China Relations: The White House isn’t Mincing Words

There have been rising concerns of late about a new Cold War between America and China. It has to be admitted that these concerns are not without some foundation.

Anyone who doubts this should read a paper published by the White House on 20 May titled United States Strategic Approach to the People’s Republic of China.

Experts on US China relations say there has been nothing like this written before in recent history.

Contained within the first paragraph of the 16-page document are the following two sentences: “Beijing openly acknowledges that it seeks to transform the international order to align with CCP (Chinese Communist Party) interests and ideology.

The CCP’s expanding use of economic, political and military power to compel acquiescence from nation-states harms vital American interests and undermines the sovereignty and dignity of countries and individuals around the world.”

These are pretty assertive, if not sweeping, statements.

Aside from making it clear that China is viewed as at best a strategic rival and at worse an enemy, the report also singles out the role played by President Xi Jinping, both in terms of removing presidential limits and in terms of his desire to build a “system of socialism with Chinese characteristics”.

This system, says the report, is “rooted in Beijing’s interpretation of Marxist-Leninist ideology and combines a nationalistic, single-party dictatorship; a state-directed economy; deployment of science and technology in the service of the state; and the subordination of individual rights to serve CCP ends.

This runs counter to principles shared by the United States and any likeminded countries of representative government, free enterprise, and the inherent dignity and worth of every individual.”

The Cold War-style nature of this report is reflected in the heavy ideological tone, as reflected in the above quotes.

This is not to deny that under Xi the Leninist nature of the Chinese system has undoubtedly been strengthened to a remarkable extent and that, as the report says, “the distinctions between the government and the party are eroding” while hopes of political reform have “atrophied”.

Still if all is indeed the case it still raises the issue of whether American policy towards China is going to be as ideologically driven going forward as the authors of this report would undoubtedly like it to be.

This writer is not yet convinced of this since a re-elected Donald Trump would likely back off such a hard ideological line since the 45th American president does not really do ideology.

Indeed he has probably only allowed such a document to be published because of his seeming recent decision to run the presidential campaign on blaming China for COVID-19 and 119,131 American deaths and counting.

Trump the “Deal Maker” will Prioritize Economy over Ideology

Rather as a businessman and self-pronounced deal maker, a re-elected Trump is more likely to focus on the practical reality of what China is.

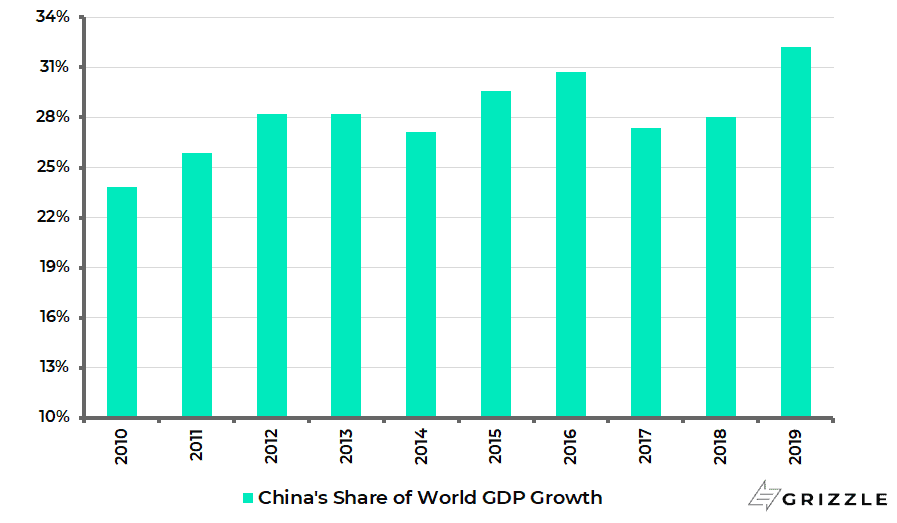

That is the second-largest economy in the world which last year accounted for 32% of the world’s recorded GDP growth.

China’s share of world GDP growth

That will also be what the American business and financial community will want to do. Their agenda is certainly directly threatened by the national security zealots in the Trump administration, led by Secretary of State Mike Pompeo, an evangelical Christian, who seems to view the Chinese government as evil.

