Airbnb is going public this month and has the distinction of being the largest December public offering in what is turning into a packed IPO month.

To get you ready for the stock’s debut we’ve poured over the financial filings to figure out what this company is all about.

We think the pandemic is handing investors a gift with this one.

A true unicorn at a discount.

Let’s Dive in..

Airbnb has Just Cracked the Surface of a Massive Market

Airbnb is just getting started disrupting an absolutely massive market.

Between short-term stays, experiences and the potential for long-term rentals, the market is worth over $1.6 trillion in 2020.

Airbnb’s gross booking value, pre-COVID-19, was $38 billion a year, or only 2.3% of the market.

Airbnb is Just Scratching the Surface

As big as you think AirBnB already is, they are just getting started.

Management is spending lots of money on R&D to figure out how to expand their market opportunity even further and how the team responded to the Coronavirus gives us confidence they will find growth in unlikely places.

COVID-19 Has not Been Kind but Airbnb Surprised Us

Yes, the entire short-term rental business took a hit this year, but the resilience of Airbnb’s business model was on full display.

Offering a private space for families, close friends or individuals has now proven to be a good business model in and out of a pandemic.

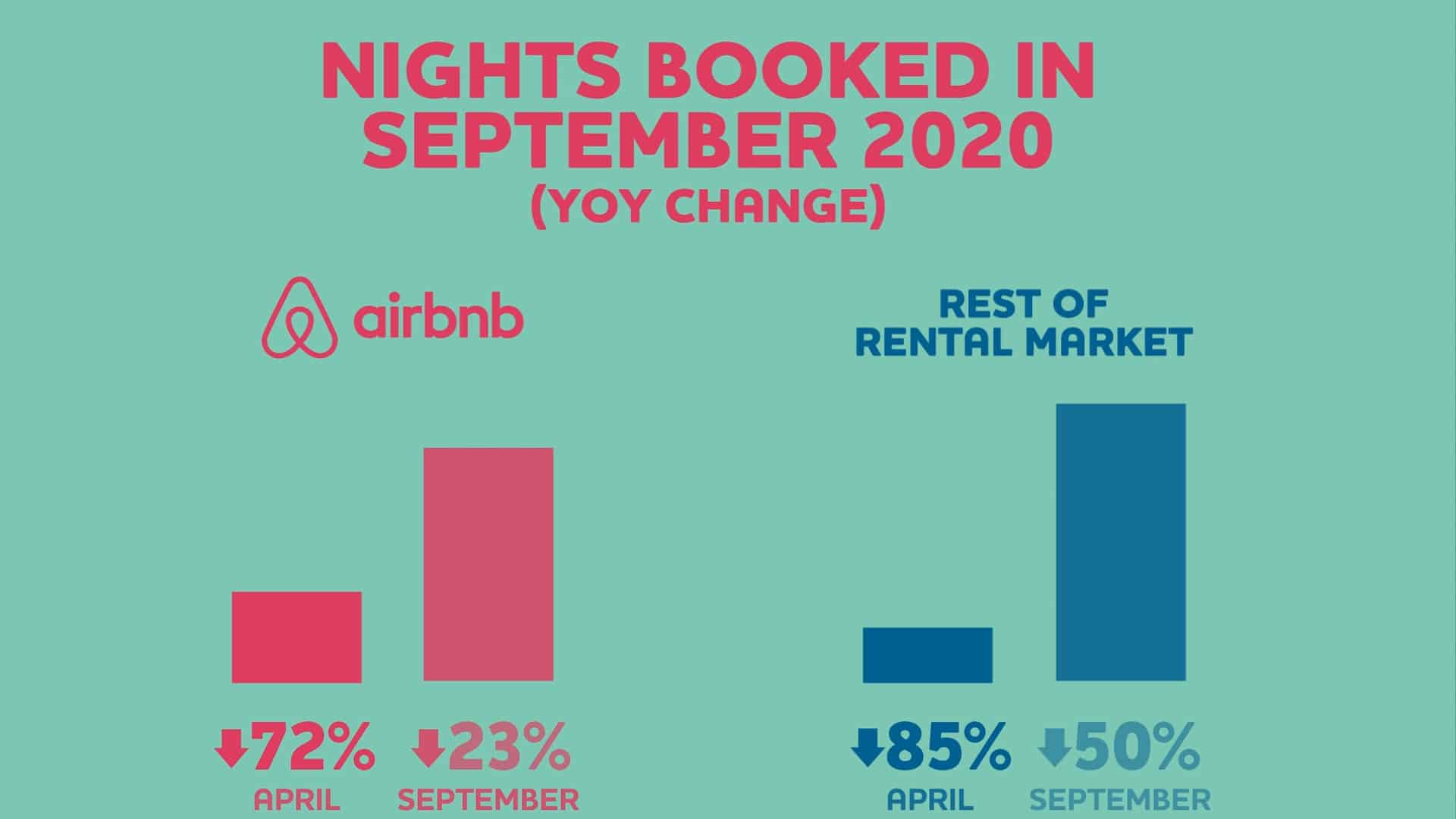

Looking at nights booked, Airbnb suffered just as much as hotels when the world was locked down, however, the rebound has been so much stronger for the company.

As of September Airbnb’s bookings were only down 23% year over year while global hotel chains are still down 50%.

