Before Russia’s invasion of Ukraine, it was always likely that US inflation would peak with the March data point due to the pronounced base effect.

It is still possible that the March CPI report of 8.5% YoY marks the peak, barring more geopolitical shocks triggered by Ukraine such as the Eurozone deciding not to buy Russian energy.

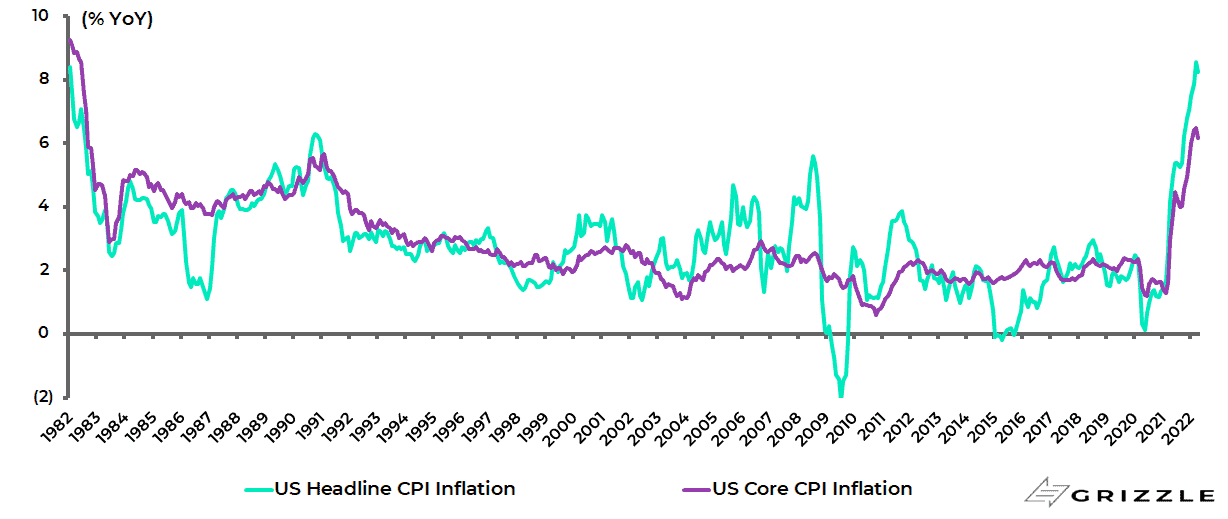

Still underlying inflation is running well above 4%, while the April CPI report was nearly as high.

US CPI rose by 0.3% MoM and 8.3% YoY in April, while core CPI was up 0.6% MoM and 6.2% YoY.

