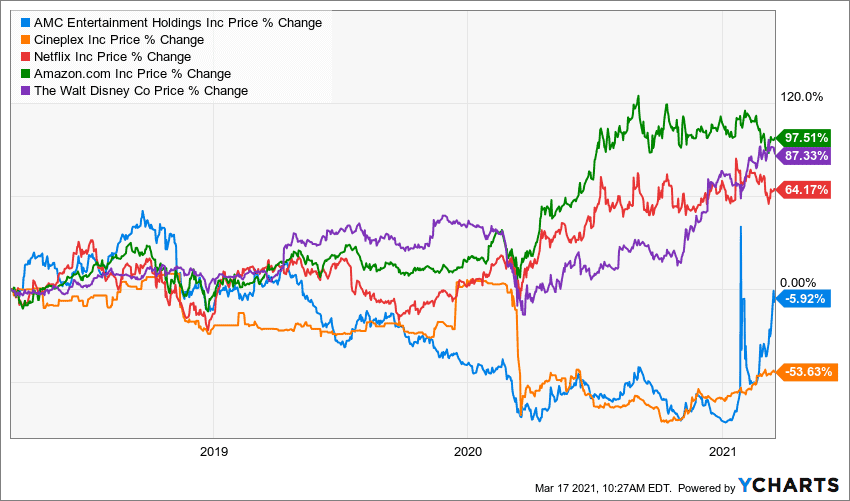

AMC Entertainment Holdings (NYSE:AMC) share price has been steadily declining over the last several years, which is no surprise given the rise of at-home streaming options such as Netflix, Amazon Prime and Disney+.

https://youtu.be/gu7LUbUCcms?t=1558

Traditional Theater Operators vs. Online Streaming Services

AMC is not unique in its fall from grace, other traditional movie theater companies such as Cineplex and Cinemark have suffered a similar fate.

Cineplex is currently suing Cineworld, a UK movie theater operator, after a merger deal fell through in large part due to the ongoing COVID-19 pandemic.

So, with COVID-19 lockdowns and revenues down ~90%, why are we even talking about AMC?

First off, RUMORS.

Last year, rumor had it that Amazon may acquire AMC. The original article featuring this speculation appeared back in May 2020 and more recently, a translation of an article from Forbes France spiked investor interest briefly.

Upon further inspection, it is clear that no new information was being provided in the French article and all speculation remains based on rumors from the original May article.

But the stock did rally as uninformed investors jumped on the bandwagon and pushed AMC’s stock price to a high of $20.36.

Second, Reddit.

Reddit posters/traders are at it again. This time they’ve set their sights on AMC and have played a large part in the stock’s upward price momentum.

It seems the rationale is that once COVID-19 lockdowns cease, people will flock to movie theaters and revenues will soar.

The problem is that AMC was barely making money even when there wasn’t a pandemic to worry about.

