Bottom Line

Early indications point to investors not loving the huge mark to market net loss of $218 million in Acreage Holdings (CNSX: ACRG.U) Q4 2018 earnings.

However $200 million of the loss comes from unrealized losses on derivatives and non-cash stock compensation.

At the end of the day Acreage lost about $10 million on revenue of $23 million in the quarter, which is in line with losses seen at most other Multi-State Operators (MSO).

We would be looking to scale into Acreage on any dip tomorrow and over the rest of the week as the company still has the largest state footprint in America, trades at a discount and is executing well despite many moving parts.

An upcoming share unlock on March 14 or 15 could put additional pressure on the stock so look for more than one opportunity to buy at a lower price over the next few trading days.

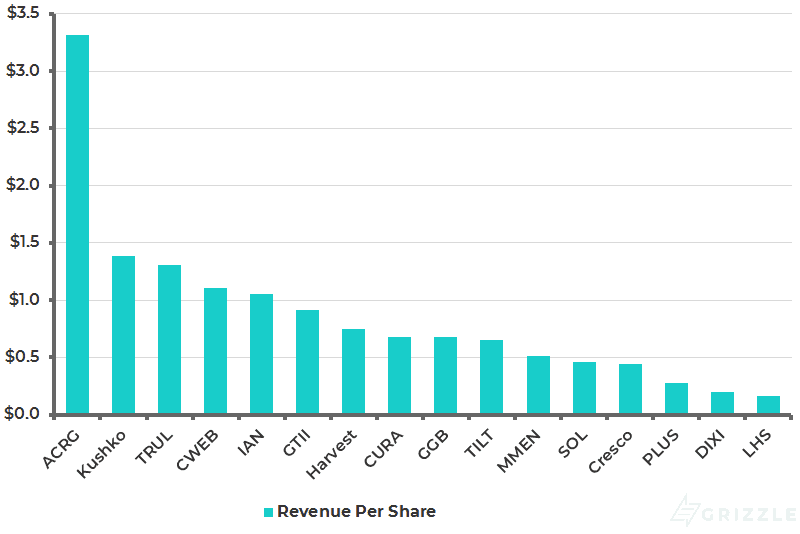

Looking at the fundamentals, Acreage is generating the most revenue per share in the industry and will continue to hold the crown by a big margin as we finish up 2019 even if they dilute shareholders through another capital raise.

With digital advertising largely restricted, the best way to gain cannabis brand recognition is by putting your products in front of customers at a dispensary.

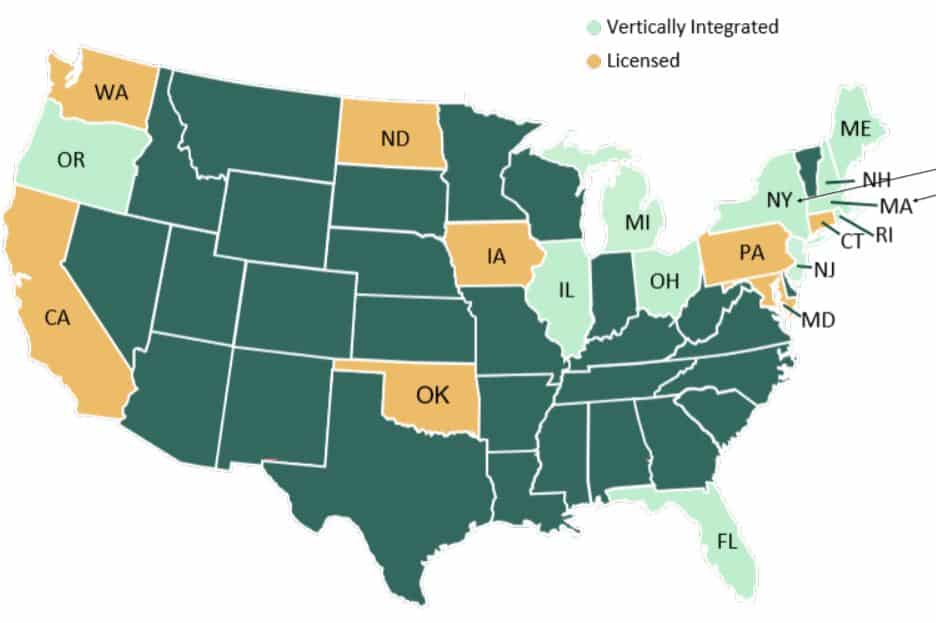

Acreage’s 18 state footprint gives management the best chance among MSOs to become a household cannabis name once the drug is legalized nationwide, potentially in three to four years.

Revenue Per Share Estimated in 2019

What makes Acreage intriguing to us is that the current valuation doesn’t require investors to pay a premium for a piece of this market leader.

