Bottom Line

Aphria’s Q1 earnings are a warm-up before the main event — launch of legal recreational in Canada (October 17). As such the outlook is as important as the earnings and operational results themselves.

Aphria’s output in 2019 will be greater than it’s two largest competitors. This will be one of the key drivers of the share price as the market transitions to rewarding cost and execution over marketing and promotion.

There were some transitory operational headwinds in the quarter that we believe they were not material — Aphria remains the lowest cost producer.

A very important point that is rarely discussed in cannabis investing is the quality of earnings disclosure within this sector and in this respect Aphria is genuinely in a league of its own.

Why is earnings quality so important? If you are a consumer goods company’s buyout team, your comfort that the perceived value of the assets you intend to buy is really there, may make the difference between a direct equity investment or a less desirable JV partnership, or nothing at all.

One of the reasons more deals have not been announced could be the lack of quality companies to buy in the cannabis space. We feel Aphria is positioning themselves as the leader in transparency and thereby setting themselves up for the most attractive deal.

Importantly in the quarter, Aphria released 3 new retail brands (Good Supply, Goodfields, and RIFF) and now has a total of six, including their premium producer Broken Coast.

The battle for consumers will be won through branding, product choice, and consistency and Aphria is executing on all three.

We find it very intriguing that Aphria trades at a market capitalization 60% less than its peers but will match them in growing capacity in 2019.

For this fact alone, we think Aphria represents a compelling relative value opportunity for cannabis investors and a valuable portfolio of assets for a potential acquirer.

Operational Overview

Like all of the other large producers, Aphria worked through some operational issues in the quarter that come from ramping up the workforce and growing capacity at such a rapid pace.

However, even with $1 million of one-time costs from destroying a week’s worth of plants and lower capacity in the quarter, Aphria still has production costs 20% below the next producer and 40% below the group.

A lack of qualified growing staff made it necessary to throw out a week’s worth of plants. The decision to dispose of non-optimal plants instead of sending them to market anyway shows us Aphria is serious about their promise of product quality.

Aphria has since doubled headcount so growing issues should be a thing of the past.

Aphria also announced a two-month delay to the processing infrastructure at Aphria Diamond and to the construction timeline of the Processing Center of Excellence.

These delays are disappointing but are inconsequential to the longer term valuation.

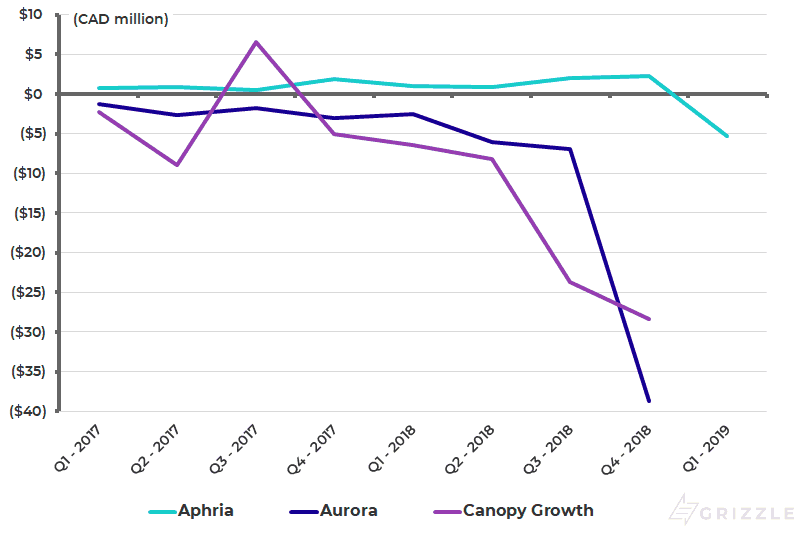

Due to ramped up spending on headcount, marketing and research, EBITDA turned negative in Canada, but we expect positive EBITDA in Canada will return in the first quarter of calendar 2019 as legal sales ramp up.

EBITDA by Quarter

Production and Inventory

Aphria sold 1,778 kg in the quarter, up 35% over last quarter.

Full capacity is running at 20,000 kg annually due to the decreased planting space in the quarter, but will be over 110,000 kg by January of 2019.

Inventory continues to ramp up for legal sales and is now at 4,900 kg, from 3,200 kg last quarter.

