Apple Inc. (NASDAQ: AAPL) announced earnings results for Q1 2020 today.

Revenue came in at $91.8 billion, which beat analysts’ estimates of $88.41 billion (+3.83% vs estimates).

EPS came in at $4.99, which beat analysts’ estimates of $4.54 (+9.9% vs estimates).

Apple is providing the following guidance for its fiscal 2020 second quarter:

- Revenue between $63.0 billion and $67.0 billion.

- Gross margin between 38-39%.

- Operating expenses between $9.6 billion and $9.7 billion.

- Other income/(expense) of $250 million.

- Tax rate of approximately 16.5%.

Overall, the stock has rocketed to all-time highs and has more than doubled since this time last year. Back in August 2018, Apple made history by becoming the world’s first private sector publicly traded company to reach a $1 trillion market cap.

A Rich Valuation for a Rich Company

Currently, the company sits at a whopping $1.38 trillion market cap and is often regarded as the most valuable brand in the world.

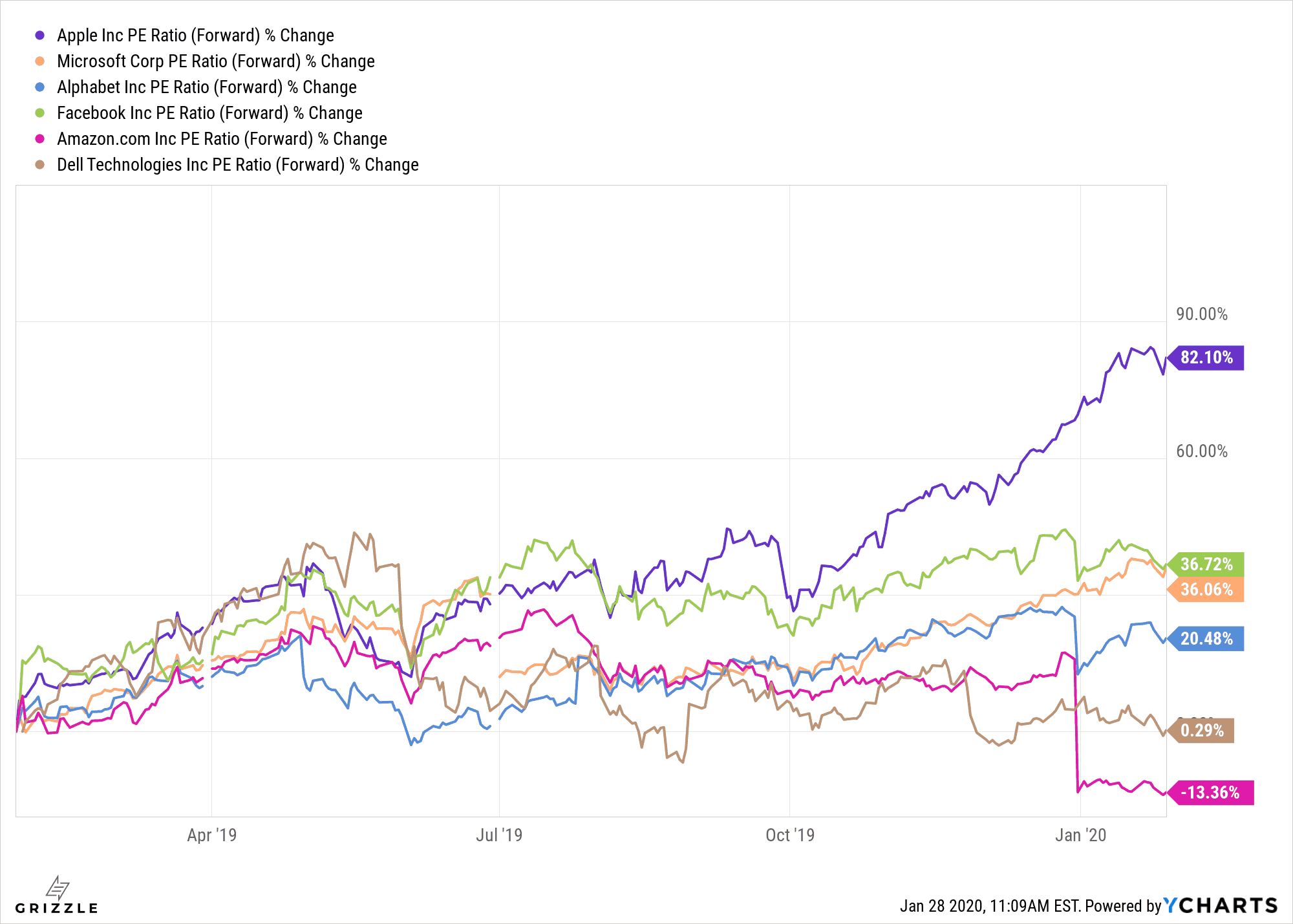

Taking a look at the change in forward P/E of Apple compared to other big names in tech, we see that Apple’s P/E has by far gone up the most throughout the past year, and the stock is trading at a valuation much higher than its typical levels. Part of this growth comes from excitement over Apple’s planned adoption of 5G connectivity in upcoming iPhones.

Competitors like Samsung already offer 5G options on some of their latest Galaxy devices and Apple is expected to follow suit after settling a lawsuit with Qualcomm back in April 2019. Qualcomm is widely expected to be the supplier of the 5G modem chips Apple would need on the upcoming iPhones. Apple’s dominance in the wearable tech industry with the Apple Watch has also certainly helped the stock price grow to new heights. According to 9to5Mac, in August 2019, Apple has the single largest market share of wearable smart devices at 37.9% beating out Fitbit (24.1%) and Samsung (10.6%).

Apple Wants You to Think That They’re a Software Company Now

Although Apple’s forward P/E has gone up significantly, it is currently still (only) just above 20. Comparing it to other tech companies, Google trades at around a forward P/E of 26.7 and Microsoft trades at a forward P/E of around 27. Apple’s historically low P/E in comparison to its peers is due to the fact that Apple is mostly regarded as a hardware company.

This is not without good reason, in the past quarter, about 52% of Apple’s revenue came from iPhone sales. In contrast to other big tech companies like Google or Microsoft who make most of their income through software, the technology hardware space is inherently less profitable due to the extra costs of manufacturing and shipping and just general logistics. Software sales are also often done on a subscription basis so it is easier for companies to guarantee a steady flow of cash instead of relying on the whims of the consumer on whether or not they want to upgrade to the latest iPhone this year.

This why Tim Cook, the CEO of Apple, has been pushing heavily for Apple to transition into a software company by offering services such as Apple Music, Apple Arcade, and Apple TV+, which is a streaming service meant to compete with the likes of Hulu, Netflix, and Disney+. Apple is also trying to get into the financial services space and has teamed up with Goldman Sachs to launch an Apple-branded credit card that integrates nicely with iPhones.

Apple has seemingly been very successful at convincing Wall Street of its transition into software and services and has been rewarded with an ever-increasing stock price. If Tim Cook’s vision of Apple’s software and services business comes true, then Apple’s P/E might increase even more to match that of other tech giants, and of course it will as well have a new stock price to match its new P/E.

However, for current shareholders of Apple or for people who are considering picking up some shares, one must ask themselves if they are convinced Apple’s vision of software and services dominance. If not, then as a hardware company it appears the stock is very overvalued at the moment.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.