Shoot first and ask questions later.

This is the perhaps understandable and certainly predictable response of governments to the emergence of the, by all accounts, highly infectious Omicron Covid variant.

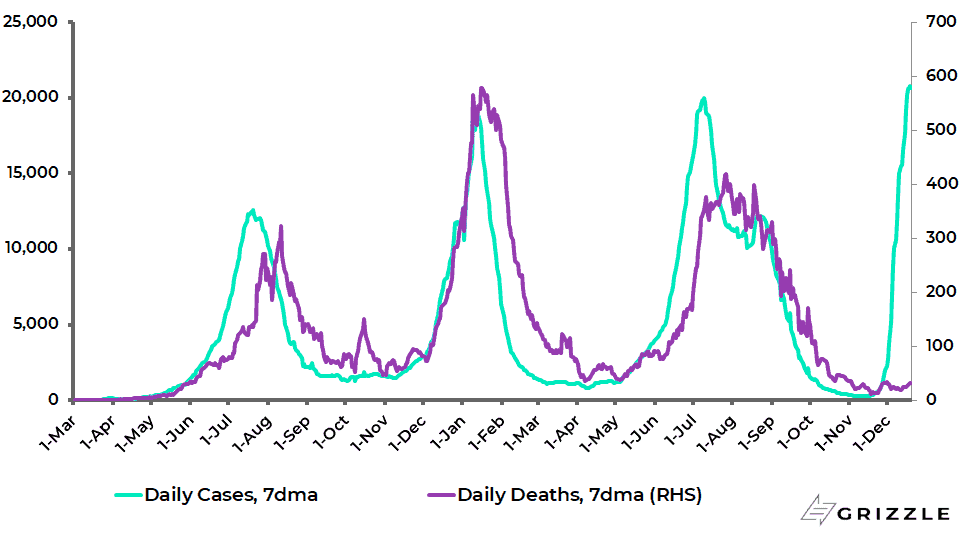

So far it appears, from the South African experience at least, that Omicron is far more infectious than it is deadly.

South Africa 7-day average daily new Covid cases and deaths

Still, it will be a few weeks before the efficacy of existing vaccines against it will have been established, though it is worth noting again that the mRNA technology can be easily tweaked for new variants, with the real bottlenecks remaining regulatory approval and the ability to manufacture at scale.

Meanwhile, if it does turn out to be the case that Omicron is far more infectious than it is lethal, then it will be following the path of most pathogens of getting less lethal over time.

Also, the more people who get infected with the hopefully milder version, the greater the resulting immunity amongst the population at large.

At least such has been the experience in Britain based on official data.

Thus, the case fatality rate in the UK for Alpha is 1.9%, Beta 1.2%, and Delta 0.5%, according to a recent update published by the UK Health Security Agency (see SARS-CoV-2 variants of concern and variants under investigation in England – Technical briefing 28, 12 November 2021).

That means, optimistically, the case fatality rate for Omicron could be around 0.25%.