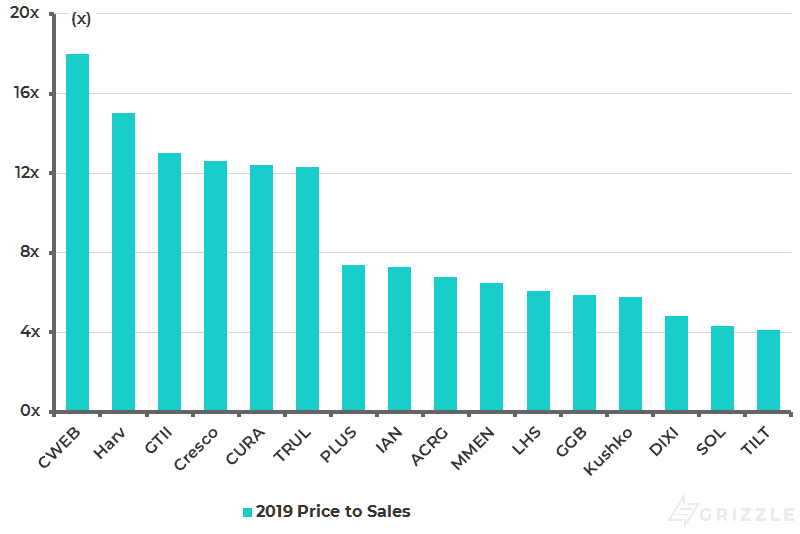

Acreage trades at a 2019 price to sales of 6.8x, a 20% discount to the group average, even though it is a market leader.

A low share count and a reasonable multiple make Acreage an interesting pick for any investor’s watch list.

Further share price weakness could create a solid buying opportunity, especially if the company can actually meet the consensus revenue estimates of $282 million for 2019.

Estimated 2019 Price to Sales Multiple

The company does have a long way to go to meet those consensus estimates generating only $92 million annualized in the fourth quarter of 2018.

Overhead costs are also high as the company scales, and it is not yet generating positive EBITDA, let alone net income.

What Happened in the Q4 2018

Pro-forma revenue of $23 million was up only 18% from last quarter, likely due to a slow dispensary rollout.

The company opened three new dispensaries in the fourth quarter to end the year with 19, but have ramped up store openings with five additional stores open as of March 12.

The new stores imply revenue could be somewhere around $27 million next quarter for growth of 20%.

EBITDA, excluding non-cash items, was a loss of $7.1 million, up from a loss of $2.3 million last quarter.

Acquisitions in Pennsylvania, California, Illinois, Michigan and expansions in Massachusetts and Ohio closed during the quarter.

Liquidity

Acreage has solid liquidity with $254 million of cash and liquid investments.

This cash should last until September 2019 at the current burn and investment rate, meaning the company will likely come to market with a convertible debt or equity deal sometime in the first half of 2019.

The main challenge of owning so many licenses is the large amount of cash needed to build assets in so many states.

Acreage’s celebrity board and deep financial contacts should allow them to fund near-term growth without any hiccups.

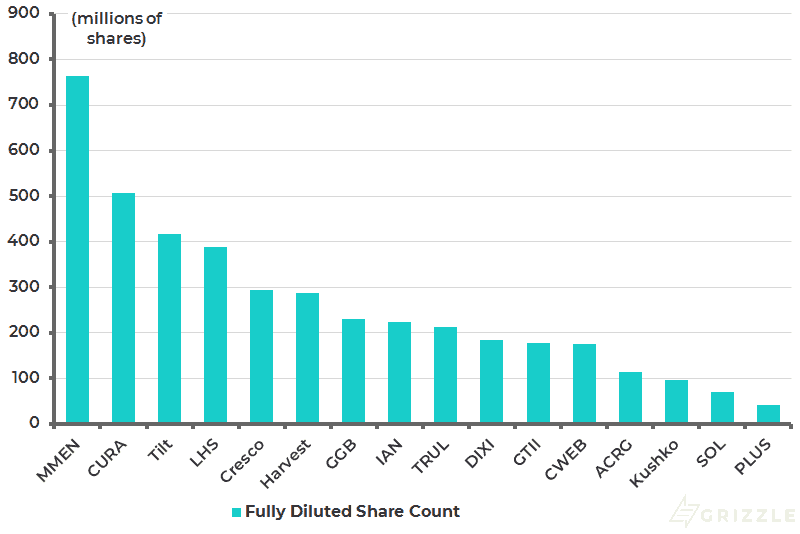

From a fundamental perspective, Acreage has the lowest share count by far among MSOs and will likely see some dilution this year as the company builds out dispensaries and cultivation facilities.

However, even with the dilution, the company still has a low share count, reasonable multiple and massive footprint to leverage over the few years we have left until full nationwide legalization.

Fully Diluted Share Count

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.