US CPI inflation

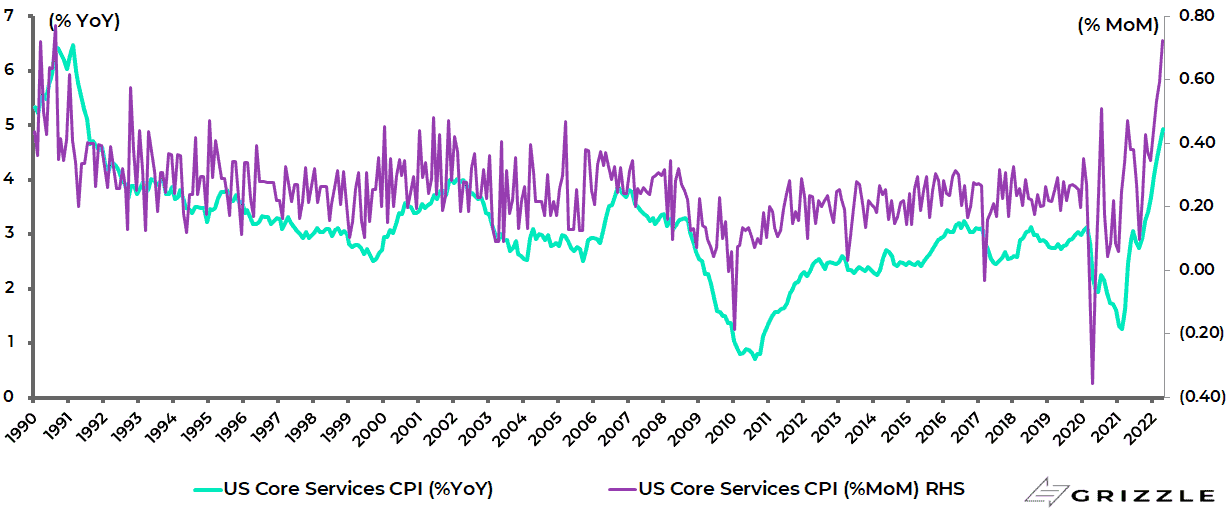

It is also the case that inflationary pressures are moving from goods to services, where they risk becoming more entrenched.

Core services CPI inflation accelerated to 0.72% MoM and 4.9% YoY in April, the biggest monthly increase since August 1990 and the largest YoY inflation print since July 1991.

US core services CPI inflation

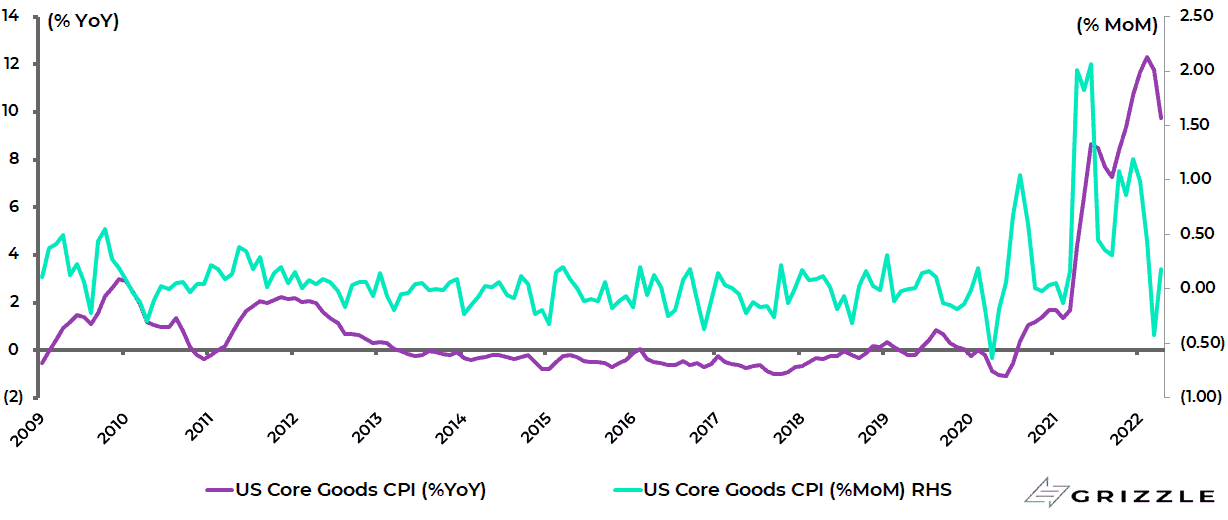

By contrast, core goods CPI rose by only 0.18% MoM in April after a 0.4% MoM decline in March. It was up 9.7% YoY in April, down from 12.3% YoY in February.

