because Casper’s IPO valuation has set a new high watermark for mattress valuations.

There is a real risk that Casper’s valuation is inflated and does not represent how the public markets will really value the company longer term.

Once the IPO is old news, Casper’s slower growth and deep losses could cause the stock to actually trade at a discount to Purple, at least 20%-40% below the expected IPO price of $18/sh.

Note: Grizzle subscribers get access to our full Casper IPO guide starting next week. Signup is free and gives you access to all of Grizzle’s best ideas and private weekly strategy email.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.