Bottom Line

There’s no getting around the fact that it was a messy operational quarter for Aphria, however investors received very good news about the underlying value of the business.

A reevaluation of the LATAM assets decreased the carrying value by $50 million but still found these assets are worth more than Aphria originally paid.

This reevaluation effectively debunks the most important short seller allegation, that the LATAM assets were worthless.

Putting the LATAM controversy to bed should remove the last cloud hanging over the stock since the short report was released.

Aphria’s recent win as one of only three producers licensed to grow cannabis in Germany reinforces the fact Aphria is a top class producer to be taken seriously.

Aphria represents a very attractive target for a CPG company looking to buy into cannabis at a big discount or for another licensed producer coveting their international footprint. On this front we are encouraged by the addition of former Whole Foods Co-CEO Walter Robb to the board of directors.

The bottlenecks and supply issues Aphria experienced this quarter are not unique and are part of the industry-wide scaling problems faced in the early months of legalization.

Aphria has approved capacity of 115,000 kg scheduled to start up before everyone else and plants in the ground as of March 8 leading to much higher revenue and significantly lower growing costs in the first fiscal quarter of 2020 (ending August 2019).

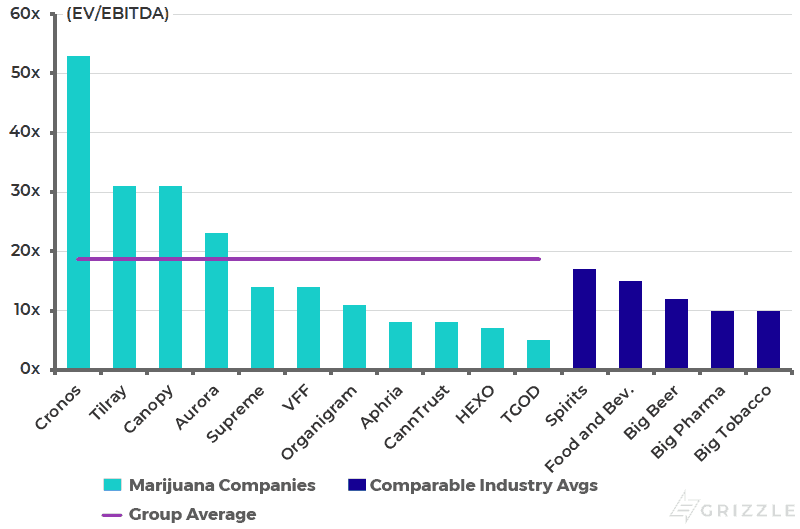

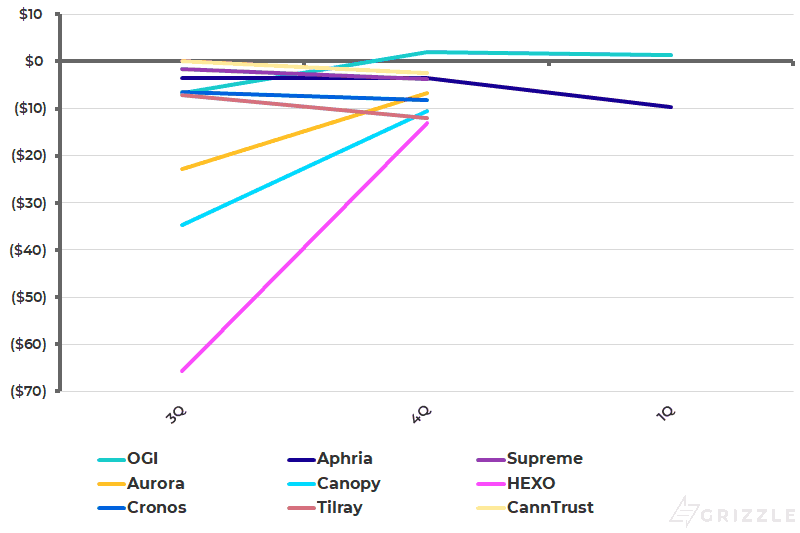

With all allegations in the short report debunked, a new management team at the helm and a stock trading at an unwarranted 70% discount to similar-sized peers, we believe the market will arbitrage away this extreme valuation disconnect.

We believe a hedged trade of long Aphria and short Aurora is one of the most attractive risk/return propositions in the cannabis market.

2020 EV/EBITDA Among Canadian Cannabis Producers

Operational Overview – Aphria’s Cannabis Production in Need of a Boost

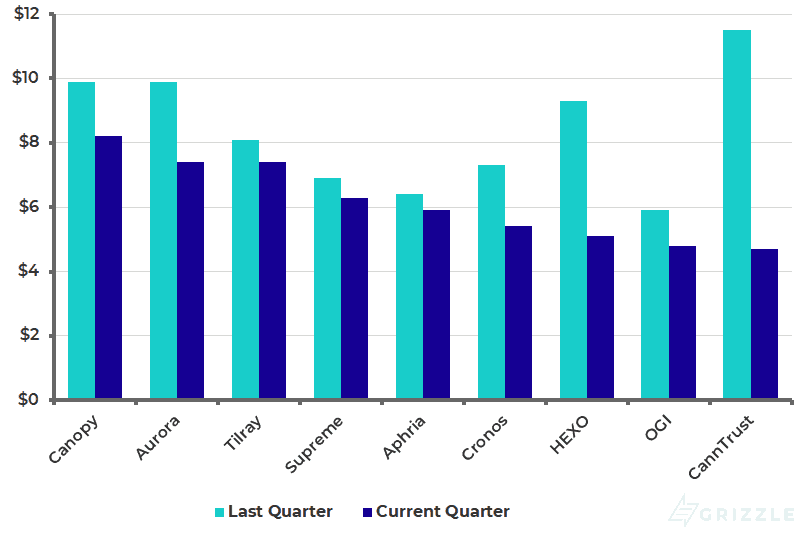

From a cannabis production viewpoint, Q2 2019 is a quarter Aphria would like to forget. Revenue fell ~30% QoQ to $15.4 million from $21.6 million. This stemmed from disappointing cannabis sales, which saw a 20% drop to 2,637 kg from 3,408 kg. Overall, Aphria’s revenue per gram of $5.90 leaves them directly in the middle of industry peers.