YoY of Nights Booked

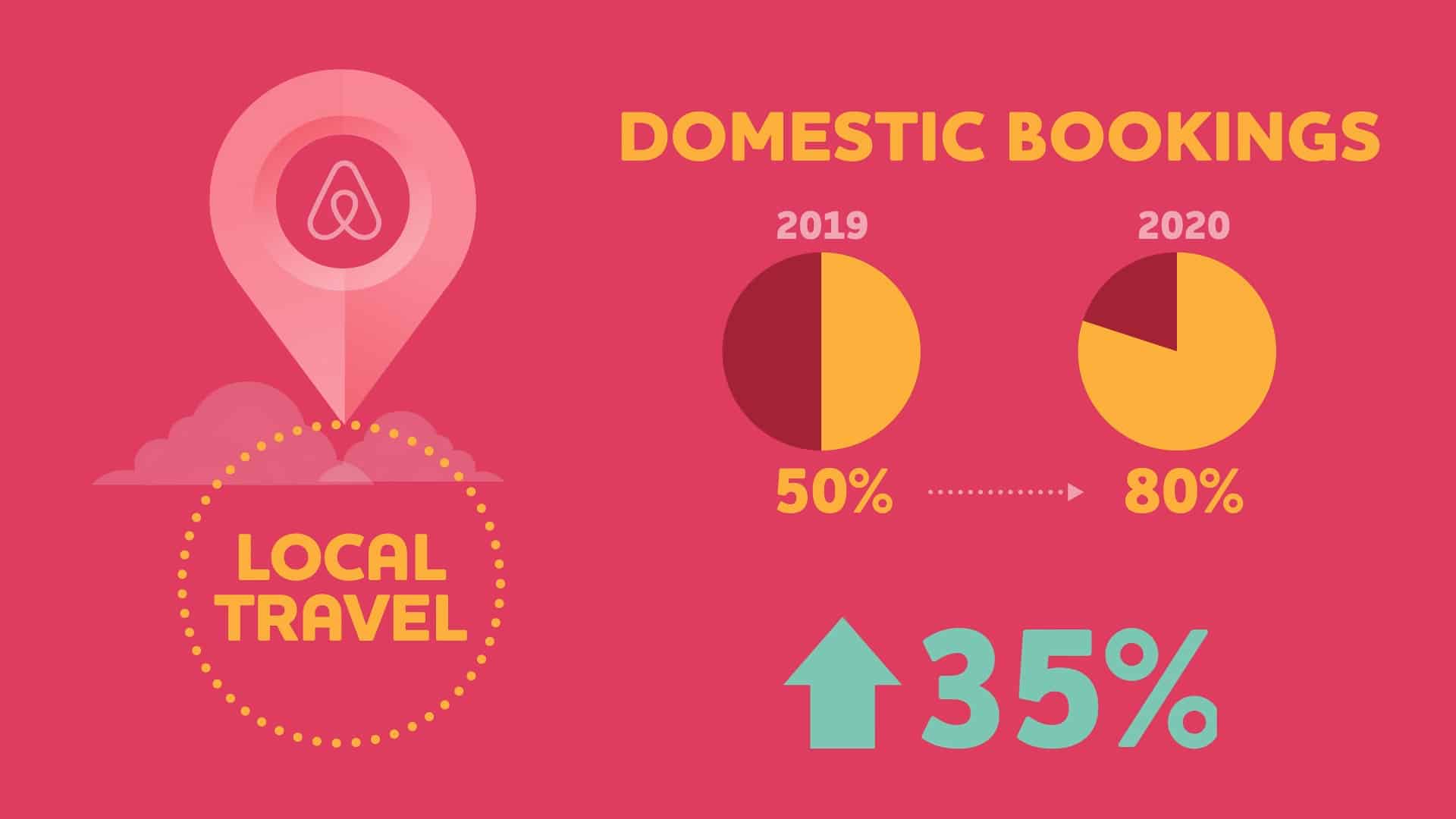

How Did they Do it? Local Travel

Airbnb has been more resilient than traditional accommodation providers because it has a much more diversified source of housing supply.

While hotel chains are clustered in big cities and along travel corridors, Airbnb’s hosts can be located literally anywhere.

Not to mention an Airbnb rental is usually private and does not force you to be among dozens of other guests, which has been a huge advantage during a pandemic.

In 2019 nights booked on Airbnb were 51% domestic, while in 2020, a full 77% of nights have been local or 35% growth year over year.

Local Travel Picked up the Slack for International Travel

Airbnb is unique because its rental inventory truly is the entire global housing market.

The company will keep innovating and finding ways to grow the number of ways consumers will want to interact with the Airbnb platform.

Airbnb is a True Tech Unicorn

The word “unicorn”, was coined in 2013 to describe the rare occurrence of a $1 billion startup.

Now with the market whipped into a cappuccino like froth, $1 billion dollar startups are pretty common.

A $1 billion market cap may now be common but a profitable startup remains the true unicorn.

Airbnb is that unicorn.

