SUBSCRIBE TO GRIZZLE and Invest Smarter

Who is Sprout Social

Sprout Social offers social media management software.

Basically, if you have more than one social media account, Sprout Social will simplify your life by allowing you to manage all of your accounts from one place.

You can see user comments, auto-post content and create unique content for each platform all in one place.

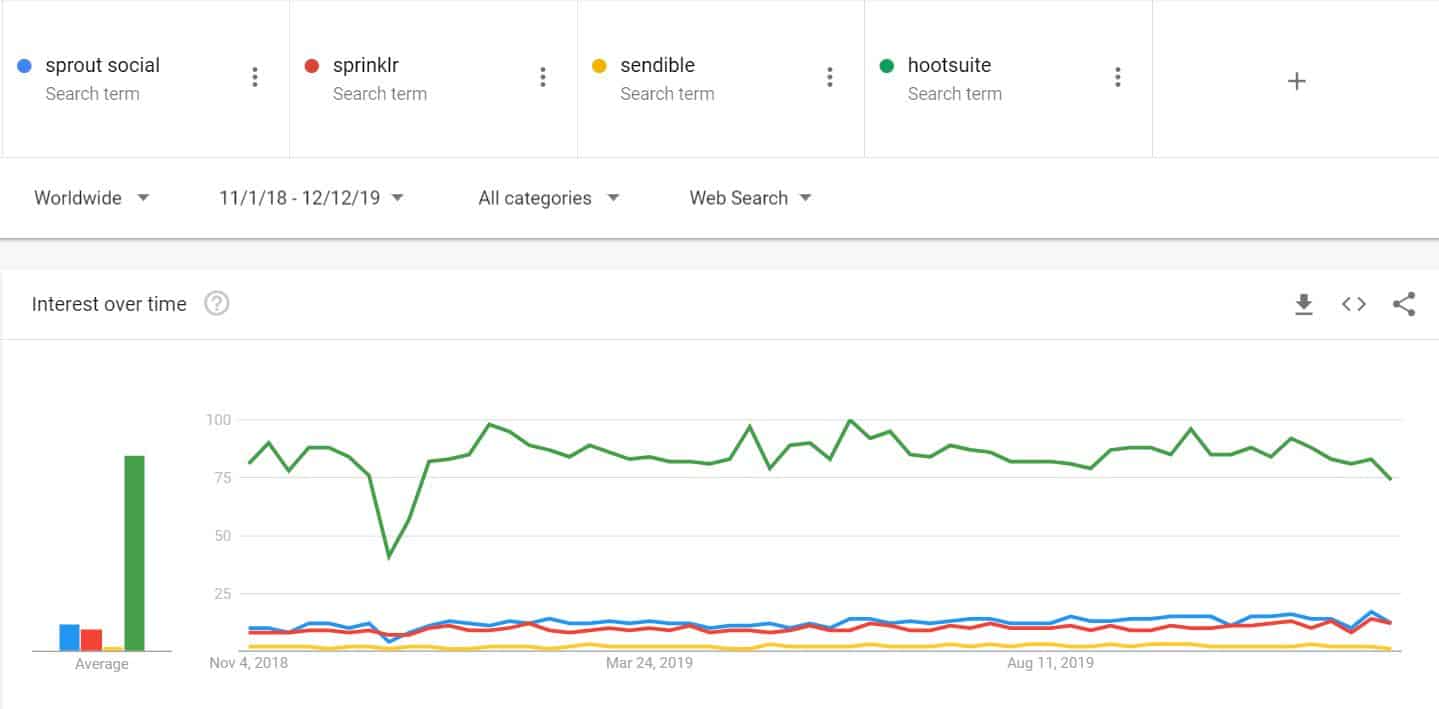

No Clear Growth in Popularity

When looking at the popularity of Sprout Social based on the number of Google searches, there isn’t a clear trend in either direction.

Sprout Social is much less popular than Hootsuite and doesn’t seem to be gaining or losing market share over the last two years.

Google search data is not perfect but we would like to see a rising trend to tell us Sprout Social is growing more than the speed of the market.

In 2018 the number of users on a social media platform grew 10% which tells us the company is growing at about twice the market rate, but peers are as well.

