Altria in Talks with Aphria

The Globe and Mail put out an article (Paywall) today saying that Aphria (Ticker: APH.TO) has been holding partnership talks with cigarette maker Altria (Ticker: MO).

Altria is rumoured to be seeking a direct minority stake in Aphria, similar to the initial investment Constellation Brands made last October in Canopy Growth.

The article goes on to say that Altria would like to acquire a minority stake at first with plans to eventually own a majority of Aphria shares.

The news was received well by both Aphria shareholders and the cannabis industry in general with most LP stocks spiking on the news.

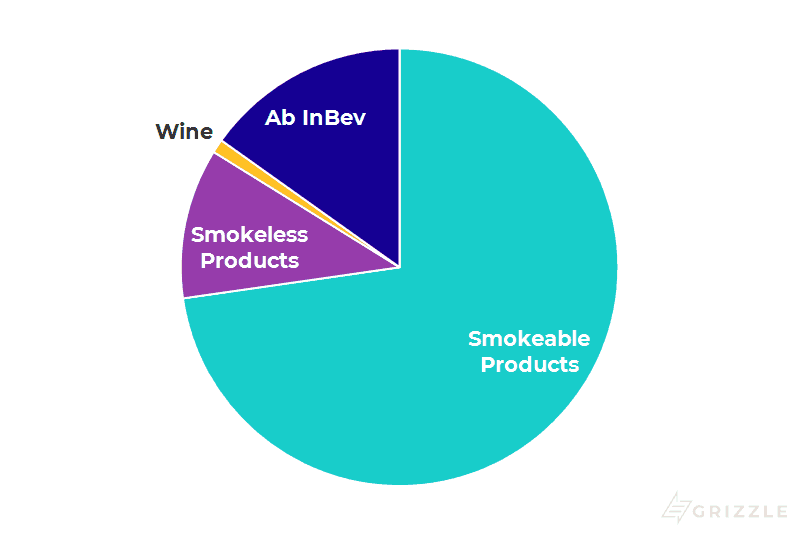

Who is Altria

Altria is primarily a tobacco company, with 84% of operating income coming from cigarettes or smokeless tobacco.

They own cigarette brands such as Marlboro and Parliament and smokeless tobacco brands such as Skoal and Copenhagen.

Altria Operating Income Split

Interestingly Altria also own 10.2% of Ab Inbev, the largest beer company in the world.

We may be speculating but perhaps Altria could be looking to incorporate what it has learned about alcoholic beverages from access to AB Inbev to create cannabis-infused drinks in the future.

A tobacco company buying a cannabis company makes a lot of sense as there is significant customer overlap and Altria customer insights can likely be applied to building a cannabis customer base.

Not to mention Altria has $1.43 billion of cash, enough to buy a 30% stake in Aphria without raising any debt or equity.

An Equity Deal Would Be Only the Second of Many

As we discussed in August when Constellation invested $5.1 billion more into Canopy Growth, every remaining major player is now a buyout target for a consumer company looking to add cannabis to their product portfolio.

Investors have been punishing the stock of companies caught flat-footed when asked if they are looking at the potential of cannabis.

Consumer management teams took notice and are all now circling the cannabis industry trying to figure out the best way to gain a foothold.

We think a scenario where most of the larger cannabis producers are eventually absorbed into larger consumer goods companies is not out of the question.

Deal chatter will continue to support the cannabis sector over the next 12 months in our view and any diversified producer who underperforms the group could be gobbled up for a premium by a consumer products company waiting on the sidelines for the right deal.

There is potentially a valuation floor under any cannabis company with one or more of the following:

- Global distribution

- A brand medical consumers know and a targeted list of recreational brands ready for Oct. 17

- Deep portfolio of infused consumer products and edibles ready to launch in 2019

An Equity Investment Signals Confidence

If Altria, or any other company, does end up taking a stake in Aphria directly, it demonstrates confidence in Aphria’s asset quality and strategic vision.

A company like Altria puts its money on the line only when it knows it’s getting some value in return.

Joint venture deals tell you that both sides are looking to share in the value of any FUTURE intellectual property, while a cash infusion says the outsider wants a piece of the value a cannabis company has already created.

Aphria Remains Best In Class and Will be Swallowed up Sooner or Later

As those who have followed Grizzle know, Aphria is one of our favourite cannabis companies because it’s led by a management team with the most successful business track record in the industry, has the lowest cost structure, and focuses on profitable growth, not just growth at any cost.

Aphria is an attractive takeout target whether or not Altria is the buyer. The longer Aphria is left to execute and grow, it only means a more expensive price to pay for any suitors.

In the interest of full disclosure, employees of Grizzle personally purchased and currently own stock in Aphria, Inc. See the Content Disclosure section here on our Terms and Conditions page for more details.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.