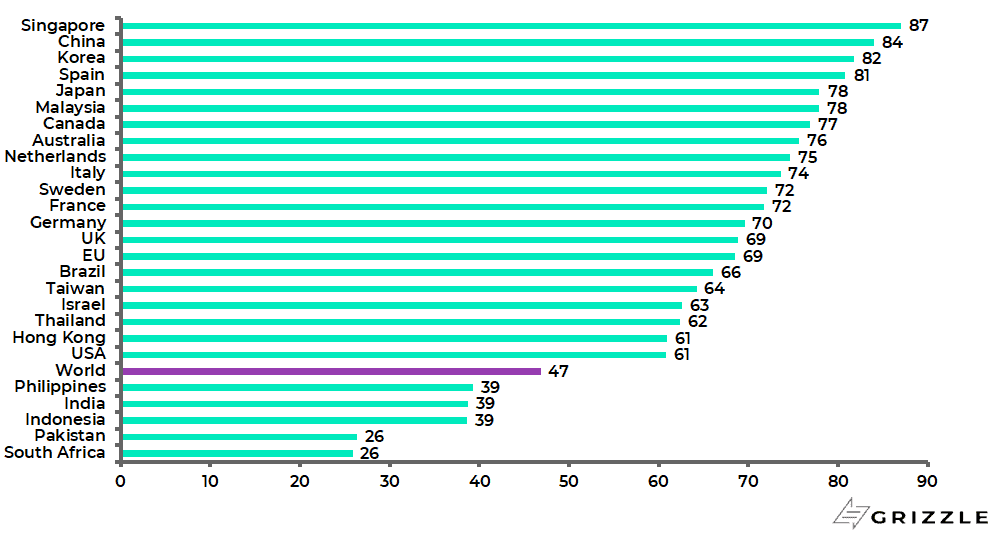

If this is the positive way of looking at the latest turn in the now nearly two-year-long pandemic, it remains the case that the world remains way short of the 90% vaccination rate globally which is probably what is required to defeat the virus once and for all and, in the meantime, these vaccines will need to continue to be tweaked for the new variants.

On this point, only 47% of the world population has been fully vaccinated.

Share of the population fully vaccinated against Covid-19

Still, it is also the case that vaccines are not quite the panacea they were originally made out to be.

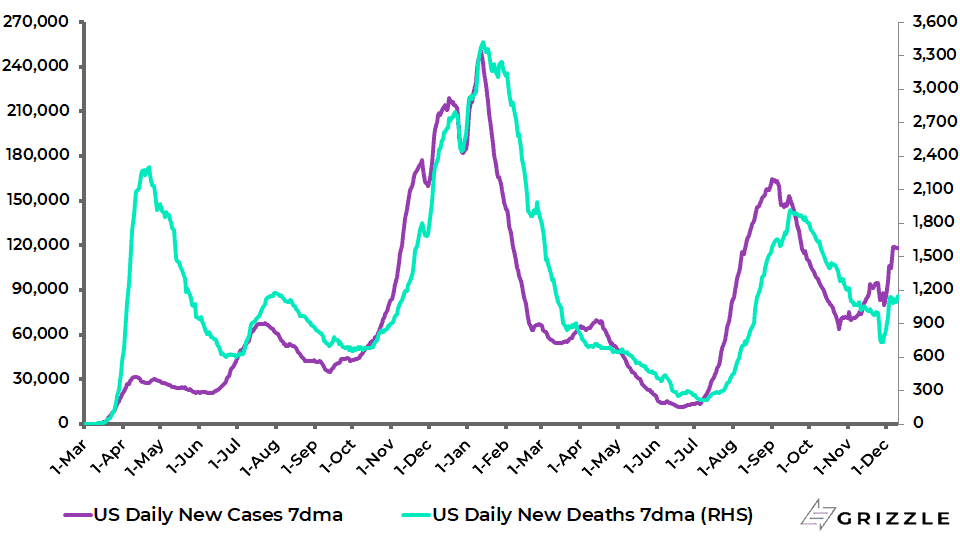

While this writer finds it personally hard to understand the sentiments driving the anti-vaccination movement and has certainly signed up for the jabs for both health reasons and pragmatic freedom-of-movement reasons, it remains the case that more people have died in America of Covid this year than was the case last year, based on the official data.

There have been 441,538 Covid deaths in America so far this year, compared with 361,431 in 2020, according to the Centers for Disease Control and Prevention (CDC).

This is despite the fact that at the end of 2020 only 0.01% of the American population had received two jabs whereas now 61% have.

US 7-day average daily new Covid cases and deaths

Source: CDC

This, in turn, raises the vexed issue of whether Covid has been the chief cause of death or rather an enabling agent where there have been other medical issues.

The fact that vaccines are not a total panacea also is a reminder of the importance of coming up with treatments for Covid, which Pfizer has now hopefully done.

Pfizer CEO Albert Bourla told CNBC recently that Pfizer now expects to manufacture 80m courses of its Covid antiviral drug Paxlovid by the end of 2022, up from the previous goal of 50m.