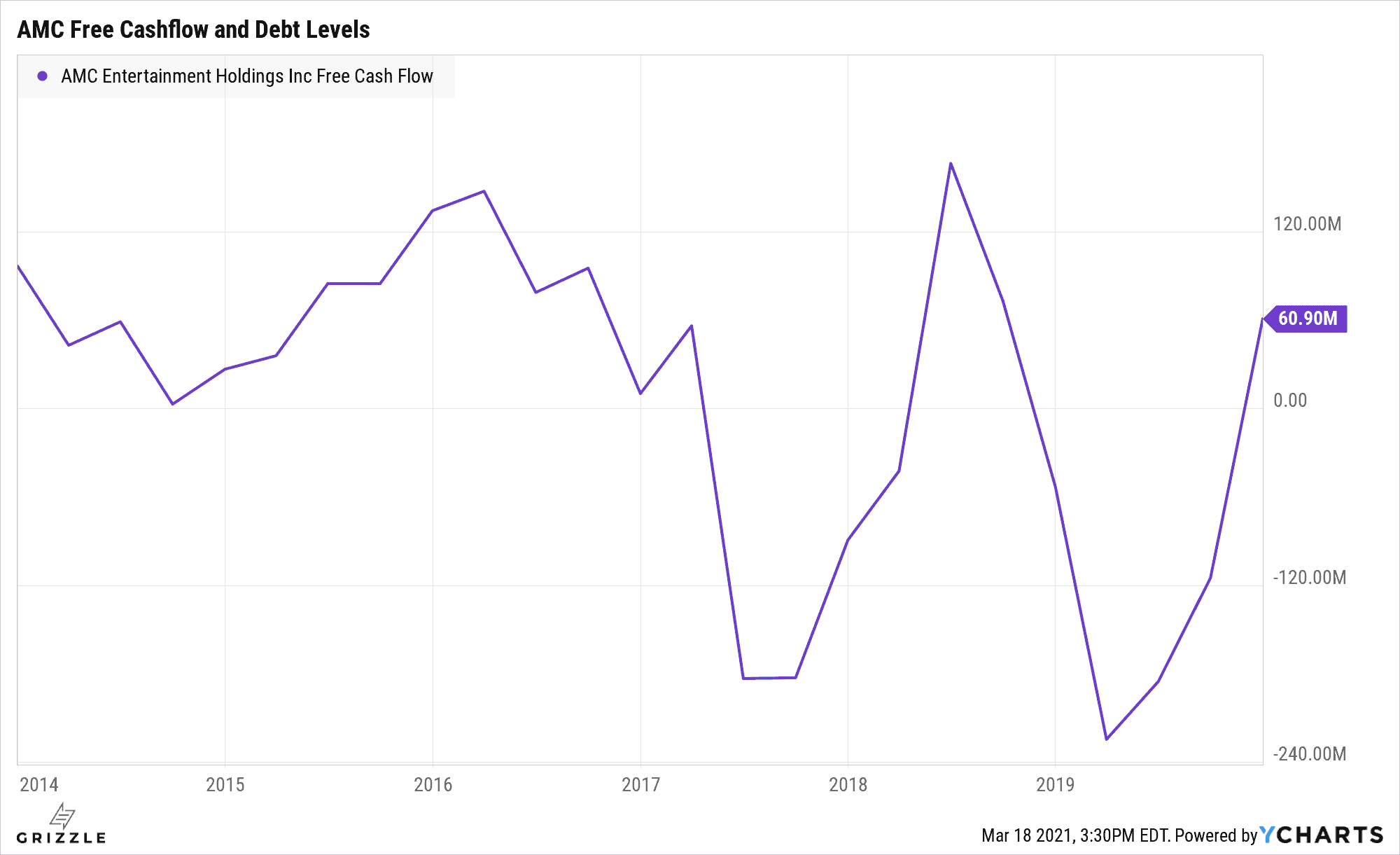

Even in a good year AMC only generated $50-$100 million in free cashflow.

