The view here remains that the key issue facing investors in 2021 is the Federal Reserve’s policy response coming out of the pandemic.

Still another point to note is that the scale of the post-pandemic cyclical rebound should not be underestimated, most particularly for Asia and emerging markets, which should also benefit from a weakening US dollar.

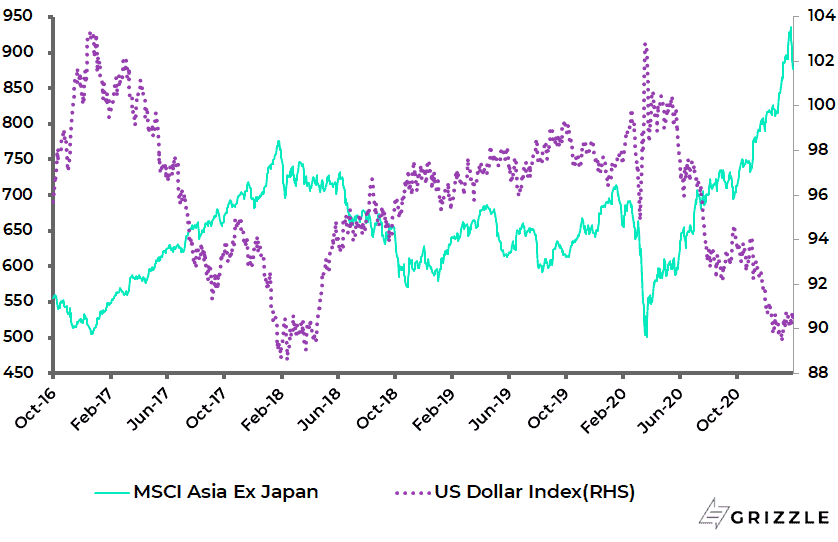

The correlation between the US Dollar Index and the MSCI AC Asia ex-Japan Index has been a negative 0.83 since October 2016.

MSCI AC Asia ex-Japan Index and US Dollar Index

In this respect, there is one major positive consequence of the Covid-19 pandemic that is often overlooked.

That is that it has created the likelihood of a global synchronised recovery for the simple reason that most economies bottomed out in the second quarter of last year when lockdowns were at their most intense, though, in the case of China, the recovery commenced one quarter earlier because the lockdown of the economy in China occurred in the first quarter of 2020.

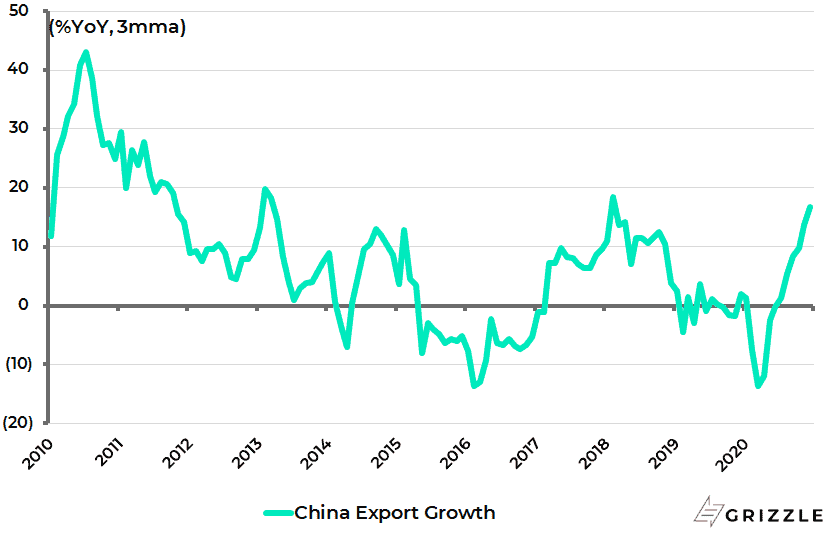

This is one reason why Chinese exports have recovered so dramatically in recent months since its factories were open to accommodate demand whereas other economies were still in varying degrees of lockdown.

China exports rose by 18.1% YoY in US dollar terms in December and were up 16.7% YoY in 4Q20.

China Export growth

Pent up Savings Could Drive a Post Covid-19 Recovery

While the medium- to long-term constraints on growth in the G7 world are real because of the monumental debt levels, investors as a practical matter, for now, should be focused on the potential for cyclical momentum to surprise on the upside.