US core goods CPI inflation

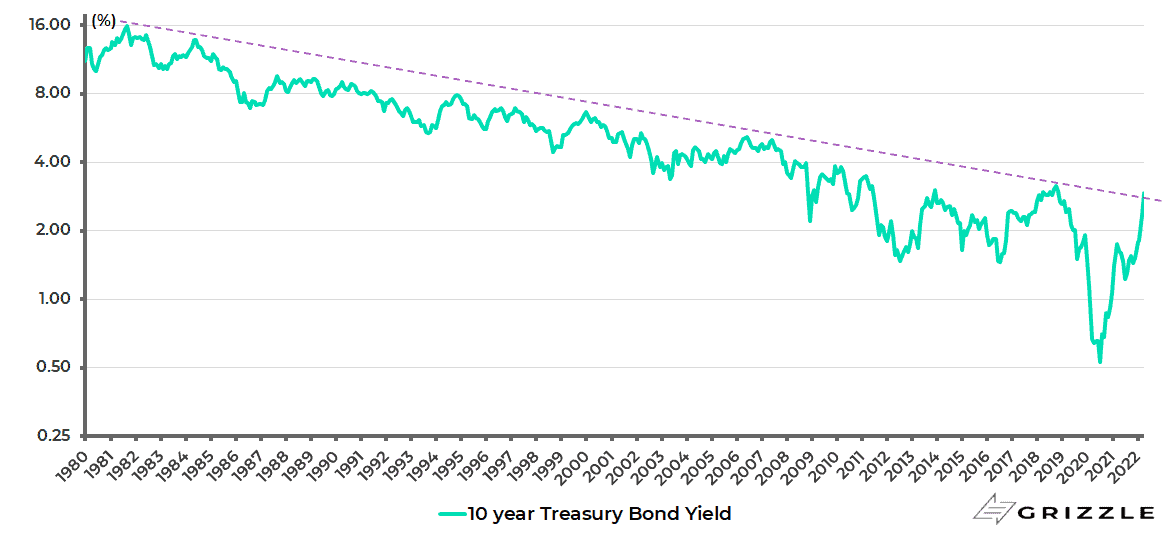

The ten-year Treasury bond yield has now touched the trend line in place since the beginning of the bond bull market in 1981, which is currently at around 2.8%.

The 10-year Treasury bond yield rose to 3.2% on 9 May and is now 2.78%.

As discussed here previously (Will Alternative Investments Cause A Lehman Moment?, 19 May 2022), it makes sense for fixed-income investors to start to think about adding exposure to long-term Treasury bonds at this juncture if the view is taken that both the Fed is committed to real monetary tightening and that inflation has put in a peak.

US 10-year Treasury bond yield (monthly log scale chart)

Source: Bloomberg

Eurozone Lurching Toward Monetary Tightening

On the Eurozone, the evidence of late has been that the hawks have been gaining more traction in terms of more ECB board members pushing for an earlier end to tapering and earlier commencement of rate hikes.

Thus, the minutes of the March ECB meeting, published on 7 April, revealed that some ECB members preferred to set a “firm end date” for net asset purchases during the summer which could “clear the way for a possible rate rise in the third quarter”.

As for the last ECB meeting in mid-April, the ECB statement noted that “inflation pressures have intensified across many sectors” and that incoming data since its last meeting reinforce the expectation that net asset purchases under its asset purchase programme “should be concluded in the third quarter”.

Expectations for rate hikes have also moved up. Money markets are now discounting a 25-30bp rate hike in July and a total of 100bp of rate hikes by the end of this year.

Meanwhile, the trend remains towards fiscal integration in the Eurozone as reflected in the €750bn EU Recovery Fund.

Also, with French President Emmanuel Macron’s re-election in France, the French and German governments are currently singing off the same hymn sheet.

