Agilent Technologies (NYSE: A) reported fiscal Q1 2020 earnings for the period ending January 31, 2019 beating analyst estimates but softer than anticipated guidance for next quarter is hurting the stock.

The scientific instrument firm reported sales for the quarter of $1.36 billion which came in just ahead of consensus estimates of $1.356 billion. Revenues grew 5.7% compared to the same quarter the previous year, with solid growth across all of its segments.

On the bottom line the company posted earnings of $0.81 per share which beat Wall Street expectations of $0.70 per share.

While the reported quarter performance from Agilent was better than expected, analysts and investors may be disappointed in the updated guidance the company provided for next quarter. The company expects revenues for their fiscal Q2 2020 to be in the range of $1.28 billion to $1.32 billion which is less than the $1.34 billion consensus estimates. On the profitability side the company also provided guidance below expectations, with the company anticipating earnings of between $0.72 to $0.76 per share compared to estimates of $0.78 per share.

After being spun out of Hewlett Packard (NYSE: HPQ) in 1999, Agilent split it’s focus between an electronics measurement business and it’s laboratory instrument business. The company then subsequently spun out the electronics business as Keysight Technologies (NYSE: KEYS) in 2014, focusing exclusively on lab instruments in the Life Sciences, Diagnostic and CrossLab markets.

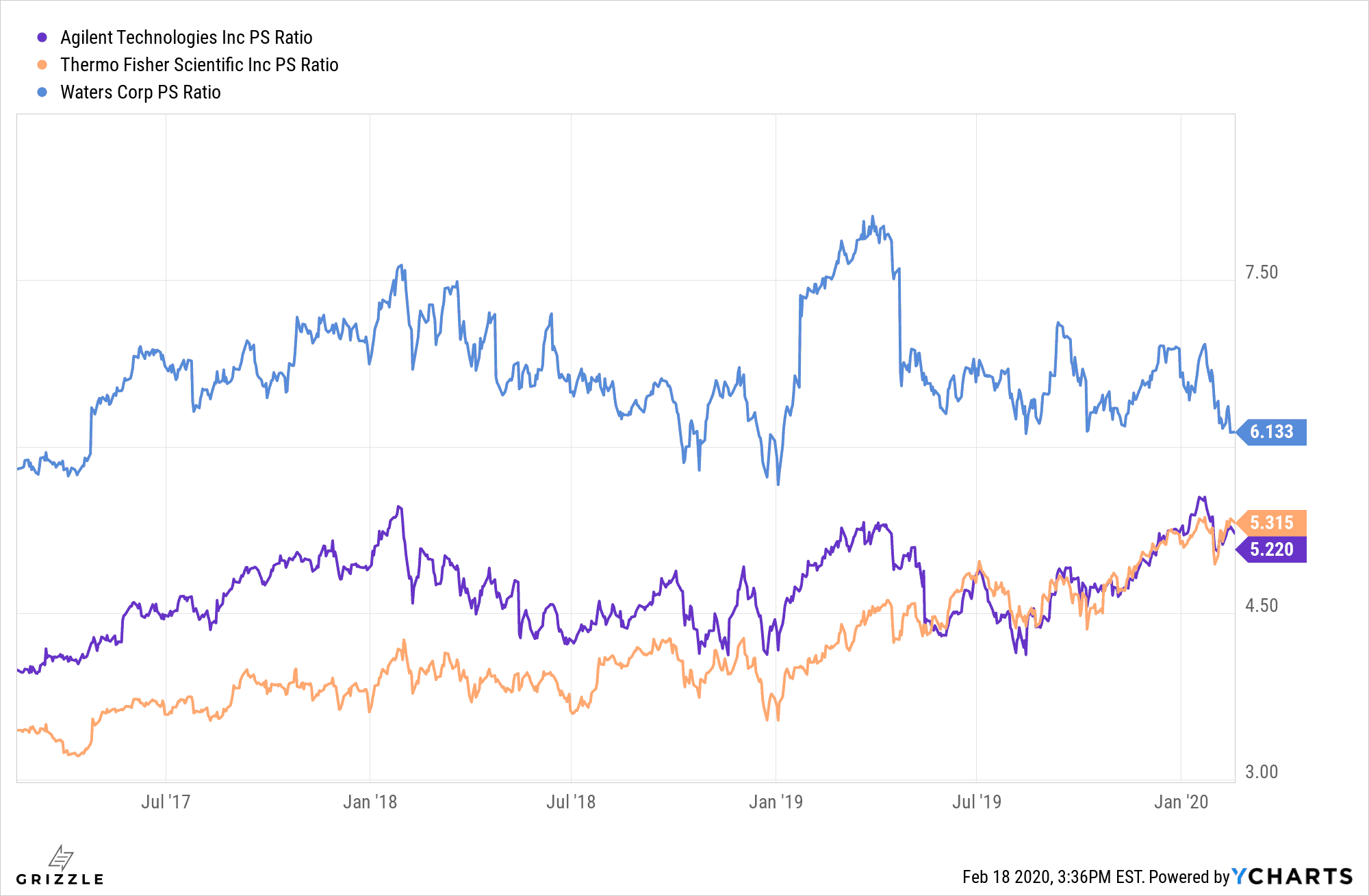

Competition in the lab equipment space is predominantly between 3 big players, Agilent, Thermo Fischer Scientific (NYSE: TMO) and Waters Corp (NYSE: WAT).

Agilent stock performed similar to the overall market in 2019 as it returned 27.5% compared to the 31.5% growth in the S&P 500. In 2020 thus far however, Agilent has been lagging the overall market, closing today down just under 1% year to date. After releasing earnings, the stock was down another 1.2% in after market trading as of the time of publishing.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.