Bottom Line

The special committee findings confirm that the Quintessential Capital Management short report was nothing more than an accusation Aphria overpaid for its Latin American (LATAM) assets disguised as an investigative report on a global web of fraud.

As Grizzle argued, and third parties have confirmed, Aphria (NYSE: APHA, TSE: APH) paid the going market rate for the assets it acquired.

We welcome the committee’s recommendation to strengthen Aphria’s governance practices, specifically as it relates to conflicts of interest. The decision by Board Chair Irwin D. Simon to refresh management is in our view a necessary step to regain investor confidence in the company.

The market has been demanding full closure on this matter for months from the company, the special committee’s findings give investors clarity and more importantly it allows management to focus their energy on executing and growing the business.

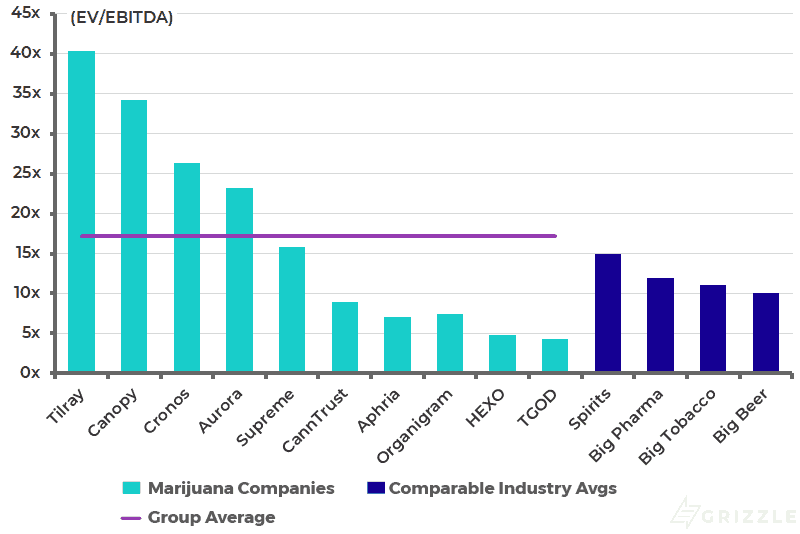

The valuation gap versus peers is significant. Aphria trades on 7x EV/EBTDA vs. peers at 17x EV/EBITDA.

There’s no question a significant part of the undervaluation is directly related to the controversy and allegations around the short report. We believe the closure of this matter should begin the process of bridging this sizeable valuation gap.

EV/EBITDA in 2020

While Vic Neufeld, Cole Cacciavillani, and John Cervini may have let down shareholders on the governance front, it is abundantly clear they were talented asset builders who will be handing off a company with industry-leading margins that is well positioned to flourish against peers in a fast-growing recreational cannabis market.

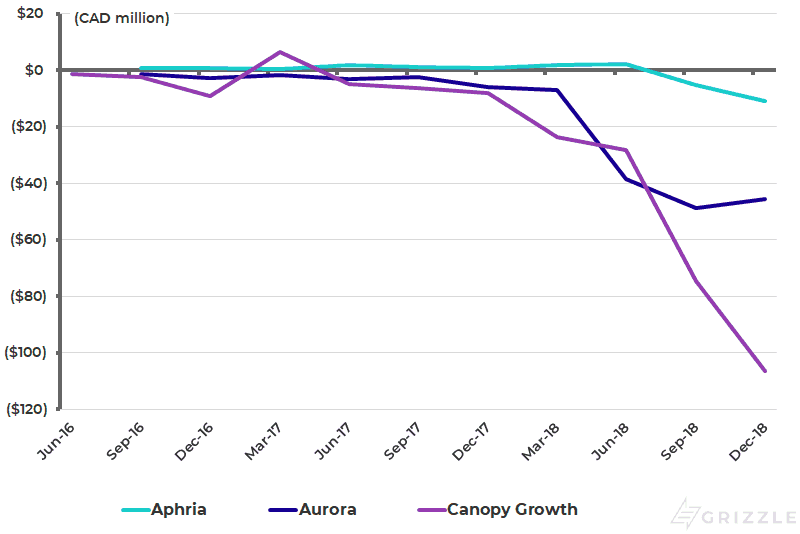

Quarterly EBITDA by Company

LATAM Transaction Price was Always in Line with Peers

Grizzle came out only hours after the Quintessential short report as the only voice willing to push back on the report’s conclusion that the value paid for the LATAM assets was massively inflated.

A cursory glance through the M&A metrics of competitors Aurora and Canopy showed us the value paid for these assets was fully in line with prices paid industrywide.

Stepping back a bit and looking at the deal-making history of Aphria’s two main competitors, Aphria is far from the most aggressive acquirer in the space.

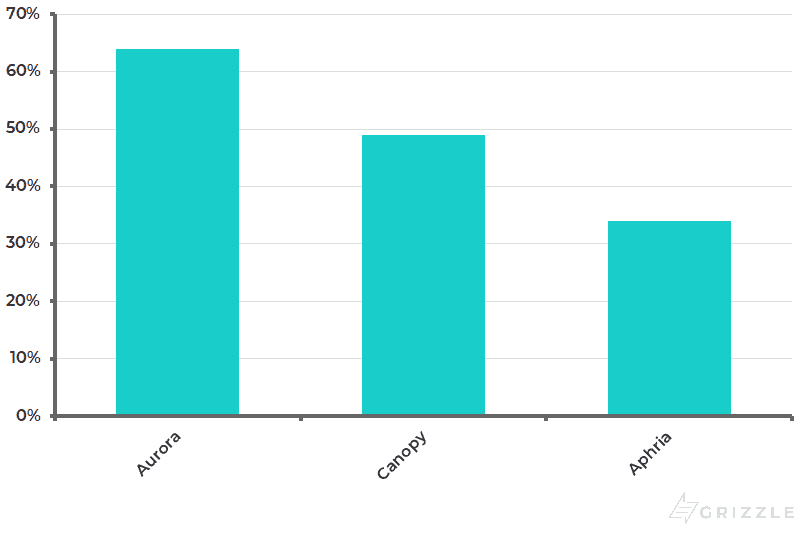

50% of Canopy assets are in goodwill, while Aurora was even worse at 64%, compared to Aphria with only 34% of assets in goodwill.

These numbers are all an investor needs to see to judge which LP is making acquisitions with a value mindset.

Goodwill as a % of Non-Cash Assets

Aphria paid the going market rate for assets it needed to establish a leading global footprint and two different independent third-parties validated the rationale for these business decisions.

The market has likely gotten the closure it needs to refocus back on Aphria’s peer-leading history of low-cost production and profitable growth.

The valuation gap won’t stay this large forever.

In the interest of full disclosure, employees of Grizzle personally purchased and currently own stock in Aphria. See the Content Disclosure section on our Terms and Conditions page for more details.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.