The longer monetary tightening proceeds the more likely it is to trigger real problems in the area where credit growth has exploded in America since the global financial crisis in 2008.

That is in the private lending market, outside the post-2008 heavily regulated commercial banking system, and in particular in institutional leveraged loans to finance the likes of private equity deals.

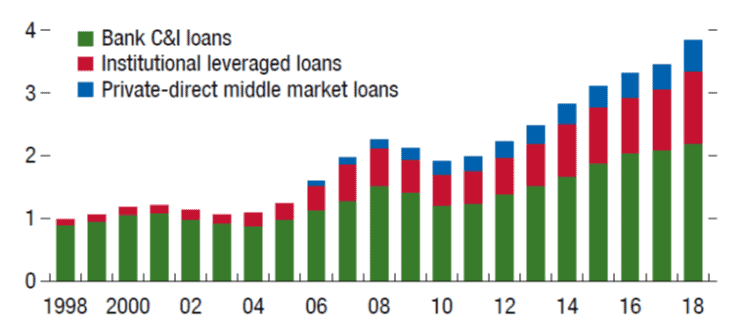

On this point, a chart from an IMF report in 2019 showed clearly that nonbank private lending in America has been growing at a faster rate than banks’ commercial and industrial loans (see following chart and IMF report: “Global Financial Stability Report: Lower for Longer”, October 2019).

Thus, leveraged loans and private market loans accounted for 43% of total corporate loans outstanding in 2018, up from about one-third in 2010.

US Outstanding Loans (US$tn)

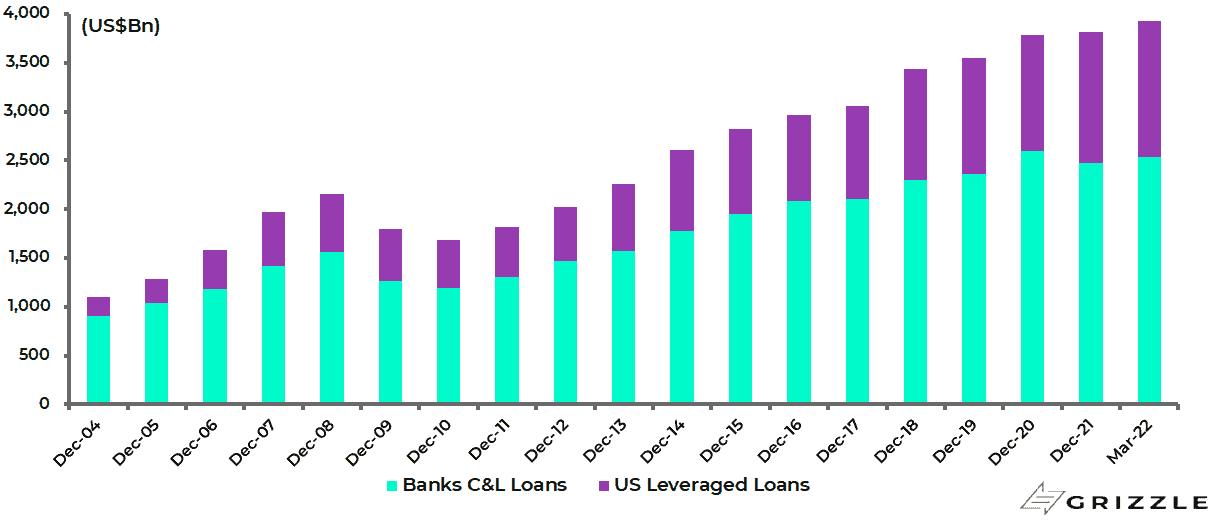

The situation has got more extreme since.

US total leveraged loans outstanding were US$1.39tn as at the end of 1Q22, according to data from the Federal Reserve’s latest Financial Stability Report published in May and leveraged loan information provider Leveraged Commentary & Data (LCD). This is up US$893bn or 180% from US$497bn at the end of 2010.

By contrast, US banks’ commercial and industrial loans have increased by US$1.34tn or 112% from US$1.19tn at the end of 2010 to US$2.53tn at the end of 1Q22.