AMC Free Cashflow by Year

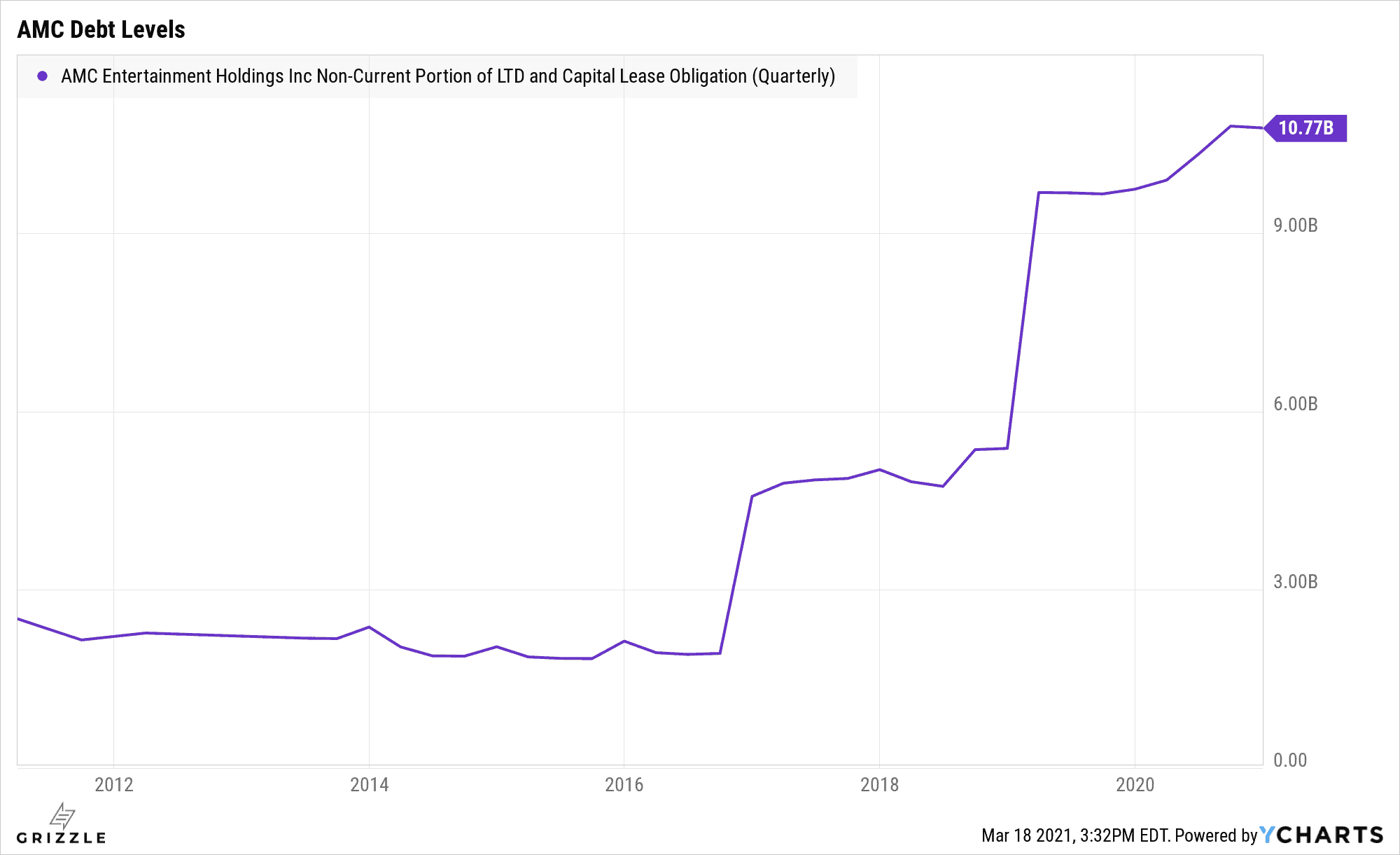

and debt levels have been rising, hitting a decade+ high of $11 billion due to the pandemic.

$100 million of free cashflow is barely a drop in the bucket compared to $11 billion of debt that will have to be repaid in the next five years.

AMC Debt is at a Decade High

Is AMC a Good Investment or just a WallstreetBets YOLO?

Before we jump into the numbers, I’d like to note that one of the company’s largest stakeholders, a Chinese conglomerate founded by a Chinese billionaire, has reduced its position from more than 30% in early December to less than 10% as of March 3 according to Forbes.com.

But what do Chinese billionaires know?

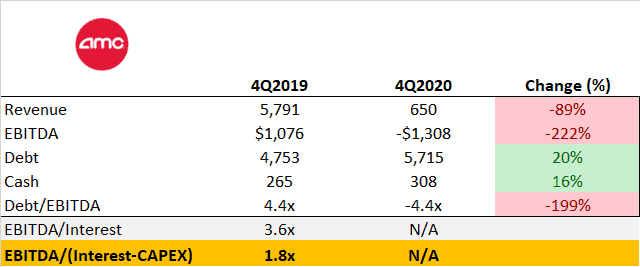

Looking at AMC’s financial position before the pandemic hit compared to today, we see a company in much worse shape.

The company added 20% more debt while revenue fell 90%.

AMC Financials Pre-Pandemic and Today

http://www.ycharts.com

To keep the lights on (a.k.a. not go bankrupt) a company needs to be able to pay its debt on an ongoing basis.

This means paying the required interest and the money that was originally borrowed, called principal.

All debt eventually matures, so paying interest is not enough if you can’t eventually come up with the cash to pay off your debts.

AMC can pay off the debt balance in one of three ways:

- Use cash on hand if there is enough (which there is not)

- Issue more stock and use the resulting cash. This only works if the market will buy all the stock without the stock price crashing below $1/sh.

- or lastly, refinance the maturing debt into more debt.

Selling assets is out of the question considering AMC owes at least $3 billion more than all their assets are worth.

Refinancing the debt will also still lead to bankruptcy.

The new debt will have a higher interest rate than the old debt, meaning interest costs will go up and up, taking away more of the free cashflow until the company has no way of paying off the debt and eventually has to default anyway.

This leaves stock issuance as the only way out, but first, we have to talk about AMC’s ability to service its existing debt.

Pre-pandemic, AMC had an EBITDA to interest payment coverage ratio of 3.6x.

But EBITDA does not account for reinvesting in the company. Reinvesting includes fixing physical assets, for example, broken seats or carpets that need to be replaced, etc.

Without reinvesting the business revenues will eventually go to zero because the service being provided will no longer generate income (i.e., people will not pay to go watch a movie in broken seats).

Taking minimum reinvestments into consideration, AMC was at a 1.8x interest coverage ratio pre-pandemic – not so good.

So even as we come out of the pandemic and consumers return to movie theatres, AMC will generate far too little cashflow compared to the debt it owes.

AMC looks headed for a reckoning even if they survive the global pandemic.

When will AMC Go Bankrupt?

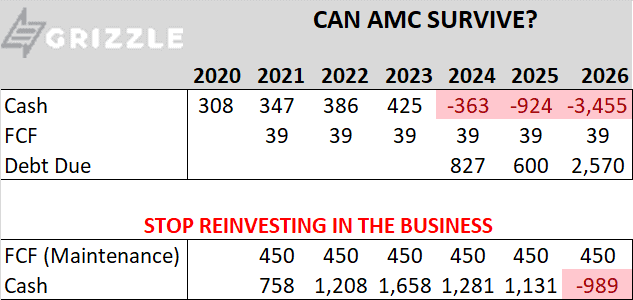

Looking at AMC’s debt maturity schedule, we can see the reckoning still has a few years to play out.

