Affirm is the most hyped private company set to go public so far in 2021.

Founded by Max Levchin, a legend in Silicon Valley for founding Paypal as well as Slide which was sold to Google.

To help you decide whether Affirm is worth an investment, we’ve put together this comprehensive guide looking at factors like:

- What does Affirm do?

- The economics of the business

- The biggest risk facing Affirm

- What the stock is worth today and 10 years from now?

What Does Affirm Do?

Simply put, Affirm is a new age credit card company.

Affirm lends you money you don’t have to make purchases for things you want today.

Where Affirm is different than a credit card company is that they offer slightly longer payment terms and for the best borrowers will let you borrow for up to 39 months interest-free as long as you make the monthly principal payments.

So compared to a typical credit card, Affirm always offers longer payment terms and sometimes offers a better interest rate, but only if you qualify.

The products Affirm offers to consumers and merchants are listed below.

1) A Point-of-Sale payment solution for consumers

- Integrated Checkout – Allows consumers to pay for items with a fixed payment plan for purchases under $250 with select merchants (instead of purchasing the total amount at once) without deferred interest, hidden fees or penalties (Affirm offers both zero interest and simple interest, never-compounding loans).

- Even if a customer misses a payment, the total amount owed at their final checkout never changes.

- They never sell the servicing rights to outstanding balances,

- Customers can also set their own repayment dates that align with their monthly budgets

- Virtual Card – consumers can apply for a universally accepted method of payment on a Visa payment system

- Merchant commerce solutions

- Customer acquisition, product-level data and insights, customer conversion

- Easy integration (API) for merchants’ websites

- By offering Affirm, merchants increase their customer base by adding clients that may can only pay for their products in installments (model works well for Affirm merchants like: Peleton, Priceline, Shopify etc.)

- A consumer-focused app

- Consumers can manage payments

- Access to a personalized marketplace (consumers can find products and buy from partner merchants)

- Offers shown to consumers are based on their spending and shopping habits

- A savings account on the app

- Customers can open a high-yield FDIC-insured interest-bearing savings account

- Provided by Cross River Bank – no minimum deposit or fees

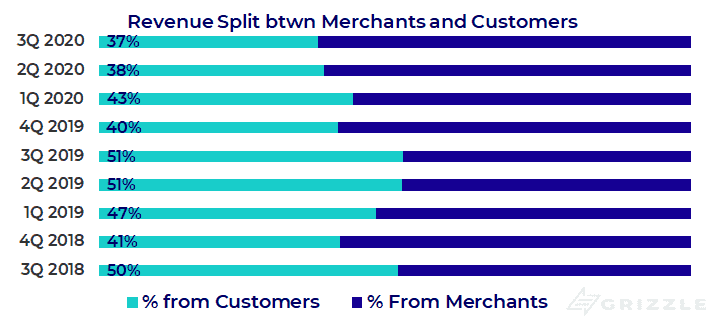

How Does Affirm Make Money

Affirm makes money two main ways.

- If you borrow from them to buy something they charge you interest.

- Merchants pay Affirm a fee for giving you a loan which helped convince you to buy something even when you didn’t have enough cash.

Some other, but less important ways Affirm generates revenue is through loan processing fees, interchange fees and selling the loans they originated for a gain.

The disruption of this new lending model is that interest is not how Affirm makes most of its money, unlike most credit card companies.

They are more reliant on the fees they get from merchants when you buy a product and aren’t as incentivized to keep borrowers in debt to extract as much interest as possible.

Competitor Afterpay pioneered the “buy now pay later” space and Affirm is taking full advantage of this new business model.

The lower the interest rate Affirm offers each customer the larger the fee they charge the merchant.

The author personally sees 0% APR offers from Affirm all over the internet and these are the most lucrative for the company with merchants paying Affirm 3% or more of the merchandise value.

Affirm has benefitted mightily from growth in 0% loans and they now make up 46% of gross merchandise value sold.

While a tailwind so far, this huge reliance on 0% financing for revenue growth may now be turning into a headwind.

Read on…

An investment in Affirm is an Investment in Peloton

One can argue the current success of Affirm can be traced back to a fateful decision to partner with exercise equipment provider Peloton in 2015.

With the world quarantined inside for the last 9 months, Peloton has absolutely crushed it in 2020 and Affirm has been along for the ride.

But all of this success has left Affirm heavily reliant on Peloton for revenue growth.

As of September 2020, we estimate Peloton made up 30% of Affirm’s total revenue and a whopping 56% of merchant revenue.

More importantly, Peloton is driving a big chunk of Affirms revenue growth.

Affirm grew revenue 100% in the September quarter, but take Peloton out and the company grew only 60%.

Investors need to keep in mind the world is going to come out of the pandemic in 2021 and sales of Peloton equipment will likely at least slow if not decline.

Affirm could see much slower revenue growth as a result, which would hurt the stock price as the valuation of money-losing tech stocks like affirm is directly tied to how fast they can grow revenue.

Anyone buying Affirm in the first half of 2021 is indirectly making a bet on the future of Peloton.