Google Search Trends for Sprout Social (BLUE)

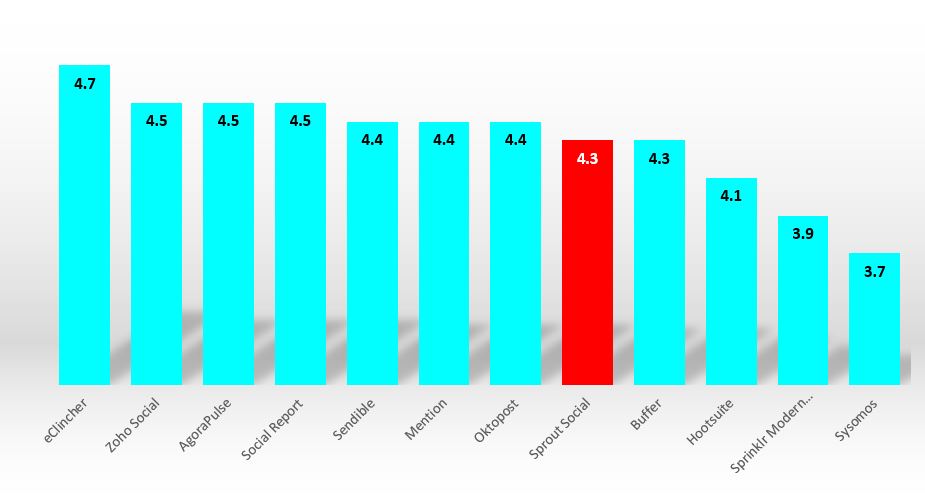

User Experience Could Use Some Work

Looking at online user reviews, Sprout Social must not have many evangelists.

Though the service is popular, from the 9,500 reviews we compiled, users are just lukewarm on the user experience.

On G2.com, where most reviews were found, Sprout Social was ranked average with a rating of 4.3 out of 5.

Sprout Social User Reviews Only Average

The user experience is critical to keep newly acquired customers.

Sprout Social may be growing today, but if customers don’t stick around, costs to acquire new users are going up and both revenue growth and profit margins are going down.

We would watch customer growth and acquisition costs closely for any signs of customer defections getting worse.

Pricing Tiers of Sprout Social and Peers

| Monthly Pricing Plans | 10 Profiles | 20 Profiles | 35 Profiles |

| HootSuite | $29 | $129 | $599 |

| Buffer | $18 | $99 | N/A |

| Sprout Social | $274 | $499 | $1,350 |

| SocialOomph | $25 | $130 | $405 |

| Sendible | $29 | $99 | $254 |

| AgoraPulse | $99 | $199 | $299 |

| Social Report | $49 | $99 | $199 |

| Hubspot | $50 | N/A | $800 |

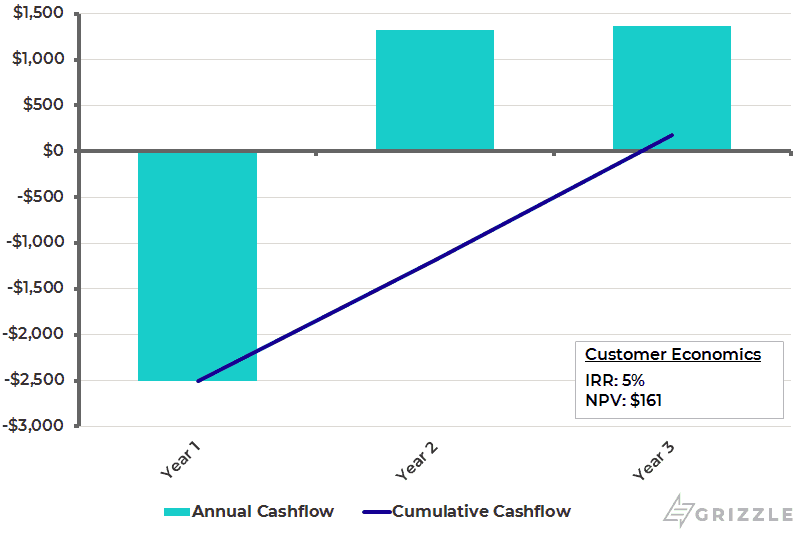

Customer Economics are Decent but Hard to Verify

Per customer economics are actually quite decent in what is obviously a competitive market

It costs Sprout Social $3,700 in sales commissions to win a customer who the company thinks will stick around for about 3 years.