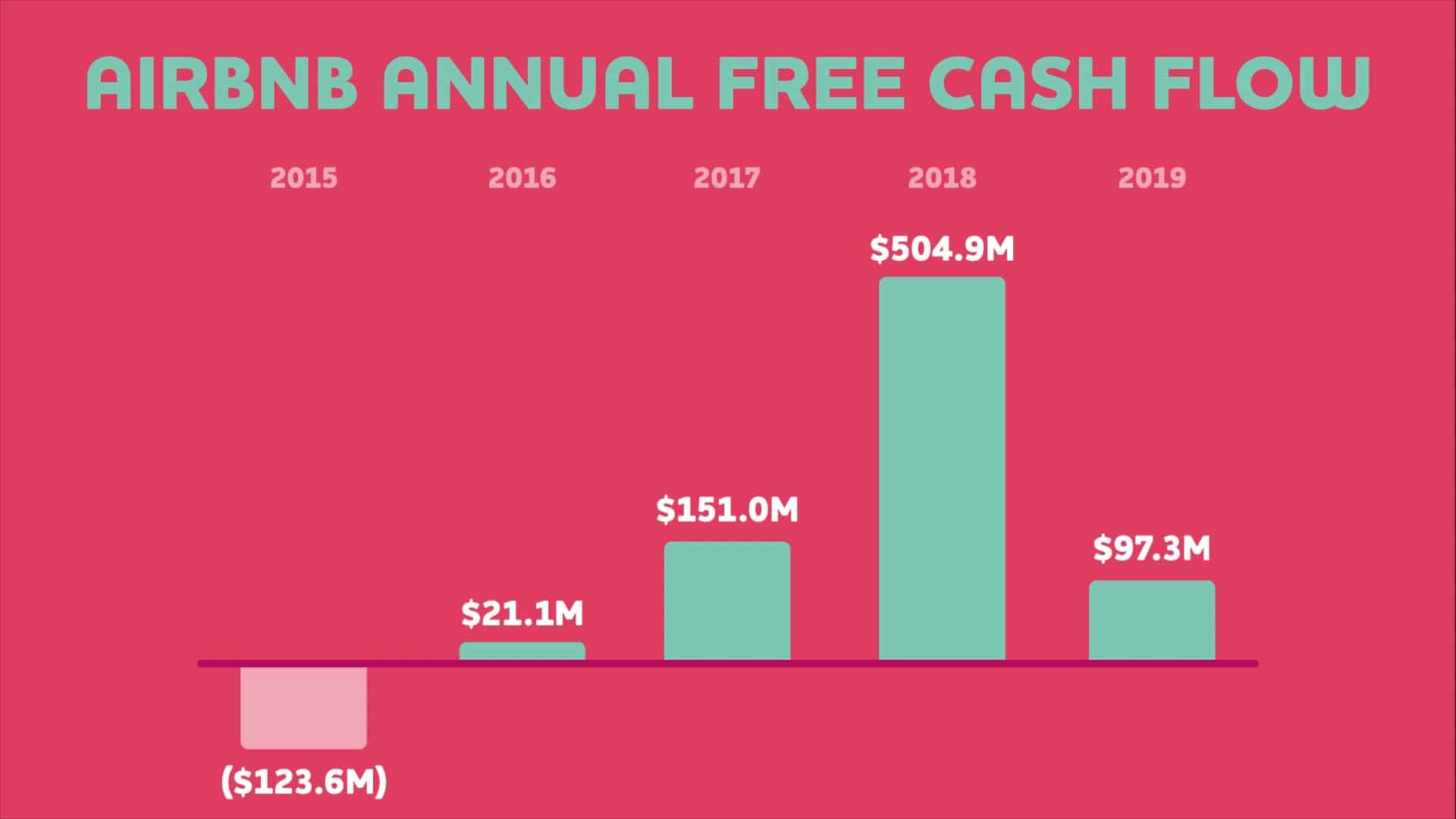

Unique in the startup landscape, Airbnb has been free cashflow positive, meaning there is excess cash after reinvesting in the business, since 2016.  Airbnb has an amazing business model that functions a bit like an insurance company.

Airbnb has an amazing business model that functions a bit like an insurance company.

Customers pay cash upfront for a rental which they may not use until months from now.

In the meantime, Airbnb can invest that cash and earn interest which they keep. They are effectively being paid to borrow money from customers.

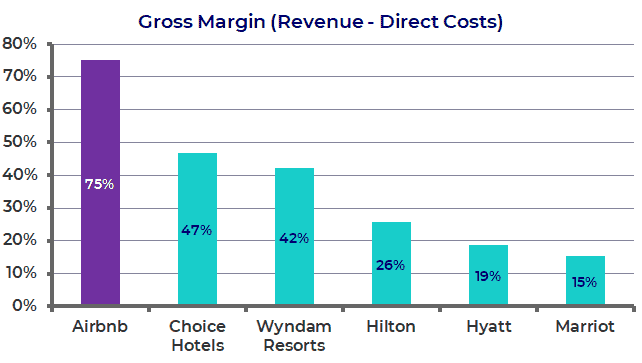

Plus the business is just inherently more profitable than hotels because of the low capital intensity, software not suites.

