After a disastrous May, shares of Apple Inc. (NASDAQ: AAPL) have swung for the fences over the last four weeks, as the prospect of easy monetary policy propelled stocks back towards record highs. The easing of trade-war tensions between the United States and China has also aided the recovery, putting Apple on track to re-take all-time highs.

Apple’s Recovery

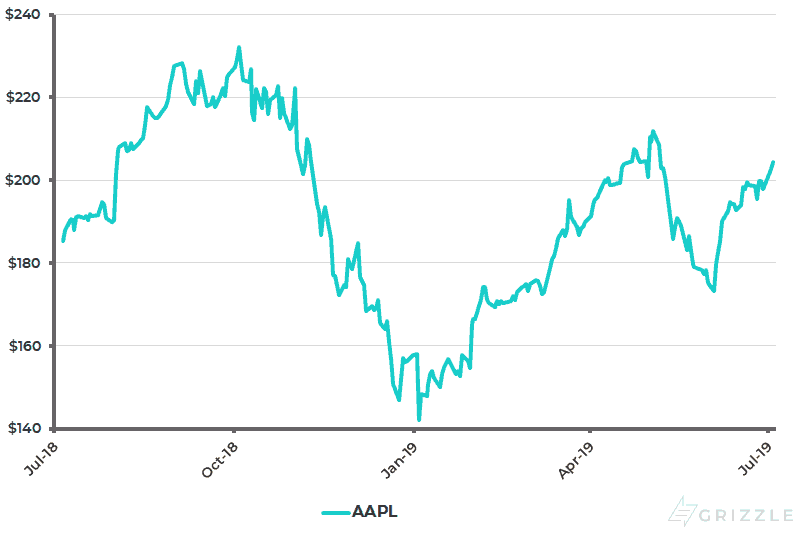

After peaking near $212 in early May, Apple’s stock price tumbled 18.1% through June, where it bottomed at $173.30. As of last week, the stock is back above $200 following an 18% recovery. APPL closed at $204.41 on Wednesday for a total market cap of $940.5 billion.

The stock is up 30% year-to-date and looks poised to re-take the May high. Doing so would put Apple on track to re-test peak levels for the first time since October.

Apple’s strong performance over the past four weeks is not unlike the rest of the stock market. The Dow Jones Industrial Average, S&P 500 and Nasdaq have all returned to record highs thanks to expectations for easy monetary policy and the resumption of trade negotiations between the United States and China. These factors have contributed to a sharp drop in stock-market volatility, as expressed by the CBOE VIX. The so-called “fear index” closed at 12.57 on Wednesday on a scale of 1-100 where 20-25 represents the long-running average.

That being said, Apple remains in a long-term uptrend that has been supported by strong innovation, booming iPhone sales, and revenue diversification (the latter is becoming more important now that smartphone shipments have peaked).

All Eyes on Earnings

Apple just announced that it will report third-quarter earnings on July 30. The Cupertino, California-based company surprised to the upside in fiscal Q2, easing some concerns about a protracted slump in revenues.

On April 30, the company reported second-quarter profit of $11.56 billion, or $2.46 per share, on revenue of $58.02 billion. Both figures represented declines from year-ago levels, but weren’t as bad as what the previous forward guidance had suggested.

Apple expects revenues to come in between $52.5 billion and $54.5 billion in Q3. Gross margin is projected at 37% to 38%.

The impact of slowing China sales remains one of the biggest question marks heading into earnings season. Citigroup recently downgraded its outlook on Chinese iPhone sales by half for both the June and September quarter. At the same time, the bank maintained a buy rating for APPL, which means that China-related volatility is only temporary.

Conclusion

In the short term, Apple’s revenue expectations should be seen as a barometer for the iPhone, which still accounts for more than half of company-wide revenue. In the long run, Apple must prove that it is more than a smartphone company. Shareholders shouldn’t be too worried given Apple’s “$300 billion-plus stock buying bazooka,” which should help offset the impact of declining sales.

At the same time, the company says iPhone sales trends are improving, which means the worst of the year-over-year declines could be over. So, while iPhone sales will likely be lower in Q3, the year-over-year declines will probably amount to single digits.

Disclaimer: Author holds no investment position in Apple at the time of writing.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.