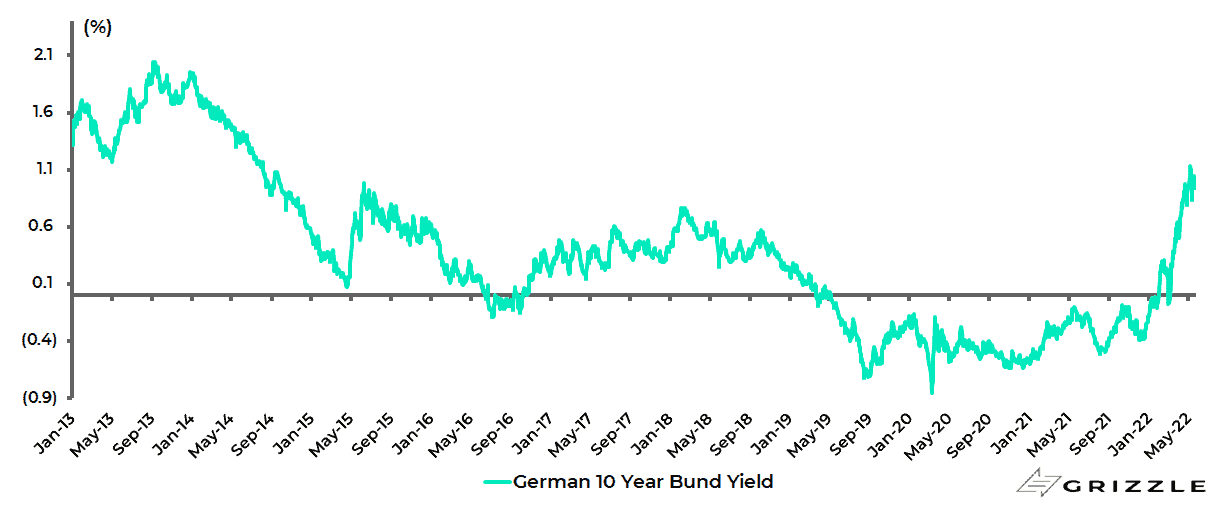

This is most bearish for German bunds.

The ten-year bund yield is now 0.94%, up from a bottom of minus 0.9% reached in March 2020.

German 10-year bund yield

Yield Curve Control Continues in Japan but will be Gated by Weakness in the Yen

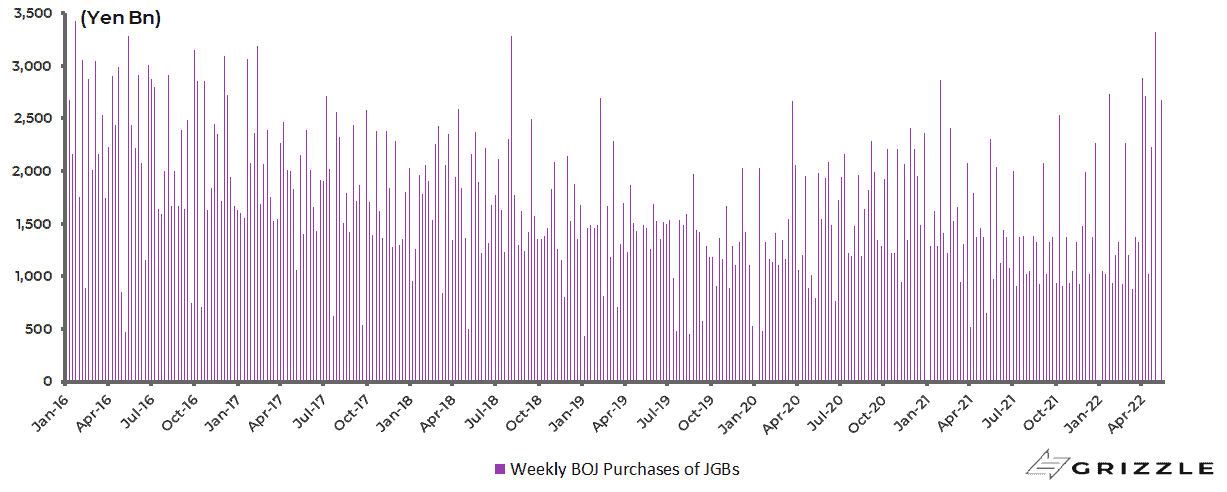

As for JGBs, the Bank of Japan continues stepped-up buying to defend the yield curve control policy in terms of keeping the 10-year JGB yield below 25bp.

The BoJ bought Y3.32tn of JGBs in the week ended 29 April, the biggest weekly buying since January 2016 (see following chart), though the weekly net buying slowed somewhat to Y2.68tn in the week ended 13 May and Y1.03tn last week.

Bank of Japan weekly buying of JGBs

Still, there is a growing likelihood that Haruhiko Kuroda will be forced to adjust policy with the key trigger further downward pressure on the yen.

Meanwhile, any future move out of negative rates in both the Eurozone and Japan is positive not only for the relevant banking sectors but also for the broader economies.

