Bottom Line

The market is not going to like a revenue decline and 60% cut to yearly guidance — expect weakness today.

However, the guidance cut reflects unrealistic expectations by management more than any deterioration in the fundamentals of Aphria’s business.

Aphria (TSE: APHA; NYSE: APHA) remains the best positioned Canadian licensed producer, with a business that is already profitable and guidance of $38 million in EBITDA this year compared to peers that are still deep in the red.

Most importantly Aphria has the cash to survive the coming market distress and can be opportunistic with acquisitions if the right asset comes up for sale.

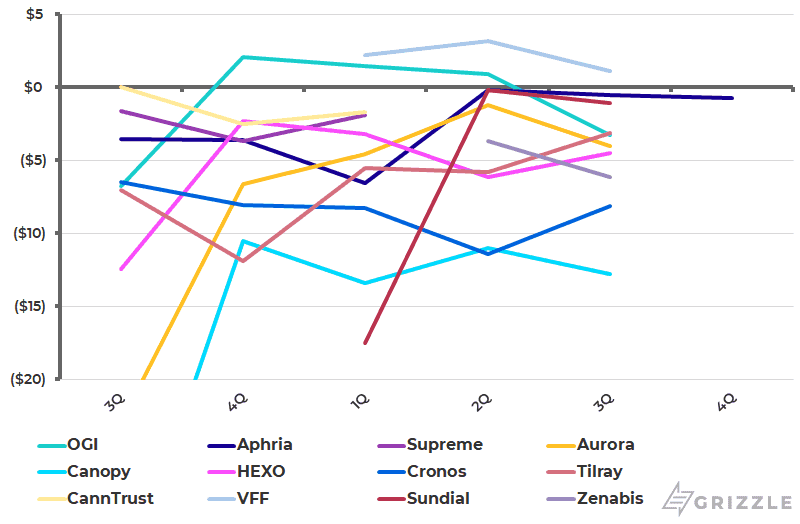

Aphria also has arguably the most beloved cannabis brand with Broken Coast, an advantage they are already leaning on in the medical market to push revenue per gram up 8% in the quarter while pricing is falling across the board for everyone else.

Bottom line, if you continue to invest in Canadian licensed producers, Aphria is the one to own and will continue to attract both retail and institutional investors due to its profits, capacity, low cost, and piles of cash.

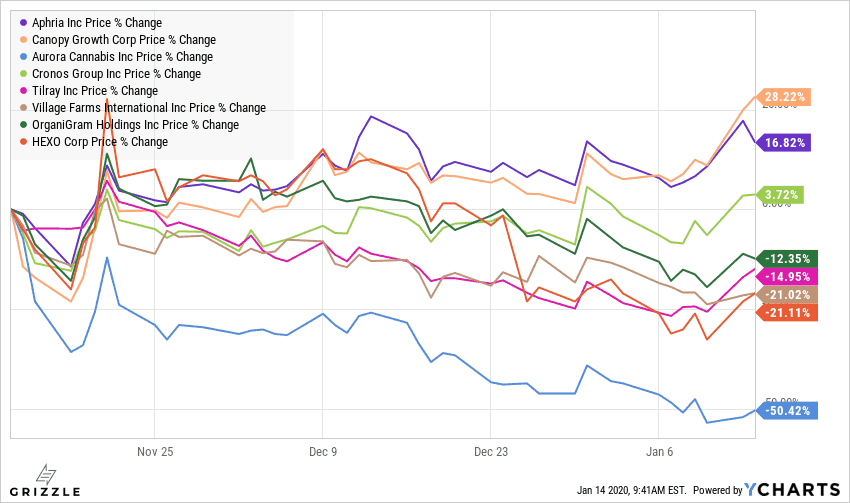

Aphria Will Continue to Outperform in 2020

Operational Overview – Slow and Steady Progress

Just as the distribution business made the cannabis business look better in good times, it can also make it look worse in bad times.

Falling distribution revenue dragged overall revenue for the quarter down 4% even though the cannabis business grew by 9%.

Revenue growth is slow leading up to the roll-out of Cannabis 2.0, but starting with next quarter we expect growth will pick back up.