Gross Margin of Airbnb and Hotels

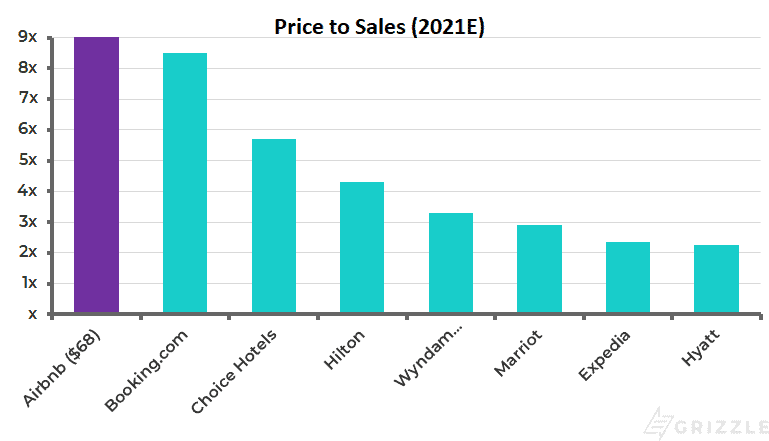

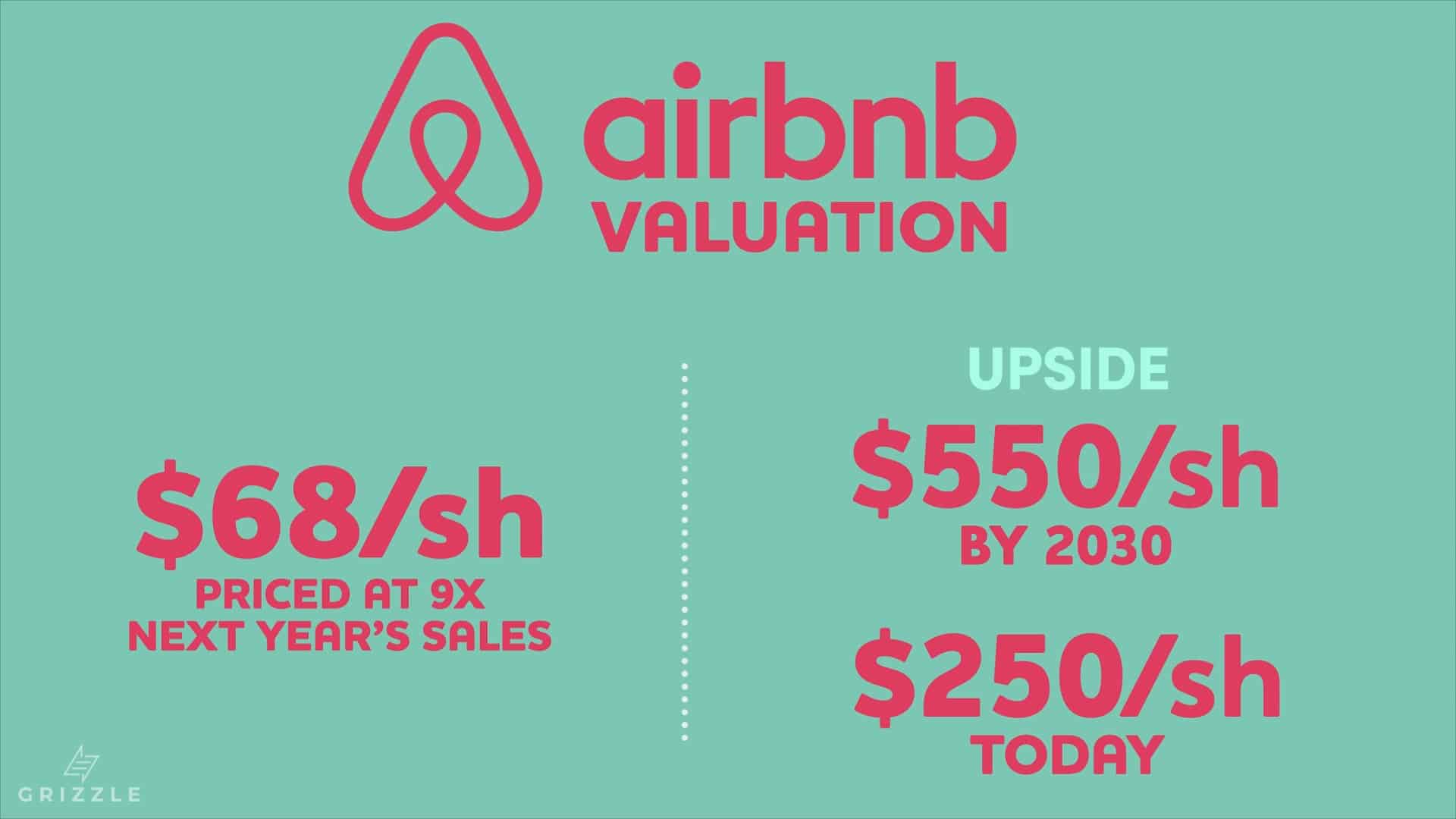

Putting the $68 IPO Price in Context

The latest indications are that Airbnb will price their IPO at $68/sh valuing the company between $41-$47 billion depending on the share count.

Based on our expectations of a 35% rebound in revenue in 2021, the company is going public at 9x next year’s revenue.

9x would make Airbnb the most expensive short term rental stock by about 6%, over main competitor Booking.com.