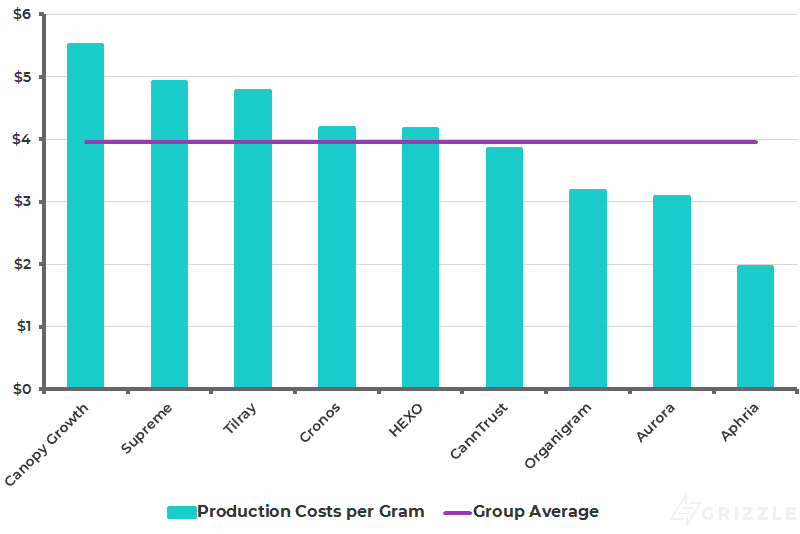

Production Costs Increase, but Still Best in Class

Like all of the other producers, Aphria had to decrease flowering room square footage to make sure space could be made for mother and vegetative plants.

The mother and vegetative plants will make sure the next two phases of the Aphria 1 expansion (phase IV and V) can begin growing as soon as the infrastructure is fully completed in January 2019.

Production costs increased as well due to the destruction of 14,000 plants because of transitory staffing issues.

Even with these two major costs, Aphria is still the lowest cost producer by a large margin.

Being the lowest cost producer means that Aphria should be the most profitable licensed producer as the legal market evolves.

Production Costs by Company

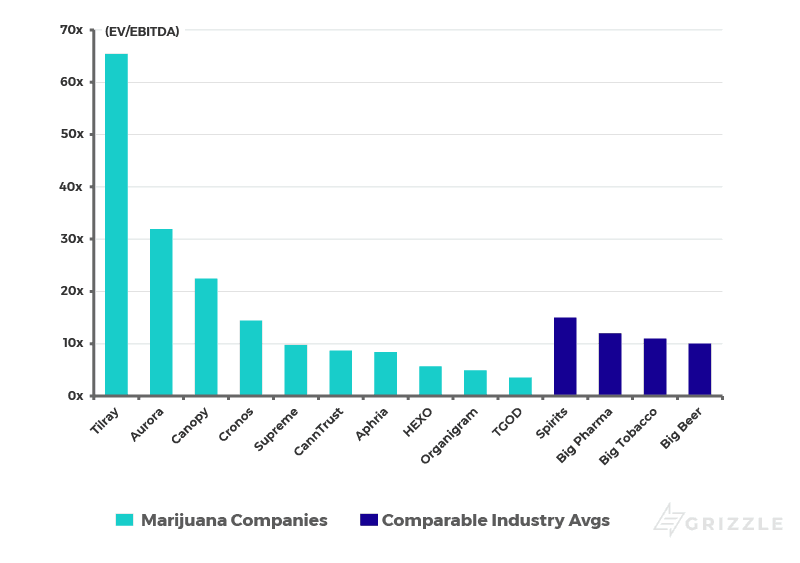

Aphria Continues to Trade at a Huge Discount to Peers Aurora and Canopy Growth

Even though Aphria will match or exceed the output of the two largest peers in the industry in 2019, the company trades at over a 60% discount to Aurora Cannabis and Canopy Growth.

The market will eventually evolve to a point where revenue is not coming solely from growing and selling cannabis flower and oils, but for the next 1-2 years, capacity and cost structure determine profitability.

Aphria is likely to out-earn peers through 2019 and we expect the stock multiple will move much closer to peers over the coming 12 months as earnings results set the gold standard for the industry.

Aphria is one of the few cannabis stocks that offer a margin of safety for investors.

2020 EV/EBITDA Multiple for the Cannabis Group

In the interest of full disclosure, employees of Grizzle personally purchased and currently own stock in Aphria, Inc. See the Content Disclosure section here on our Terms and Conditions page for more details.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.