This is because the impact of negative rates is deflationary, not inflationary, since it increases households’ risk aversion.

China Does Not Share the World’s Inflation Problems and has Room for QE

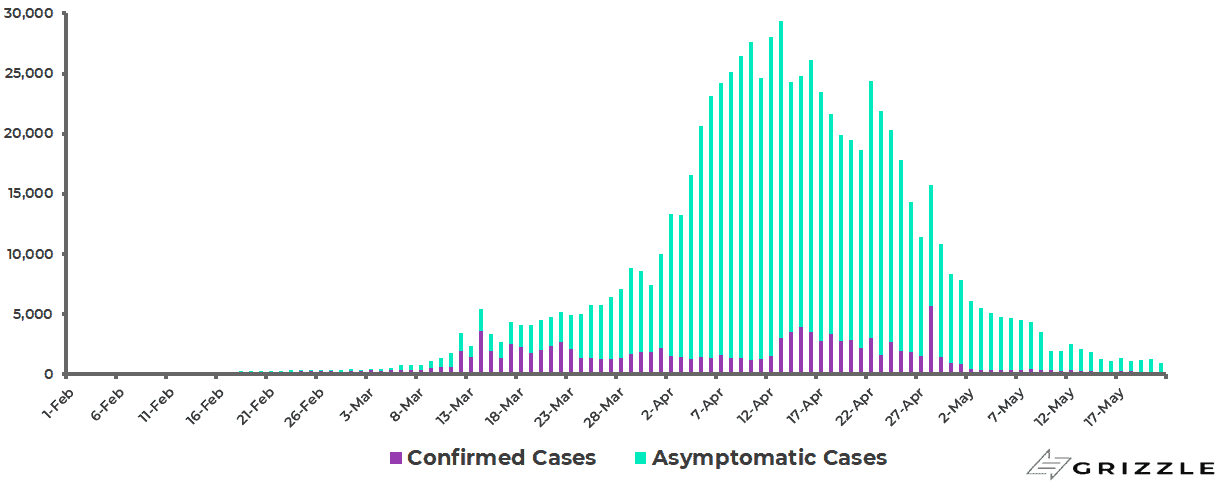

Meanwhile, in China, there is growing focus on whether President Xi Jinping risks suffering a double-whammy negative in terms of both damaging the economy, via the continuing enforcement of the Covid suppression policy, while also losing control of Omicron.

Still for now, the cases seem under control, while deaths remain low.

The number of daily new Covid cases in China, including confirmed and asymptomatic cases, rose to a record 29,411 on 13 April but has since declined to 898 on 21 May, with 89% of the new cases so far in April-May asymptomatic.

China daily new Covid cases

There have “only” been 586 Covid deaths in China so far this year, based on the official data.

Meanwhile, it is surprising that Beijing seems to be prioritising testing over vaccinations.

True, a total of 89% of the population are fully vaccinated, with 54% having taken the booster dose as of 12 May, based on the most recent data reported by the National Health Commission.

But, for those aged 60 and above, only 62% have had the required three doses of the Sinovac or Sinopharm vaccines as of 12 May, which is what is required to make them effective.