Watch Long Term Inflation Expectations for Signs of What the Fed Will Do Next

Returning to the markets, this writer has gone on all year about the importance of monitoring inflation expectations in 2021 as providing the best clue as to the timing of any risk-off move in equities triggered by monetary tightening concerns.

This has worked so far in the sense that both the Federal Reserve and the ECB have been about as wrong on inflation as it is possible to be in terms of their inflation forecasts this year.

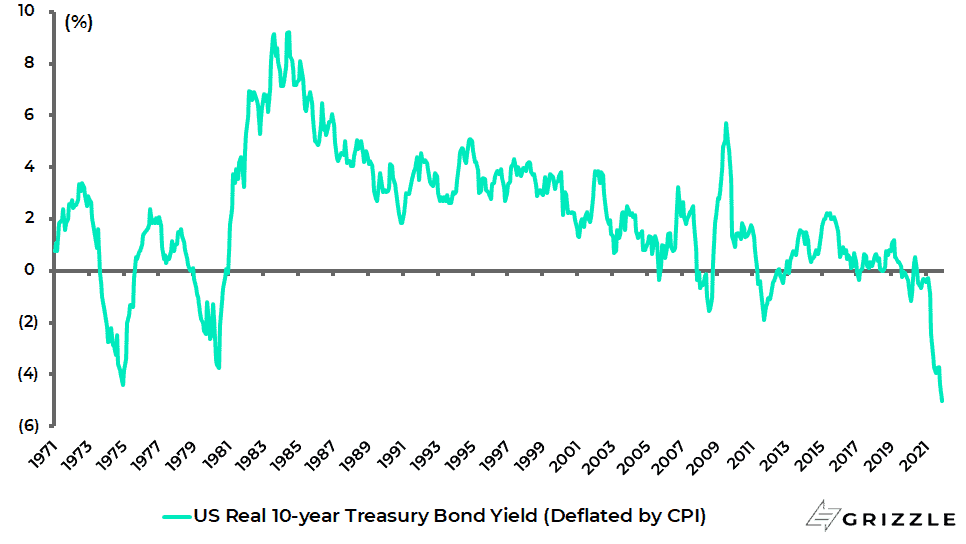

But stocks have continued to rally because the central banks have stuck to their transitory view, at least until Jerome Powell reversed his stance in testimony before Congress on 30 November, as real interest rates have collapsed.

US real 10-year Treasury bond yield (deflated by CPI)

It is also the case that, absent monetary tightening, higher inflation implies higher nominal GDP growth, which is good for earnings.

The reason to monitor longer-term inflation expectations is, of course, because the Fed and the rest of the neo-Keynesian economic establishment dominating central banks, academia, and indeed economists at sell-side firms attribute such importance to them to the extent that the Fed has said that only evidence of destabilised long-term inflation expectations would cause them to become really concerned about inflation.

It is also important to understand that all the above does not mean that inflation expectations are as important a driver of inflation as the central bank establishment appears to believe.

Indeed, this writer’s personal opinion is that this view, more akin to a medieval dogma, is largely nonsense and certainly unproven from an empirical standpoint.

Rather, the most obvious cause of the inflationary pressures seen today is what the vast majority of professional talking heads still fail to mention.