This is 35% more to acquire a customer than public competitor HubSpot.

Even so, with annual revenue per user of $4,600 in the latest quarter, Sprout is generating a decent return on each customer, 5% or $160 dollars we estimate over the three-year life of an average client.

Current Customer Economics for Sprout Social

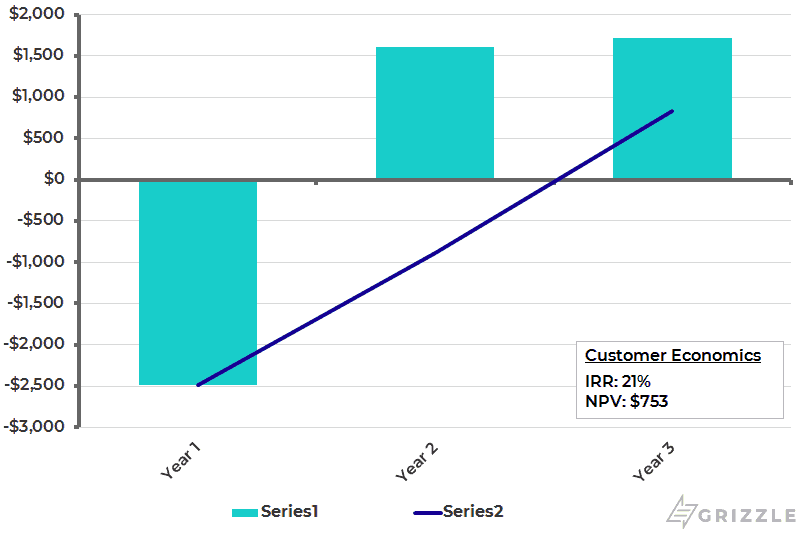

As the company scales and spreads salaries and research expenses over more customers we think the economics will likely improve with an internal rate of return as high as 20%.

This sounds attractive but with limited user history and no data on the attrition rate of customers we would caution that our acquisition cost estimates are very rough.

Even small changes to the estimate of users who quit the service make the economics look very different.

Forecast Future Economics for Sprout Social

What we do know is Sprout Social loses far more money than larger peer HubSpot even though growth is actually slower.

Typically, the less you spend on growth, the more money is left over to flow to the bottom line.

Our hunch is that Sprout Social has worse customer economics than HubSpot and therefore should trade at a discount.

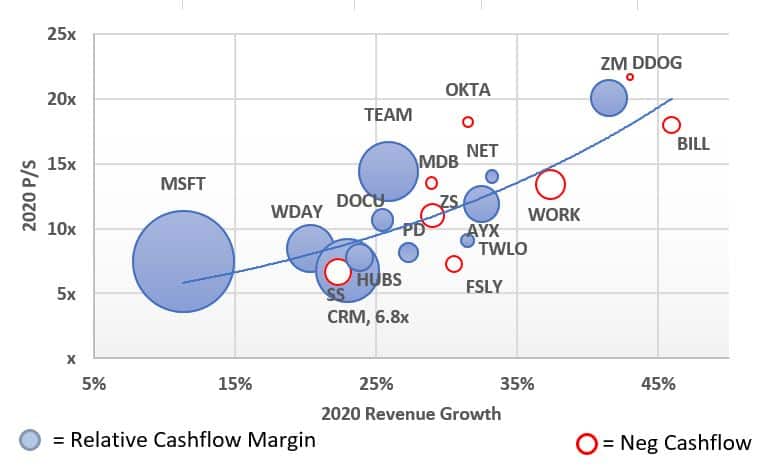

What is Sprout Social Worth?

The expected IPO price of $16-$18 a share would value Sprout Social at up to $890 million.

First, we’ll compare Sprout to its best public comparable HubSpot.

HubSpot has been public since 2014 and offers many of the same social media services as Sprout Social.

It looks to us like Sprout Social management is pricing the IPO to be in line with the trading multiple of HubSpot at 7x-8x revenue.

[su_panel background=”#C6E1FF” color=”#110076″ border=”px none ” shadow=”px px px ” radius=”4″ text_align=”center” class=”dw-editor-note”]We don’t think Sprout Social should be trading in line with HubSpot. Sprout Social is growing slower than HubSpot plus is losing lots of money, HubSpot, in contrast, is cashflow positive. [/su_panel]Sprout Social doesn’t look to be offering investors any bargains.