US leveraged loans outstanding and banks’ commercial & industrial (C&I) loans

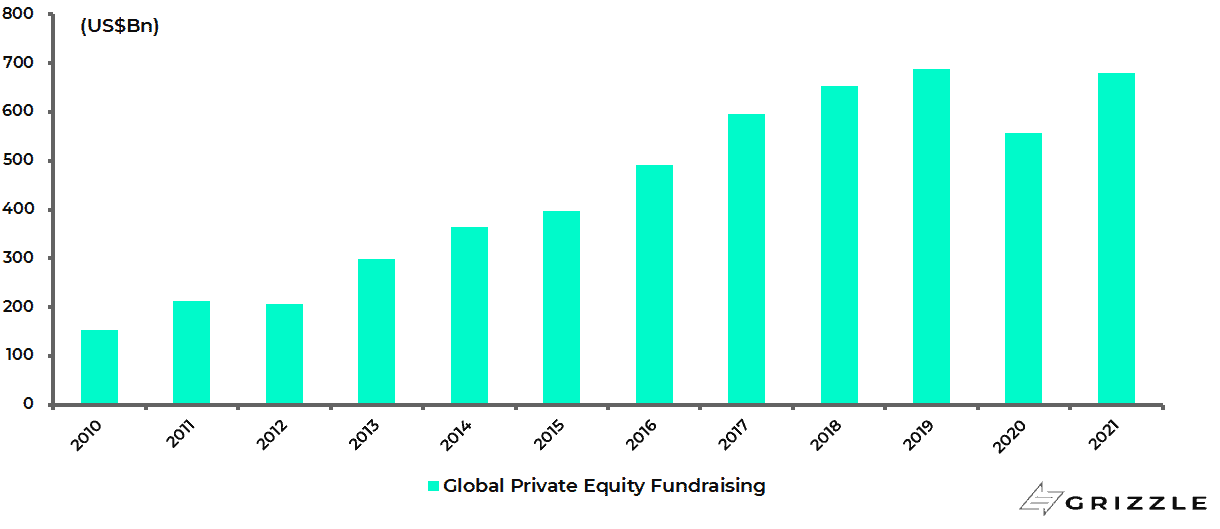

While a recent McKinsey research report published in March shows that global private equity fundraising rose by 22% YoY to US$680bn in 2021, with fundraising in North America up 25% to US$400bn (see McKinsey report: “Global Private Markets Review 2022 – Private markets rally to new heights”, March 2022).

Global private equity fundraising

Their investments are also not marked to market daily which prevents self-feeding panic selling of the type seen in recent months in crypto and the profitless tech thematic.

In this respect, ignorance seems to be bliss as highlighted in the attached article discussing the curious mentality which has driven huge asset allocation flows into the alternative investment space (see AQR Capital Management article by co-founder Cliff Asness: “The Illiquidity Discount?”, 19 December 2019).

A Mark to Market on Private Loans Could Start a Cascade

Still the longer the monetary tightening cycle proceeds, the more refinancings will expose the unrealistic “marks” valuing these investments and the related fees earned on them, and the more likely there will be an after-the-event regulatory post-mortem on why public pension funds and the like ever agreed to such restrictive terms in the first place, in terms of both the length of the lockups and the lack of transparent mark-to-market pricing.

But if this is a potential problem looming the key issue now, aside from the inflation data itself, is the stance of the Fed and the changing political pressures it is subject to.

In this respect, this writer has long criticised the Fed for its role in promoting the socialisation of credit risk and, in the post-2008 quanto easing era, promoting inequality as the perception grew, rightly or wrongly, that there was one rule for Wall Street and another for Main Street.

If this issue came to the fore in 2008 with resulting long-term political consequences, as only too evident in the extreme polarisation of American politics today, the origins of this problem, in reality, go back to the bailout of Long-Term Capital Management back in 1998, if not before.

The Fed is focused on Main Street, Not Wall Street

Still, if this is the past the issue now is that the Fed has started, rightly, to re-focus on Main Street.

And in this respect, it is the case that inflation is a regressive tax which hurts poorer households most.

It is also the case that consumers do not distinguish between consumer inflation and core inflation.

Similarly, the politically driven process of energy transition is inflationary and therefore is also a regressive tax in practice, while the conduct of war is just plain inflationary.

An acknowledgment of this aspect of inflation was made in a major speech last quarter by Fed governor Lael Brainard, who since 23 May has become the Fed vice chair (see Brainard’s speech at a virtual conference at the Minneapolis Fed: “Variation in the Inflation Experiences of Households”, 5 April 2022).

What is interesting about Brainard’s speech back in April is the emphasis she put on the socially regressive impact of inflation.

Thus, she stated that the burden is particularly great for households with more limited resources, noting that lower-income households spend 77% of their incomes on necessities compared with 31% for higher income households.

She also discussed how several studies have demonstrated that the consumer baskets of lower-income households have experienced higher-than-average inflation rates over time, while adding that it would be useful to have data about consumer inflation broken out by differing demographic groups, as is the case with US labour market and personal income data.

But for now such data does not exist.

If the likes of Brainard continue to stress such factors it may take them longer to turn dovish than this writer was previously assuming.

Still, that will only become clear if and when there is material evidence of the labour market weakening, which is not yet really the case.

But that point is surely coming.

Is 18% Fed Funds a Possibility?