Even though Airbnb will go public as the most expensive in the group, this is actually a reasonable valuation compared to most other IPO’s this year.

DoorDash, for example, priced their IPO at a 50% premium to the next most expensive competitor and as of today (December 9th) is trading at a 170% premium.

If Airbnb went public in late 2019, the IPO price would have likely been at a much higher premium to all the other competitors in the market, simply because of how hyped this company has become.

Airbnb is Priced Above Hotels and Booking Websites

Airbnb is Worth $550 by 2030 or $250 Today.

Even though the IPO price of $68 is not cheap, we are buyers all day as we think there is significant upside in the stock over time.

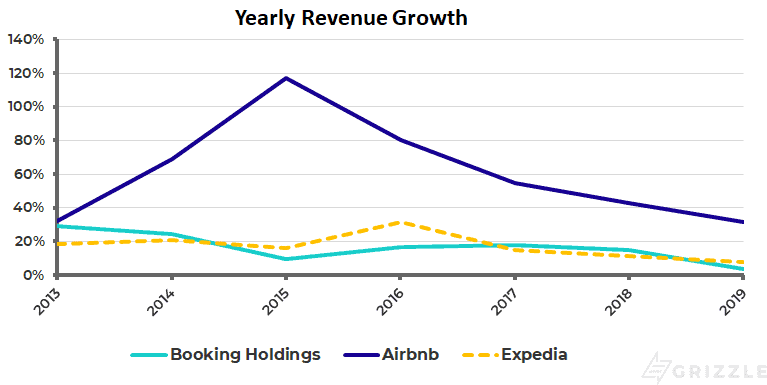

Airbnb has outgrown online competitors Booking.com and Expedia consistently since its founding and growth will continue once we move past COVID-19.