As for the Democrats, there are many within that party who have become anti-China in the past four years, as they have finally woken up to the reality that China is not turning into a Western democracy as many on the “liberal” side of American politics had previously assumed would be the case; even though China itself never encouraged such expectations.

Still as Joe Biden had a track record of being pro-China when vice president, in terms of the then fashionable policy of engagement, that creates another reason for Trump to run as the “tough on China” candidate. The other incentive is that, by backing the likes of Pompeo, it will also help bring in the evangelical Christian vote which certainly helped Trump win four years ago.

Still if all this is indeed the case, it does raise the issue of how China will react in the short term. The Chinese leadership will understand the pre-election calculations so they probably will be keeping an open mind on how a re-elected Trump would act.

As for a Biden win, the nature of a Biden administration is going to be heavily influenced by who is his choice of vice-presidential candidate since this will highlight just how left-wing might be his agenda.

Certainly, the tax hikes officially proposed by the Biden campaign look quite aggressive in an American context. Biden has proposed to increase the corporate income tax rate from 21% to 28% and the capital gains tax from 20% to 39.6%, and to raise the income tax rate for the richest Americans with taxable incomes above US$400,000 from 37% to 39.6%.

If such an outcome is also reflected in foreign policy, in terms of a focus on human rights abuses in authoritarian China, that could also keep tensions high.

China Dangling a Carrot for Foreign Direct Investment

But whichever way US politics goes in November, Beijing will have seen enough already to assume that a Cold War outcome is now a distinct possibility, if not yet necessarily a probability.

This means that in the political area it has less incentive to play nice in its dealings with Hong Kong and Taiwan, while in the technological area it will be more determined than ever to end its dependence on US technology.

Still a sign that it has given up all hope of a mutually beneficially co-existence will be if and when Beijing starts putting pressure on American corporates doing business in China by, for example, telling its nationalistic population to stop buying American products.

So far it has resisted the temptation of such retaliation because it understands that Apple or Starbucks, to name just two of many American companies doing business successfully in China, are on the same side as the Chinese government in this dispute.

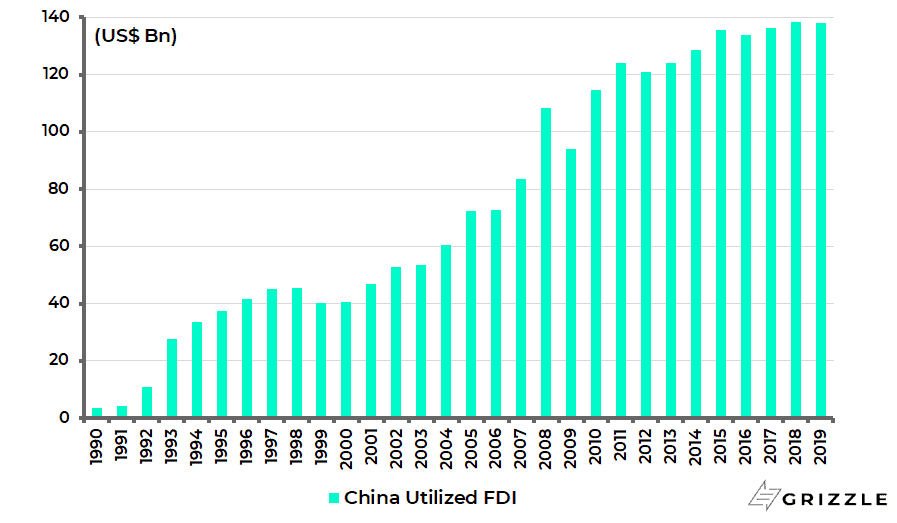

This is why China has been increasingly offering a carrot to foreign direct investors by allowing them to run wholly owned businesses in the mainland. The benefits of this policy can be seen in the still healthy trend in FDI into China, including from America. China utilized FDI has risen from US$41bn in 2000 to US$138bn in both 2018 and 2019 (see following chart).

China Utilised FDI (Foreign Direct Investment)

The Risk of Hong Kong Tensions Continuing to Flare

If all this is the case, there is clearly a risk of further confrontation in the run up to November, most particularly with the world media’s attention again on Hong Kong.