These disappointing results are likely due to the time-consuming ramp-up of production and the challenges that come with scaling distribution. With plants now in the ground, the 1Q 2020 reporting quarter which ends August 2019 should show significant improvements across the board.

Revenue Per Gram of Cannabis Produced

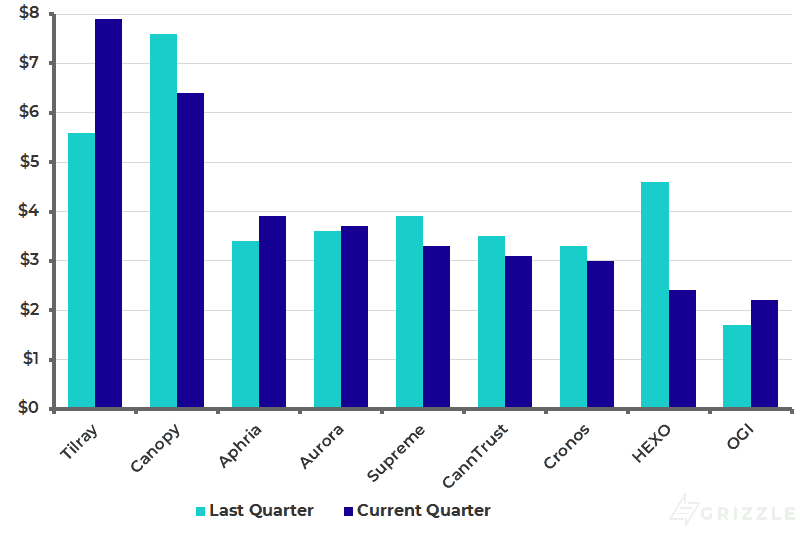

Aphria’s production was achieved with costs of $10.1 million, a 12% drop quarter over quarter. The smaller drop in cannabis production costs compared to the drop in kilograms sold arises from the higher per gram costs of growing in Canadian winters.

Overall, their per gram production cost of $3.9 is on the higher end compared to other Canadian LPs. However, we expect these numbers to drop once their production capacity fully ramps up within the new Aphria One facility.

Last quarter management warned the market that a new growing technique and preparations for ramping up Aphria One would lead to a $0.50 per gram increase in growing costs.

This increase will reverse over the next 9 months as Aphria One reaches full capacity causing growing costs to fall meaningfully.

Production Costs Per Gram of Cannabis Produced

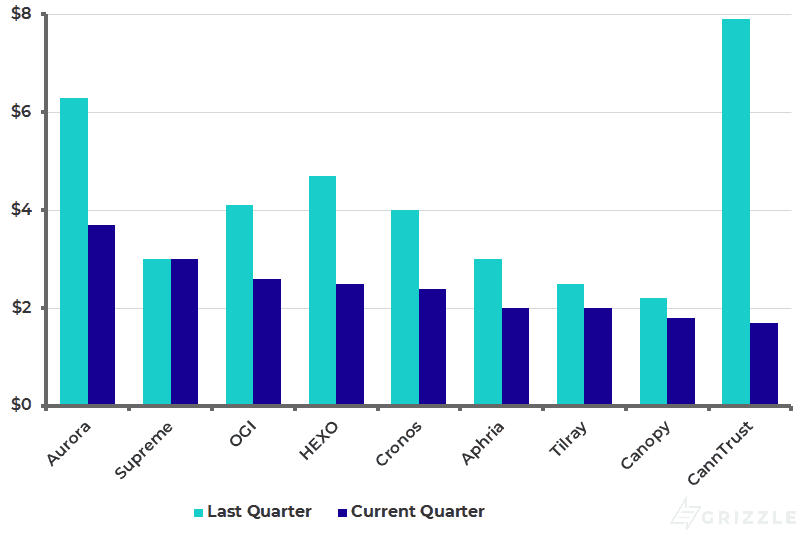

As would be expected with reduced production, gross margins saw a ~50% decrease quarter over quarter from $10.1 million to $5.3 million. This leaves them with a gross margin per gram of $2.0, tied for third lowest gross margin among peers.

Once Aphria Diamond is fully operational by August 2019, gross margins will rebound significantly.

Gross Margin Per Gram of Cannabis Produced

In the end, Aphria had EBITDA of -$24.1 million, twice the loss from last quarter’s -$12.2 million. This was good for an EBITDA per gram of -$9.15, leaving them near the middle of the pack among peers.

Aphria ramped up spending a quarter later than peers so likely reached peak EBITDA burn this quarter.

EBITDA Per Gram of Cannabis Produced

Overall, Aphria had a quarterly cash burn rate of $69 million from operating and investing activities. When you consider their cash and equivalents of $224 million, the company has adequate cash to reach profitability in late 2019 as the Aphria One greenhouse reaches full capacity.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.