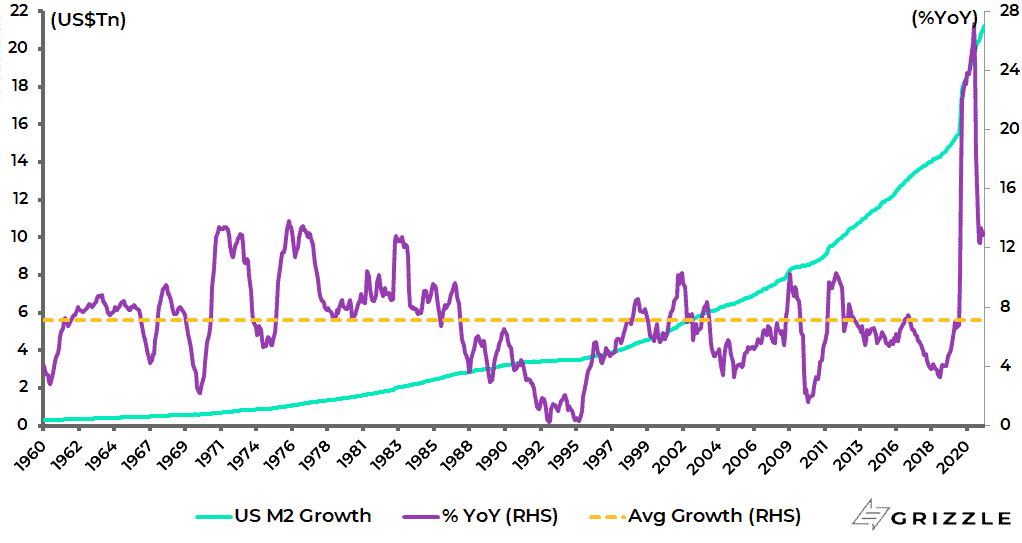

That is the explosive 37% growth in US M2 in the 20 months from February 2020 to October 2021 since the policy response to the pandemic began.

Even now, US M2 still grew at 13% YoY in October, which is way above the average annual growth of 7.1% YoY since 1960.

US M2 trend

Source: Federal Reserve

Doubts Are Even Emerging Within the Fed That Expectations Really Do Drive Realized Inflation

Returning to the inflation expectations issue, this writer’s attention was recently drawn to a Fed research paper published in September written by senior Fed economist Jeremy Rudd, which, interestingly, sought to debunk the established view that longer-term inflation expectations of households and companies play a key role in determining actual future inflation (see Fed staff working paper: “Why Do We Think That Inflation Expectations Matter for Inflation? (And Should We?)”, 23 September 2021).

Rudd writes that a review of the relevant theoretical and empirical literature suggests that “this belief rests on extremely shaky foundations” and that “adhering to it uncritically could easily lead to serious policy errors”.

In this respect, it would be churlish not to applaud the Fed for allowing such an embarrassing paper to be published by one of its own staff, as Rudd is essentially saying that the Emperor has no clothes, which is certainly how this writer has long viewed the G7 central banks.

Still, it should also be made clear that Rudd’s critique does not come from a traditional monetarist standpoint but rather from a conventional neo-Keynesian one.

While his comment that “the economy is a complicated system that is inherently difficult to understand” could have been made by the late and great Friedrich von Hayek, his study displays a conventional neo-Keynesian obsession with the labour market, arguing that the central bank should pay more attention to short-term inflation expectations and developments in the labour market, particularly as regards wage negotiations.

In a discussion of the origins of 1970s inflation in the US, he argues that wages began to respond directly to price movements from around the mid-1960s when the rate of increase in the CPI moved up to around 3%.

Rudd also allows himself a direct attack on the Fed’s recent strategy, post its so-called ‘strategic review’, of deliberately allowing an overshoot of its 2% target.

He writes: “A policy of engineering a rate of price inflation that is high relative to recent experience in order to effect an increase in trend inflation would seem to run the risk of being both dangerous and counterproductive inasmuch as it might increase the probability that people would start to pay more attention to inflation”.

This is, of course, exactly what is now happening.