The risk now is that Hong Kong becomes a political football in the US-China dispute and the China hawks in Washington led by Pompeo have an obvious lever to pull if they want to escalate tensions, say in response to another tough crackdown on pro-democracy demonstrations in the city state.

That is to remove the special status enjoyed by Hong Kong under the United States-Hong Kong Policy Act of 1992. That could even be followed, worse case, by US sanctions which could severely impede Hong Kong’s role as an international financial centre.

If all this is quite possible, it is important to understand that such developments do not mean the end of Hong Kong. Rather they mean the end of Hong Kong as the world has known it and certainly the end of “One Country Two Systems”.

Hong Kong Financial Hub Will Become More China Centric

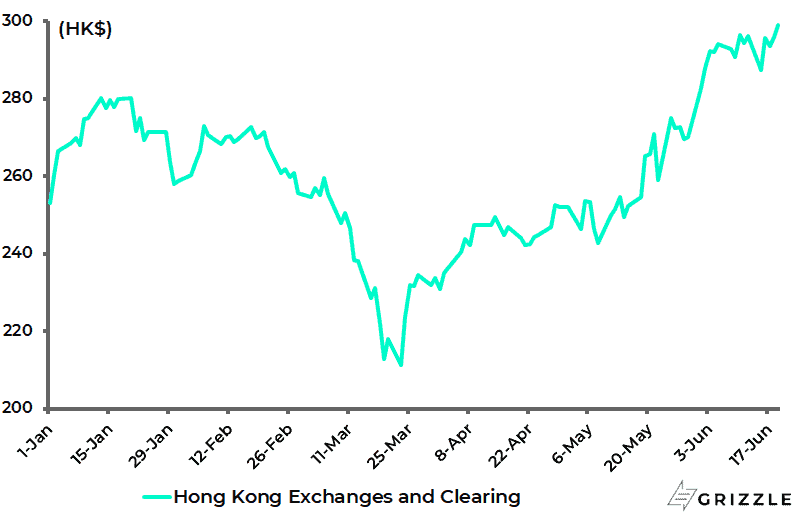

What will replace it? The answer can be found in the recent action in the Hong Kong stock market with the share price of Hong Kong Stock Exchange rising by 15% since the day after the announcement on 21 May at China’s National People’s Congress of the introduction of National Security legislation for Hong Kong (see following chart).

Hong Kong Exchanges’ Share Price

If the trigger for this move is the ongoing passage of a bill in Congress to make Chinese companies submit to American accounting standards, the irony is that President Xi will have no problem with this particular Washington-driven agenda.

For Xi has made it quite clear that he would prefer it if these major Chinese corporates were listed closer to home, as Alibaba now is following its Hong Kong listing in November 2019.

The result of such an outcome is that Hong Kong as a financial centre will become ever more China centric and China focused.

Still with the closed capital account remaining in place so long as China is run by the PRC, Hong Kong will continue to play a critical role as the conduit to the outside world via its highly successful stock and bond connects.

Indeed if Hong Kong did not exist, its equivalent would need to be invented from a PRC perspective.

Meanwhile as China explicitly asserts control over Hong Kong in coming months, via the likely establishment of a formal and visible national security apparatus within the territory, so China in a strange kind of way will become responsible for the city’s prosperity.

In this respect, Beijing will not want to see the local economy and property markets collapse once it has formally taken over in terms of being in charge of law and order.

Still in the shorter term, if the pro-democracy activists hit the streets again and there is violence, Beijing will have no problem witnessing a collapse in local asset prices since this would be viewed as showing the negative consequences of such disruptive actions.

It could then at a later date order Chinese state-owned developers to buy at land auctions at depressed prices, a signal that would then be highly appreciated in property obsessed Hong Kong.

The views expressed in Chris Wood’s column on Grizzle reflect Chris Wood’s personal opinion only, and they have not been reviewed or endorsed by Jefferies. The information in the column has not been reviewed or verified by Jefferies. None of Jefferies, its affiliates or employees, directors or officers shall have any liability whatsoever in connection with the content published on this website.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.