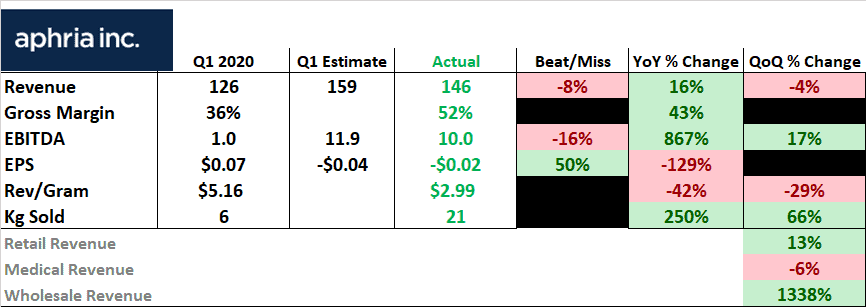

Aphria reported disappointing revenue that missed expectation by 8% and was also a decline from last quarter.

The market hates declining revenue in what should be a high growth industry and sold off the stock hard as a result.

EBITDA (a proxy for cashflow) is improving, but is growing slowly and remains at low levels compared to the margins US cannabis companies are generating.

The one bright spot was the volumes of cannabis sold in the quarter.

Earnings Results vs Market Expectations

Aphria sold 66% more cannabis by weight than they did only 3 months prior, a strong result.

Aphria definitely grabbed some market share from competitors, but these market share gains came at the expense of profitability.

Most of the incremental sales were for large form factor, discounted flower, driving revenue per gram down hard.

Revenue per gram fell 30% in this quarter alone and is down 42% from the same time last year.

Rising volumes and falling prices largely offset each other leading to a modest 13% quarterly increase in retail cannabis revenue.

This is the major problem Aphria faces.

When your retail and wholesale prices are in freefall you are swimming against the current.

Margins are shrinking unless you are cutting costs every single month.

The Canadian cannabis market is facing an issue the U.S. growers do not yet have to deal with.

There are Better Deals Elsewhere

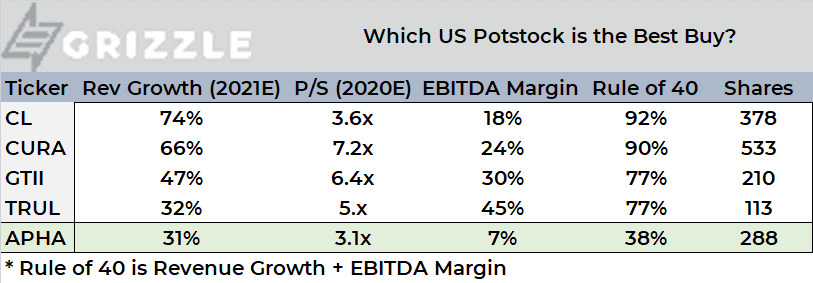

Aphria may be putting up the best results among Canadian growers, but you as an investor can buy any legal cannabis stock you want, not just the Canadian ones.

When looking at the profits, growth and future opportunities for U.S. operators, Aphria start to look a lot less compelling.

Why would you buy Aphria when for the same multiple of revenue you can own Cresco Labs (Ticker: CL) growing at 74% with twice the margins of Aphria.

You could also pay a reasonable premium for Green Thumb (Ticker: GTII) and own a business growing 50%, with ample cash and 4x the margins of Aphria.

Aphria doesn’t look so great if you simply expand your investing horizon.

Aphria vs US Cannabis Stocks

What to Do With Aphria

If you are an investor who absolutely refuses to own non-Canadian Cannabis stocks you have only one option to protect yourself from the industry’s troubles.

A pair trade.