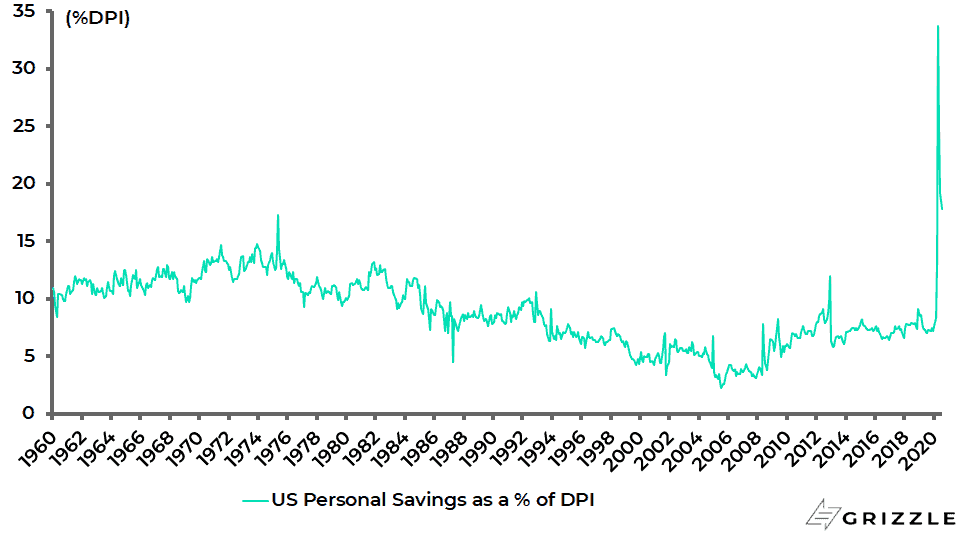

One highly relevant point here remains the increase in household savings rates in the developed world as a result of lockdowns, restraints on travel and increased transfer payments.

This can be seen both in America and the Eurozone.

The US personal savings rate has risen from 7.2% of disposable income in December 2019 to a peak of 33.7% in April and was still 13.7% in December.

US personal savings as % of disposable income

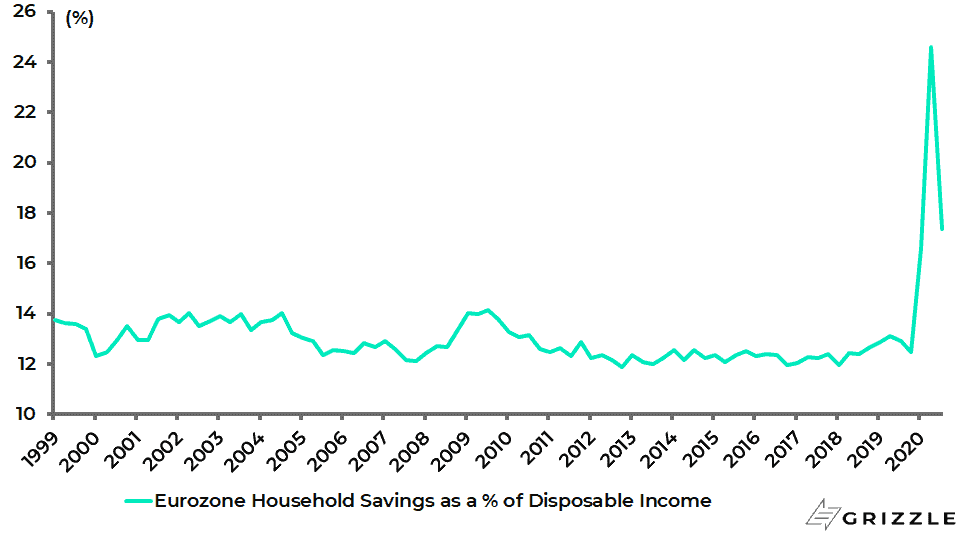

Meanwhile, the Eurozone household savings rate surged from 12.5% of disposable income in 4Q19 to a record 24.6% in 2Q20 and was still 17.4% in 3Q20.

Eurozone household savings as % of disposable income

Asia has Less Debt and Will Likely Outperform the West

Still, the real potential for a healthy extended cyclical recovery is in Asia.

The term healthy is used deliberately.

This is because in emerging Asia the Covid-triggered downturn has followed a more orthodox pattern.

Consider the example of credit growth.