The stock is priced expensive in our view compared to HubSpot and in-line with the trend line for the software as a service (SaaS) group in general.

With the uncertainties around profitability in a highly competitive marketplace, we wouldn’t be buying in unless the stock falls to $13.00/sh or lower.

Sprout Social (SS) Valuation vs Peers and HubSpot (HUBS)

Share Unlock, Float and Other Details a Trader Needs to Know

Sprout Social is planning to issue 10.15 million shares in the IPO, which would mean 21% of common shares outstanding will be free to trade while the other 79% will be locked up.

This is a slightly higher float that the 14%-17% we typically see with IPOs.

It could mean that Sprout is looking to raise more cash than is typical, perhaps to grow or just to give them a longer spending runway.

Mark your calendars, 79% of the shares outstanding will come off lockup on April 23, 2020 and can be sold into the open market.

The expiration of lockup agreements traditionally cause short-term downward pressure on stock prices and are important catalysts to watch for.

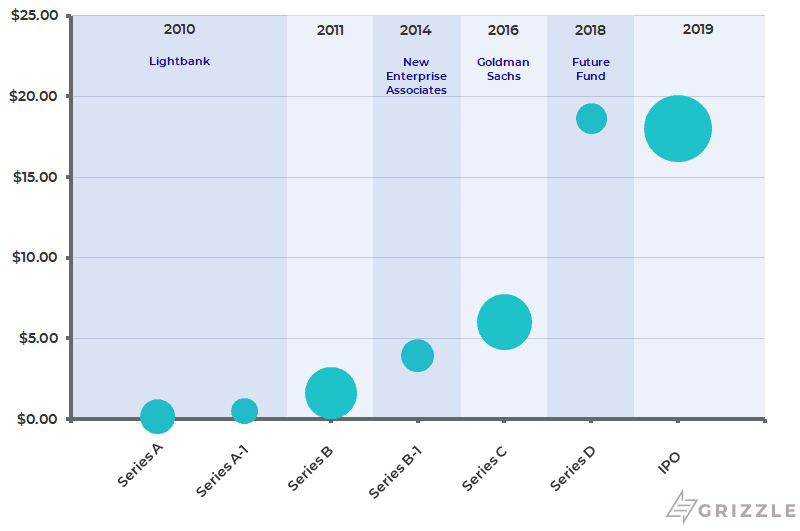

Insiders Bought Their Shares at $4.69 on Average

The expected IPO price of $18 will make many insiders very rich.

Management, investors, and employees acquired their shares for $4.69 on average giving them ~300% upside if they were to sell after the stock goes public.

Cost Basis of Funding Rounds (Circle Size = % of Shares)

21% of shares have a cost basis of $1.64 or less and are looking at gains of 1000%+.

The IPO price of $18/sh is below the last funding round but still up big from the funding rounds in 2016 and earlier.

A low cost basis increases the incentive insiders have to sell their stock as soon as they are able, potentially putting downward pressure on the stock price.

What to Do With Sprout Social Stock

Sprout Social is riding a huge trend in the business world towards social media.

The internet is where the marketing dollars and eyeballs are headed and a good majority of those eyeballs are glued to social media platforms like Facebook, Twitter, Instagram, and Snap.

Any brand that wants to thrive must have a presence on social media and software like Sprout Social is key to managing the multiple social media profiles needed to effectively reach consumers on the internet.

The product is in demand, but the valuation is just not attractive given the question marks about profitability.

As usual with IPOs, we don’t expect much value to be left for individual investors on day 1, but investors should keep this stock on their radar and see if management can maintain revenue growth at 30% or higher.

If they can, this stock is definitely going higher, regardless of the cash burn.

HubSpot Stock Crushing it Due to Strong Revenue Growth

But if growth continues to slow while profits are nowhere to be found, Sprout Social will be the first and last social media software provider to hit public markets anytime soon.

[su_panel background=”#C6E1FF” color=”#110076″ border=”px none ” shadow=”px px px ” radius=”4″ text_align=”center” class=”dw-editor-note”]If you’d like us to track Sprout Socials’ progress for you, subscribers to Grizzle will receive free alerts if the stock hits our buy price or runs into a speedbump that makes it no longer investable.[/su_panel]SUBSCRIBE TO GRIZZLE and Invest Smarter

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.