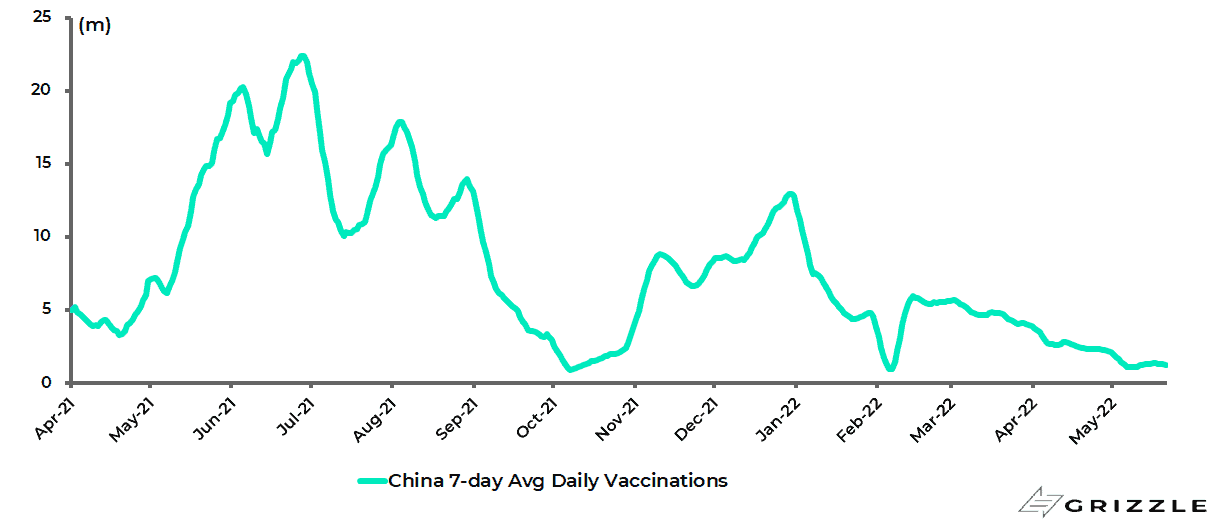

Meanwhile, the 7-day average daily vaccination rate has declined from 13m in late December to only 1.3m.

China 7-day average daily vaccinations

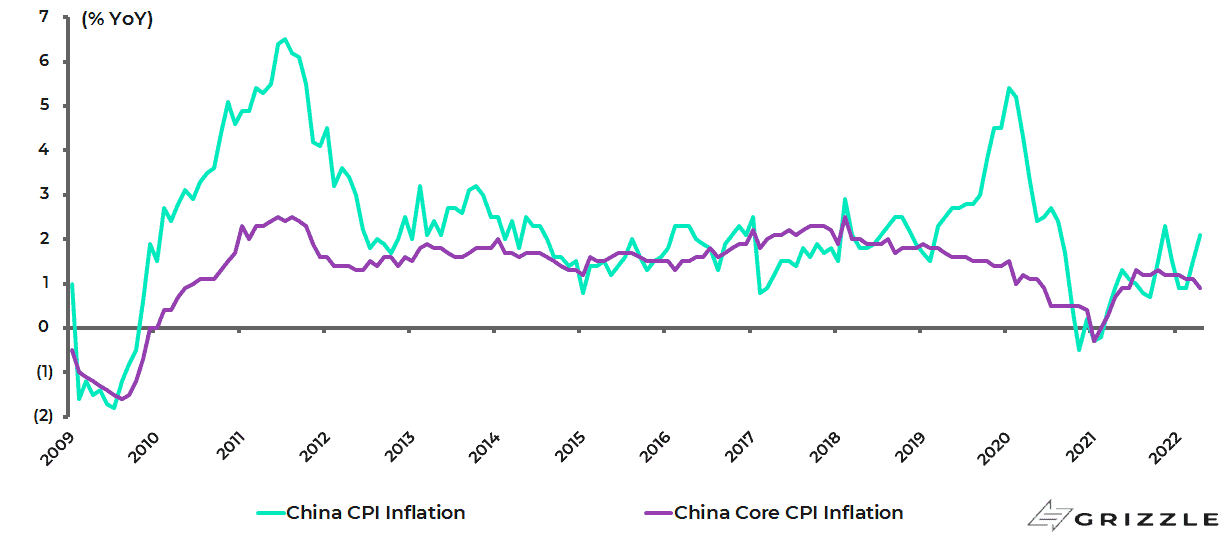

But if China currently has some problems, inflation is not one of them.

China headline CPI inflation was 2.1% YoY in April, while core CPI inflation was 0.9% YoY.

China CPI inflation

The views expressed in Chris Wood’s column on Grizzle reflect Chris Wood’s personal opinion only, and they have not been reviewed or endorsed by Jefferies. The information in the column has not been reviewed or verified by Jefferies. None of Jefferies, its affiliates or employees, directors or officers shall have any liability whatsoever in connection with the content published on this website.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.