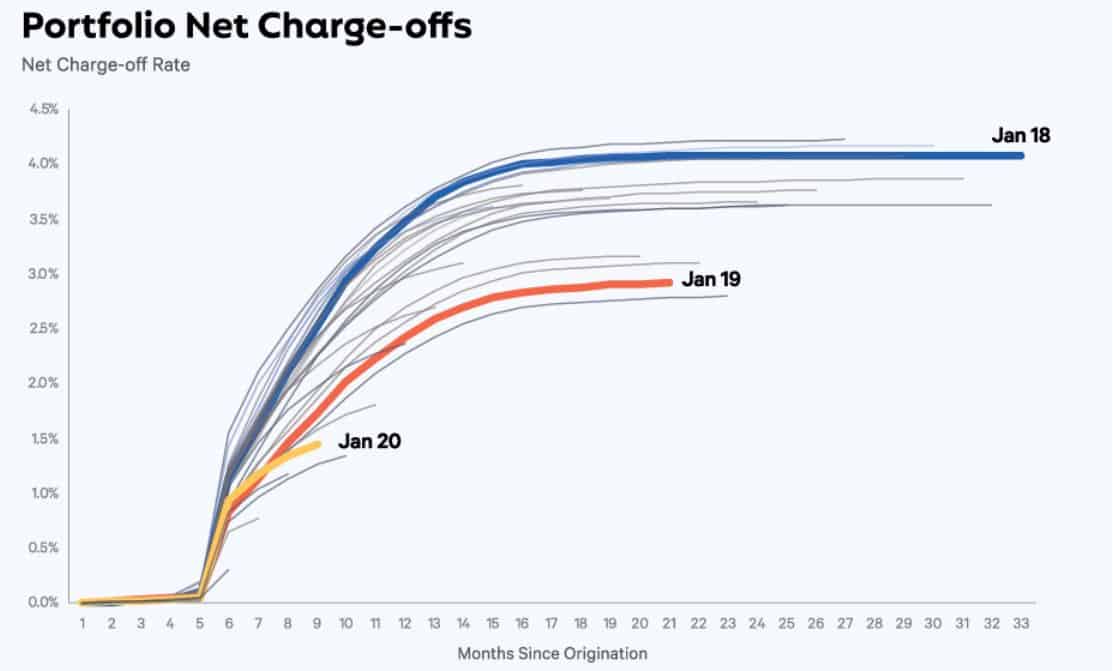

The Lending Business Itself Remains the Other Risk to Affirm

Affirm is still a lender at the end of the day and will live or die by its underwriting (loan-making) standards.

Affirm only generates $0.01-$0.03 cents of gross margin per $1 of lending so there is very little margin for error.

At the start of the pandemic, when the company thought consumers were in for a world of hurt, they booked $80 million in loan loss reserves, up from $30 million the quarter before.

This change alone flipped gross margins from positive to negative.

Bottom Line: Affirm hasn’t been through a full credit cycle and if they write loans to the wrong people, they could suffer big losses during the inevitable downturn, offsetting years of profits.

This is simply the risk of lending consumer’s money and it must be managed with care.

Losses are Falling, but That Happens in an Economic Expansion

Affirm Will be Priced at a Premium Out of the Gate

Affirm is going public at $44/sh according to the latest filing, valuing the company at $11-$15 billion depending on if you use common or diluted shares outstanding.

This may seem expensive at 13x our revenue estimate for next year, but we guarantee you this stock is going to get much more expensive before the first day of trading is over.

That’s because the company’s largest global competitor, Afterpay trades for almost double the market cap and 2.6x the revenue multiple of Affirm.

The stock market we currently find ourselves in doesn’t care that Afterpay has twice the gross merchandise value of Affirm or triple the active customers, all it cares about is growth.

Comp Table (Affirm vs Afterpay)

Considering that both companies were growing close to 100% through June 2020, we are confident the market has already come to the conclusion that Affirm should trade in line with Afterpay.

We are confident Affirm will trade somewhere between $20-$25 billion once the dust has settled from the IPO ($61-$76/sh) and could be up 50% or more from the $44/sh IPO price on the first day of trading.

If Affirm were to trade at 31x next year’s sales, in-line with Afterpay, we would be looking at a $94 stock.

This is the type of upside investors should be playing for in the short term.

The Long View

Looking out longer than just the next twelve months, we think Affirm does have potential.

Management has a stellar track record of success and understands the opportunities inside and out.

Affirm is attacking a huge market with e-commerce sales estimated to grow to $1.1 trillion by 2024 compared to less than $5 billion of sales taking place through Affirm in 2020.

Market Opportunity is Massive

Affirm is taking business away from credit cards and banks with better terms for both merchants and customers and less predatory lending with no compound interest and late fee charges.

Affirm is approaching profitability and if the company can grow 70% or more in 2021, it should start generating consistent profits.

The stock will be very expensive out of the gate which does introduce risks to owning it as a small disappointment in the growth rate will hit the stock hard.

However, the CEO’s star power and the popularity of this business model among global investors make Affirm a worthy investment.

As long as we don’t see a sales meltdown from Peloton later this year we think this stock will run in 2021.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.