Revenue per gram was down 7%, but within that mix Aphria was the only company able to push up medical prices in the quarter.

This was due to strong demand for their Broken Coast brand, a favourite among Canadian consumers.

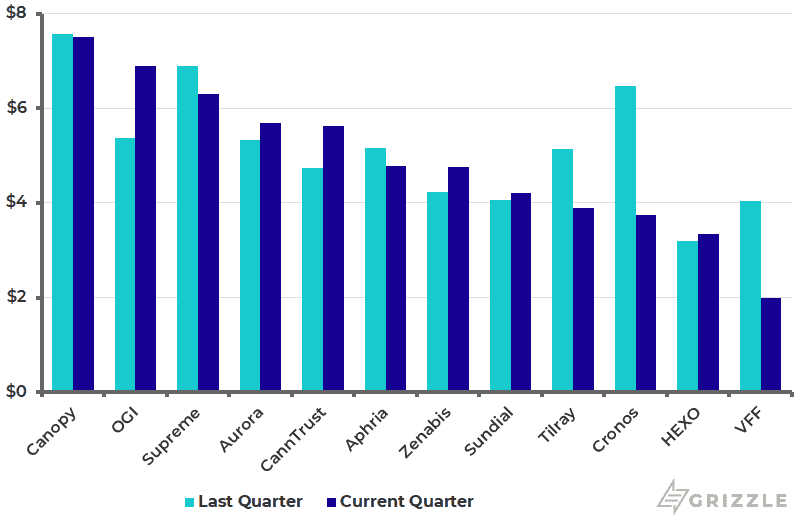

Revenue Per Gram of Cannabis Produced

Most importantly, Aphria is the second-most profitable LP, behind Village Farms, while pricing its products at a discount.

This is the power of efficient operations and low growing costs.

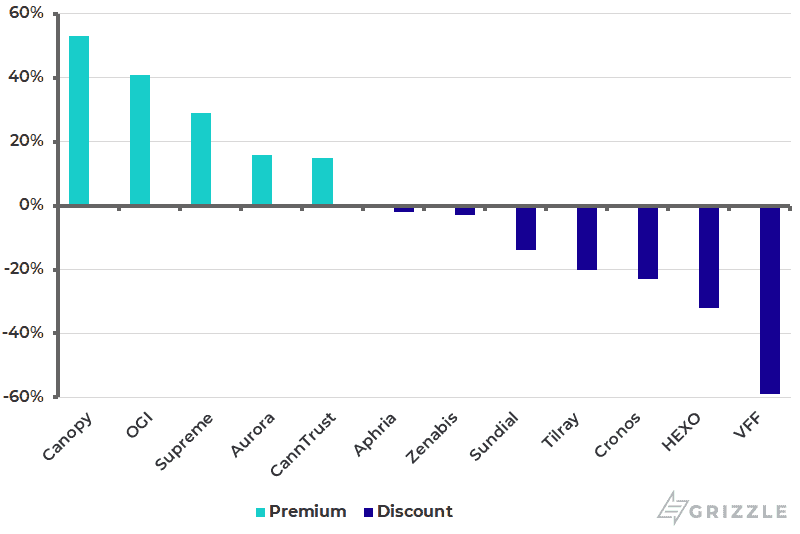

Aphria’s Cannabis is Priced Well vs Peers (2% discount)

Aphria’s overhead costs decreased again this quarter which is a good sign of scaling.

Production per gram fell 20% and at $2.10/gram puts Aphria in second place for lowest cost producer.

With Aphria Diamond just starting to ramp up, production costs could increase for a quarter or two before continuing to fall, maintaining the company’s cost advantage.