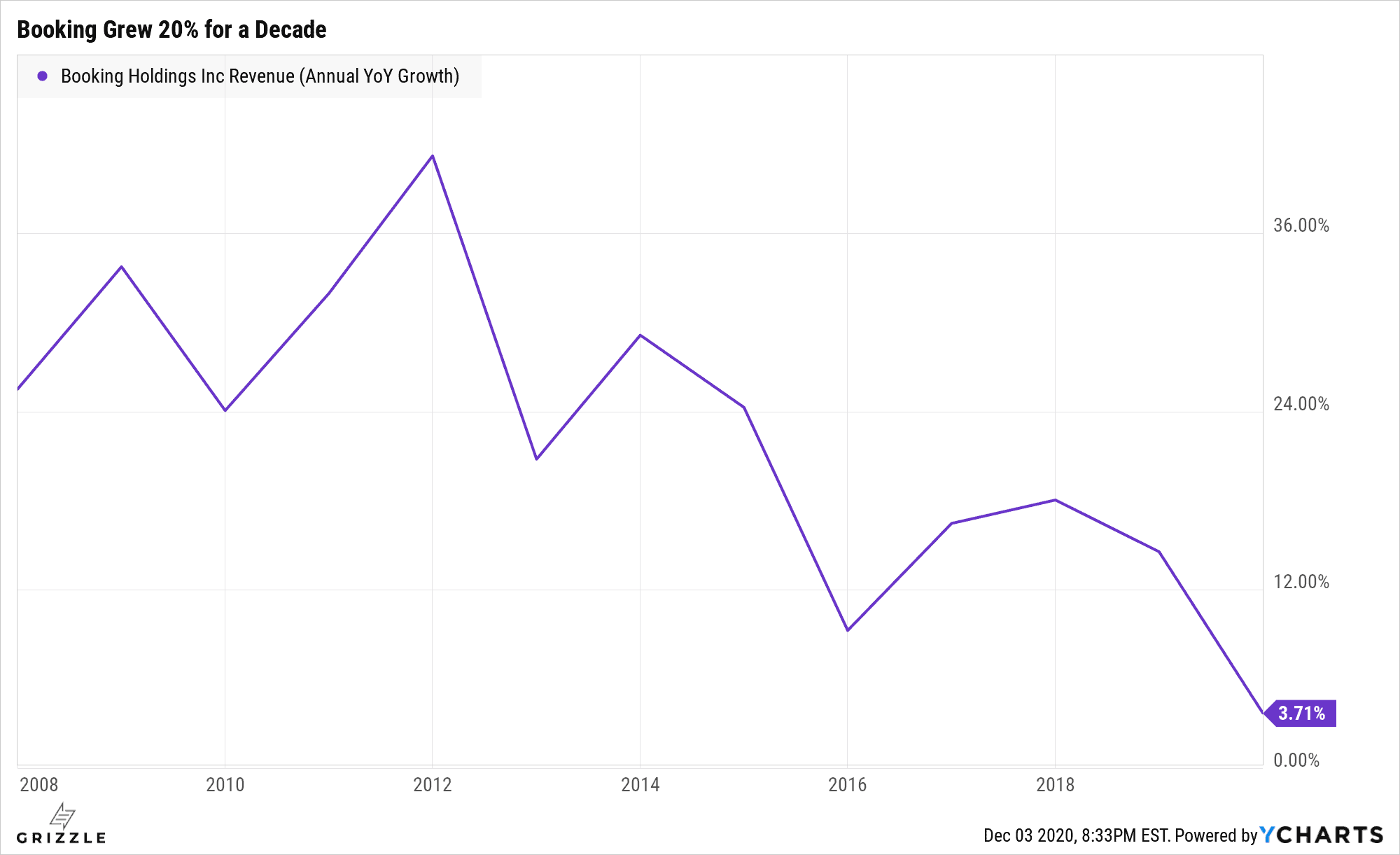

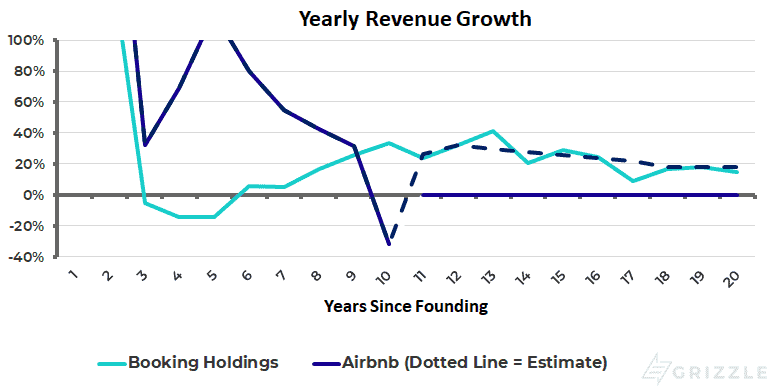

Booking.com is the bogey for Airbnb and the management team there has managed to grow revenue 21% for over a decade.

20% Growth for a Decade

We think Airbnb can do even better given the small slice of the market it currently owns which provides a huge runway for growth.

Management is still experimenting with how to crack the experience and long-term rental market and once they do, growth can easily accelerate.

Airbnb is on a better growth trajectory than booking.com and we think revenue can grow at 35% for the next 10 years, down from 50% on average over the last 4.

Booking.com Compared to Airbnb Since Founding

The upside is so significant here that investors can make money on this stock even if there are growth hiccups along the way.

With the stock worth $250/sh today, we are comfortable buying into the IPO even as it inevitable trades far higher than $68/sh for the first trade.

Grizzle’s Buy/Sell Tool Will Show You The Way

Our visual stock price guide below helps us decide if the stock is too expensive or cheap in any given year as it marches towards our price target.

At the top end of the range is a 7% annual return, or $260/sh today, which is the minimum we will accept for the level of risk inherent in the Airbnb business model.

At the bottom is a 20% annual return, or $74/sh today, a damn good rate of return any investor can be happy with.

In the red zone, Airbnb is a sell as the stock has run too far, too fast.

In the green zone, you are buying all day as the annual upside should be significant.

Buy and Sell Points for Airbnb Out to 2030

Airbnb is not a fad, this is a true disruptor and should be on any investor’s long term buy list.

Airbnb is not a fad, this is a true disruptor and should be on any investor’s long term buy list.

*Assumptions for $550 Price Target

*35% revenue CAGR to 2030

*25% FCF margin in 2030 (25% below Booking.com)

*6x revenue multiple in 2030 (low end of Booking.com range)

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.