Meanwhile, it is also interesting that Brainard quoted at the start of her speech a comment made by former Fed chairman Paul Volcker nearly 43 years ago who, when noting that the Fed’s dual mandate is not an either-or proposition, commented that runaway inflation “would be the greatest threat to the continuing growth of the economy … and ultimately, to employment”.

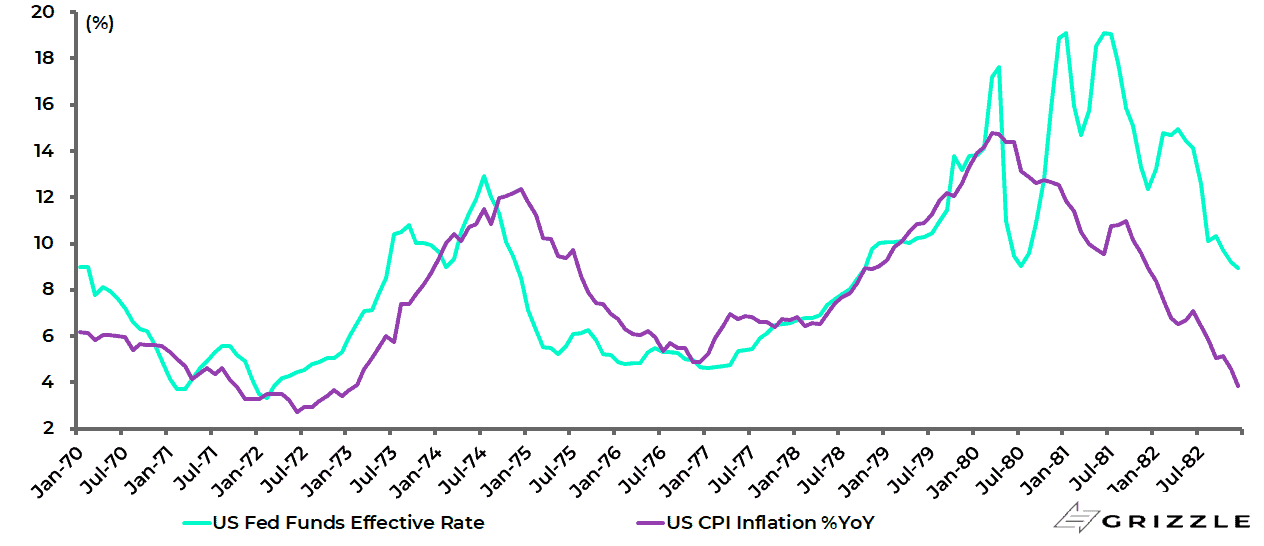

Speaking of the great man who died in December 2019, it is useful to compare the current situation, in terms of the potential for rate hikes going forward, and what happened back in the 1970s.

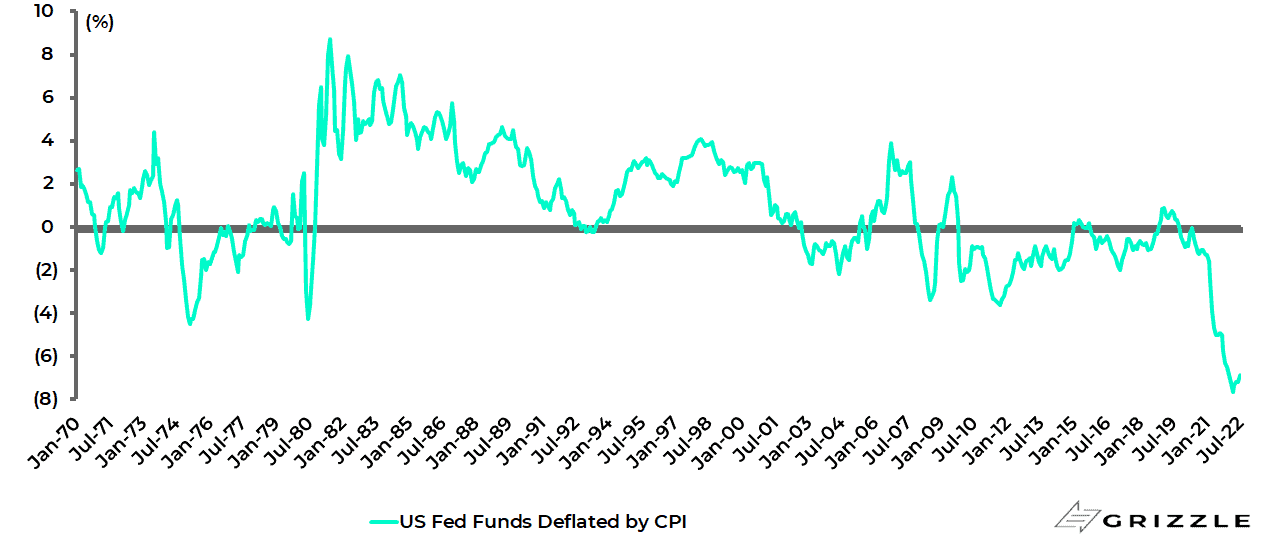

The first point to note is that, long before Volcker became Fed chairman in August 1979, the federal funds rate was raised from 5.5% at the start of 1973 to 11% at a time when CPI inflation was running at 7.4% in August 1973.