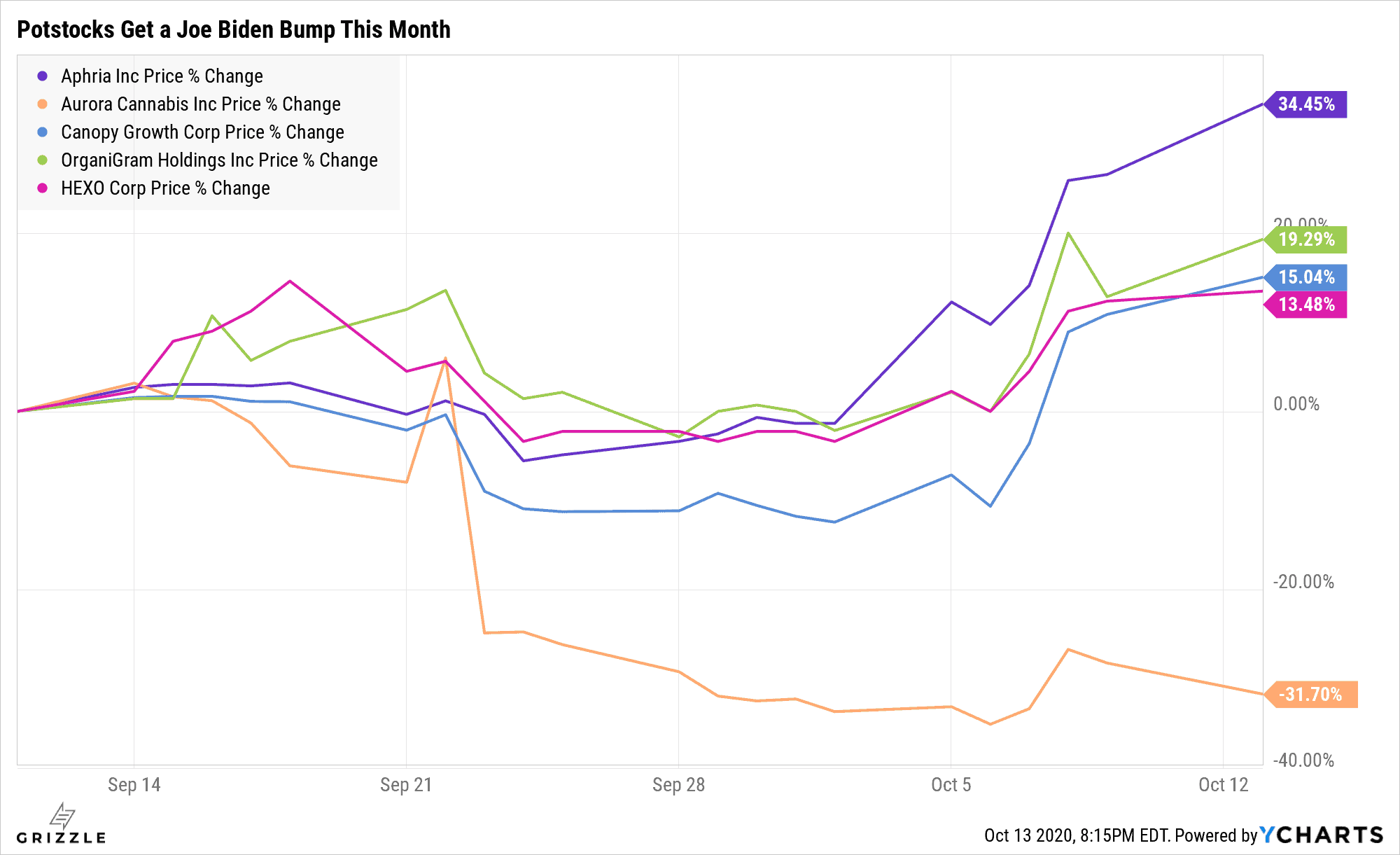

Aphria still makes sense as your long position (the stock you own) with the stock putting up the best performance in the group YTD.

Owning APHA, Selling Others Worked Great in 2020 So Far

The second part of a pair trade is to pick a cannabis stock that is in trouble and sell it short.

This leg of the trade protects you from an industry selloff.

Our top two options remain long Aphria, short Aurora or Canopy Growth.

If this all sounds too complicated, we would agree with you, but otherwise you are at the mercy of a Canadian cannabis market with retail prices in freefall.

Until the market consolidates (companies buy each other) and prices stop falling, Aphria may be a winner in Canada, but will ultimately be a loser in North America.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.