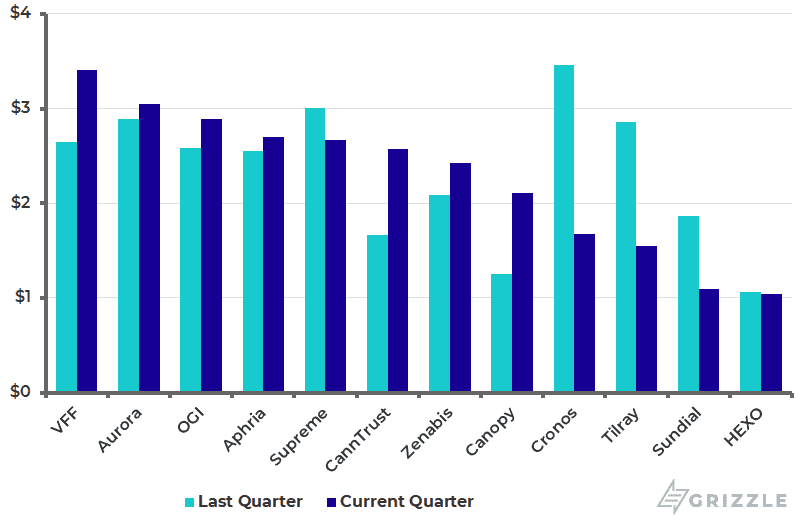

Production Costs Per Gram of Cannabis Produced

Aphria’s overall gross margin fell 6%, but margins in the cannabis business increased 6% and are 20% higher than the group average.

Aphria now generates $2.70/gram of gross margin putting it just behind Aurora and Organigram in fourth place.

Village Farms is the most profitable LP because the company is spending almost nothing on expansion, meaning production costs are much lower than peers.

The ramp-up of Aphria Diamond may lead to lower gross margins through the rest of the fiscal year, but we expect Aphria will return to class-leading margins with the rollout of cannabis 2.0 in early 2020.

Gross Margin Per Gram of Cannabis Produced

In the end, Aphria generated EBITDA loss of -$5.2 million, which is second-best behind Village Farms.

Importantly management reaffirmed positive EBITDA guidance for 2020, maintaining their expected lead in industry profitability.

EBITDA Per Gram of Cannabis Produced

Aphria Still Looks Cheap

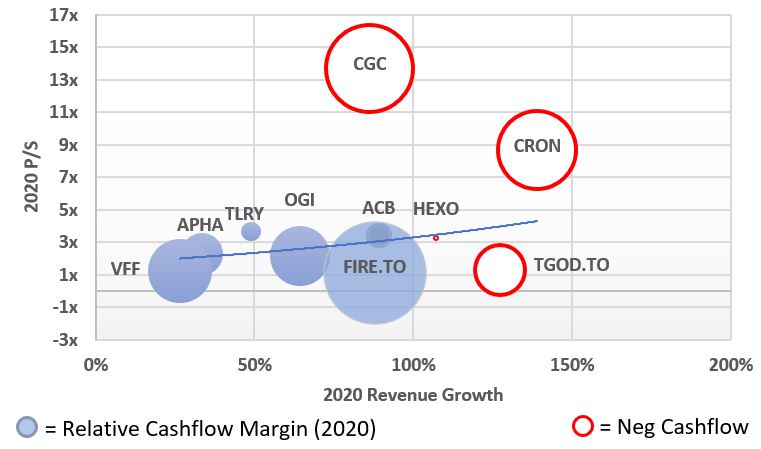

Aphria continues to generate the second-highest EBITDA margin, a proxy for cashflow, in the group yet is not being rewarded for that level of profitability.

Canopy Growth and Cronos, the two least profitable companies, trade at double and triple the multiples of the broader Canadian group.

Looking at the company’s valuation against its growth, Aphria looks fairly valued but this graph ignores the profit potential of each stock.

[su_panel background=”#ebebec” color=”#05011c” border=”px none ” shadow=”px px px ” radius=”4″ text_align=”center” class=”dw-editor-note”]Consensus expects 15% EBITDA margins in Aphria’s Fiscal 2021 vs the 6% management is guiding to this year. We think Aphria has a good shot at beating these numbers leaving upside in the stock. Aphria’s stock price will continue to outperform in 2020 in our view while peers continue to miss estimates and their stock prices lag.[/su_panel]Valuation vs Peers Remains Cheap

The company has half a billion dollars of cash and a two-year cash runway to weather any storm, plus the capacity to meet industry demand growth whatever it may be.

Canadian cannabis is looking at some tough pricing and demand trends in 2020, but Aphria remains a beacon of hope in the darkness.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.