This was under the Fed chairmanship of the much-maligned Arthur Burns. So, by recent G7 central banking standards, Burns was an extreme hawk!

Still by the time Volcker took over in August 1979 CPI was running at 11.8%.

He then raised the federal funds rate by about ten percentage points in six months in both 1979 and 1980 and imposed real rates of 9% on the American economy.

US fed funds rate and CPI inflation (1970-82)

US real fed funds effective rate deflated by CPI

A repeat of the real federal funds rate seen under Burns’ tenure as chairman would lead to the nominal federal funds rate being 13% today relative to the current level of CPI, and a repeat of what happened under Volcker would mean a federal funds rate of 18%.

In such circumstances, there will be no more talk about asset price inflation but rather the opposite, and the talking point, as in any proper bear market, will be about who has lost least.

This writer is not predicting such an interest rate outcome at this juncture but only pointing out what the consequences will be if the Fed really chooses to fight inflation properly.

Meanwhile, the other temptation for central banks and governments, when faced with the market outcome of rising inflation in the form of higher government bond yields, will be to re-engage in financial repression by imposing yield curve control by fixing the price of longer-term bonds.

This is clearly not the current direction of travel in America and Europe.

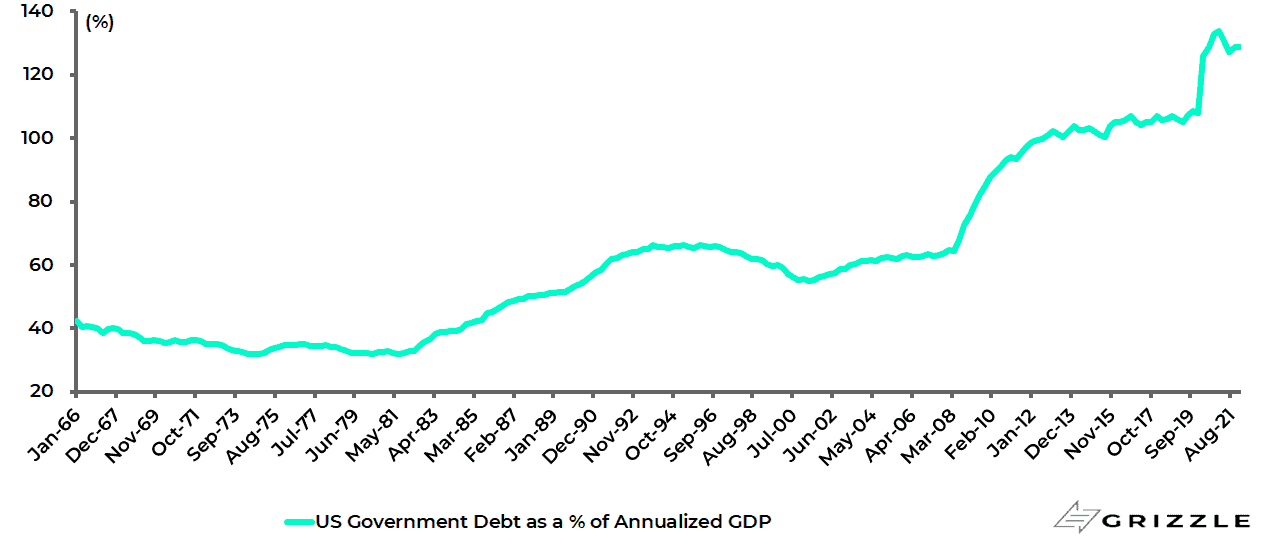

But that could change as the financial consequences of higher government bond yields became ever more evident in terms of the rise in governments’ debt servicing costs in the context of the massive increase in government debt since 2008, a process further accelerated by the policy response to the pandemic.

US total government debt, for example, has risen from US$9.5tn or 65% of GDP at the end of 2Q08 to US$30.4tn or 129% of annualised GDP at the end of 1Q22.

US government debt as % of annualised GDP

The views expressed in Chris Wood’s column on Grizzle reflect Chris Wood’s personal opinion only, and they have not been reviewed or endorsed by Jefferies. The information in the column has not been reviewed or verified by Jefferies. None of Jefferies, its affiliates or employees, directors or officers shall have any liability whatsoever in connection with the content published on this website.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.