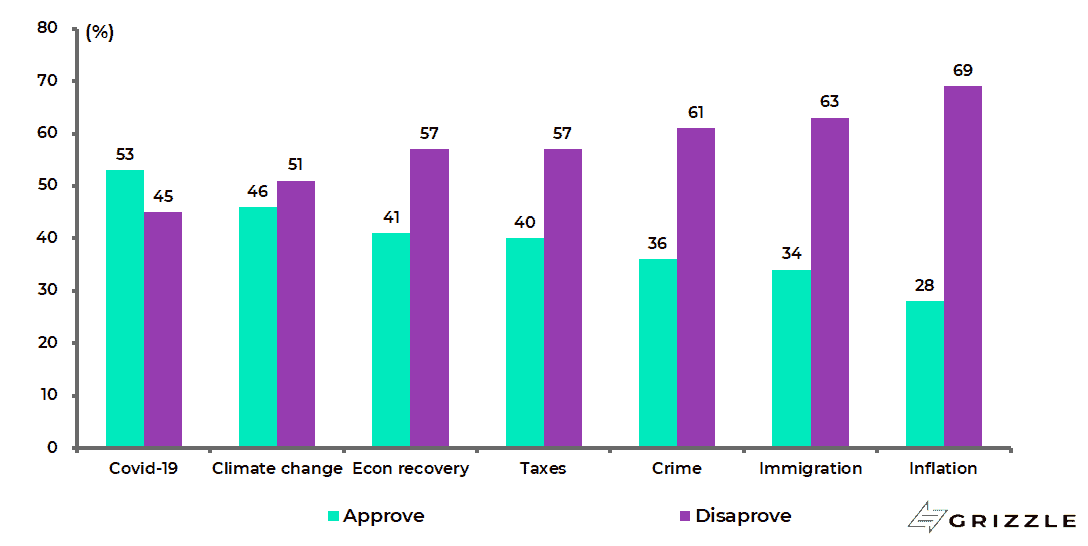

Rising Inflation is Impacting Biden’s Approval Rating

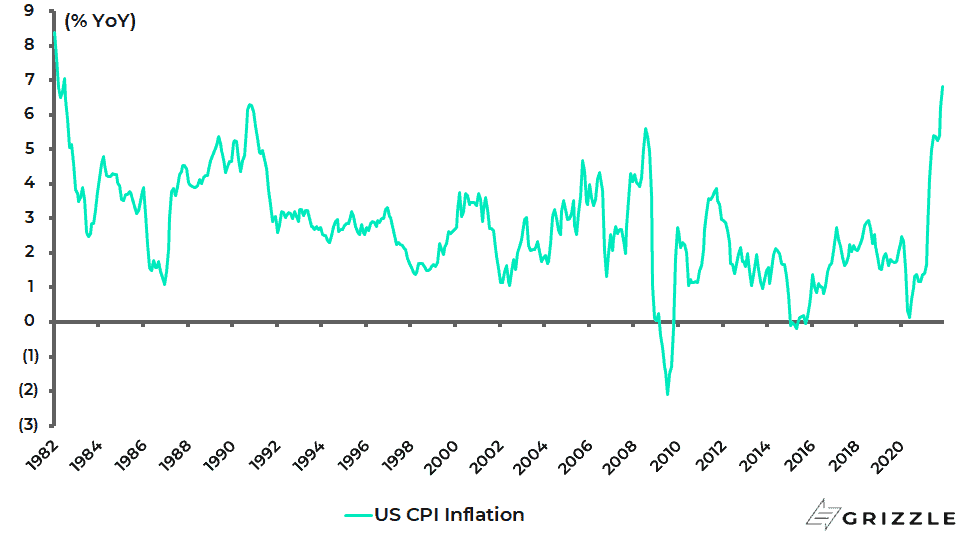

It is also why the inflation issue is fast becoming a political liability for President Joe Biden, as reflected in the latest polling data following the November CPI Report.

The CPI report, released on 10 December, shows that US CPI inflation rose from 6.2% YoY in October to 6.8% YoY in November, the highest inflation print since the Volcker era in 1982 (see following chart).

US CPI inflation

While an ABC News/Ipsos poll conducted on 10-11 December showed that only 28% of Americans approved of Biden’s handling of inflation while 69% disapproved.

ABC News/Ipsos poll: % approve or disapprove of the way Joe Biden is handling …

The views expressed in Chris Wood’s column on Grizzle reflect Chris Wood’s personal opinion only, and they have not been reviewed or endorsed by Jefferies. The information in the column has not been reviewed or verified by Jefferies. None of Jefferies, its affiliates or employees, directors or officers shall have any liability whatsoever in connection with the content published on this website.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.