AMC is on track post-pandemic to file for bankruptcy by 2024, give or take a year or two.

AMC Forecasted Debt Maturity and Cash Balance

As I mentioned above, there are several ways to kick the can down the road (put off paying the debt they own), the can pay from cash on hand (not possible for AMC), issue more stock (only works if there are willing investors) or get more debt to cover current debt (only works if there are willing lenders).

Given the company’s dire straights we think the only way out will be through issuing more stock.

However, for AMC to pay off debt coming due in 2024-2026 management would have to issue 250 million shares at the current stock price of $14.00/sh.

250 million shares would be a 56% increase to the share count, absolutely crushing current investors.

Without a retail investor rescue, AMC is on track to become the next Blockbuster Video.

Final Thoughts

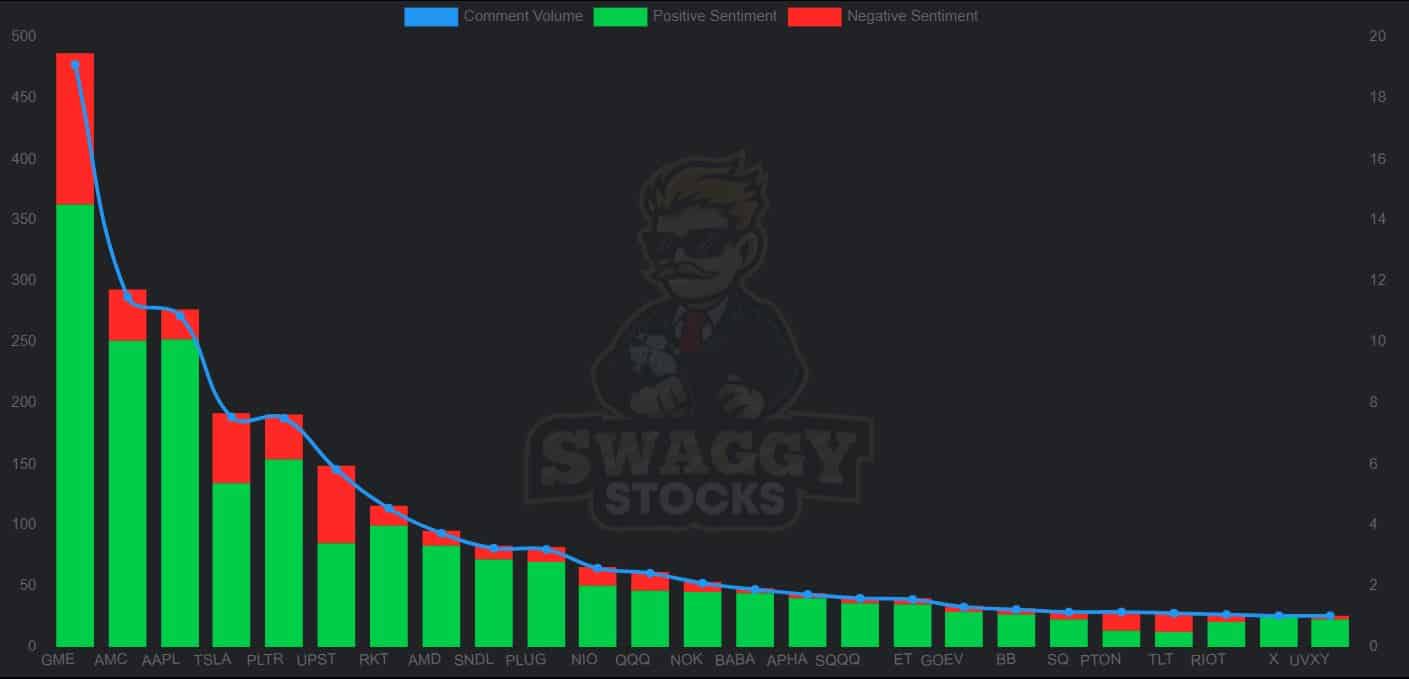

The WallStreetBets crew has taken a liking to AMC, taking a stock only months from filing for bankruptcy to pre-pandemic highs.

Most Comments by Ticker on WallStreetBets Reddit Channel (AMC #2)

The higher stock price has let management raise some cash and likely survive the pandemic.

But with almost no cash coming in and big slugs of debt due in 2024, 2025 and 2026, AMC is either headed for bankruptcy or will dilute shareholders by 35%, tanking the stock price.

If you join the WallStreetBets crew on the AMC rollercoaster just know you have entered the casino.

The longer you play, your chances of losing money approach 100%.

Disclosure: The author had no position, short or long in AMC at the time this article was published.

More disclaimers can be found HERE

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.