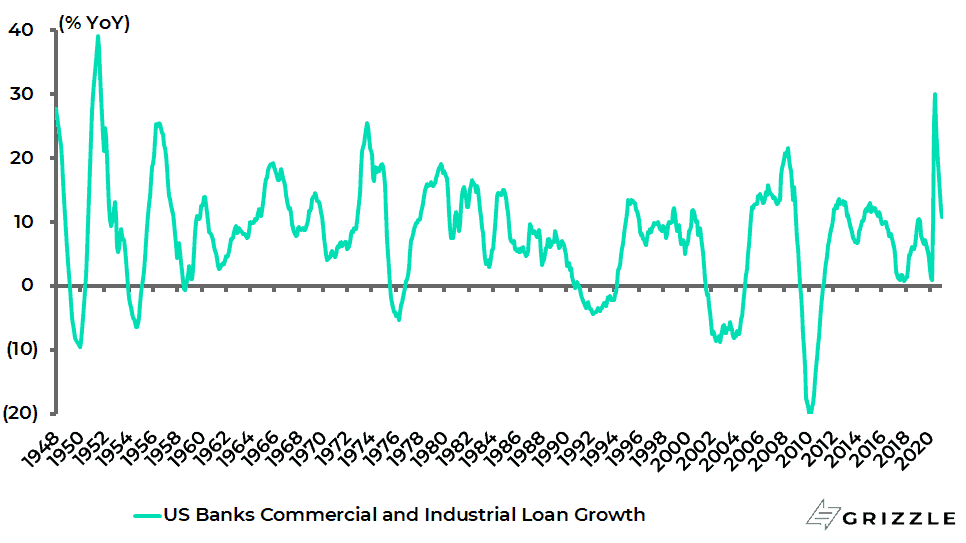

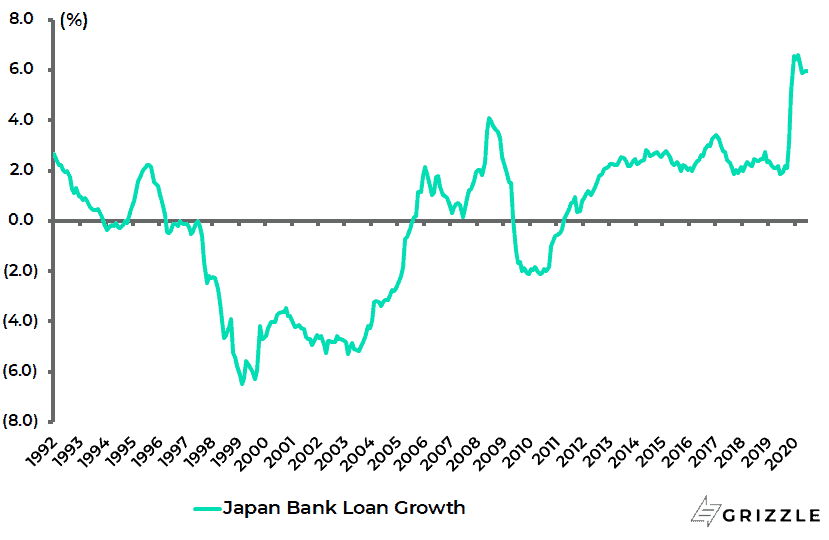

In the Western world and in Japan, bank loan growth rose to a surprising extent last year in the lockdown-triggered economic downturns.

US banks’ commercial and industrial loan growth surged from 0.5% YoY in mid-February to 31.3% YoY in early May, the fastest growth rate since August 1951, though it has since slowed to 9% YoY in mid-January.

US banks’ commercial and industrial loan growth

Eurozone banks’ nonfinancial corporate loan growth rose from 2.4% YoY in February 2020 to 6.7% YoY in May, the highest level since February 2009, and was 6.4% YoY in December.

Meanwhile, Japanese bank loan growth rose from 1.8% YoY in December 2019 to 6.6% YoY in August, the highest growth since the data series began in 1991, and was 5.9% YoY in December.

Japan bank loan growth

The main reason for this surprisingly buoyant loan growth in an economic downturn was government-guaranteed or quasi guaranteed lending schemes.

By contrast, bank lending slowed sharply last year in Asian countries like India, Indonesia and the Philippines; each of which suffered major outbreaks of the virus and related lockdowns.

Similarly, in terms of fiscal policy, the increase in transfer payments in Asia was minimal compared with the G7 world.

Transfer payments in China barely grew last year in stark contrast to what occurred in America.

Transfer payments accounted for 19.2% of China’s per capita disposable income in 2020, compared with 18.5% in 2019.

By contrast, US current transfer receipts accounted for 21.6% of total personal income in 2020, up from 16.8% in 2019.

China and US Transfer Payments as % of Income

The same lack of transfer payments was the case in India, where the government handed out food not money.

The Modi government announced in late March 2020 a food security scheme to provide free food to 800m people for eight months, giving each of them 5kg of rice or wheat per month until November 2020.

In both China and India the focus of fiscal policy was on maintaining capital spending targets in government budgets, not on expanding welfare programmes.

This is clearly a positive from the standpoint of boosting long-term productivity since China’s example has long since demonstrated the economic multiplier benefits of investing in infrastructure.

Still, there is likely to be another often ignored benefit to Asia, and indeed the whole emerging market world, from the coming cyclical recovery, assuming that it takes place in the context of a weakening US dollar and at a time when global inflation is likely to be rising.

That is that it is likely to lead to a much bigger increase in nominal GDP growth relative to real GDP growth, and it is positive swings in nominal growth that are really positive for equity investors since corporate earnings are nominal.

This dynamic at work can certainly be seen in the last major extended bull cycle for Asia and emerging markets when the US dollar was also in a weakening trend.

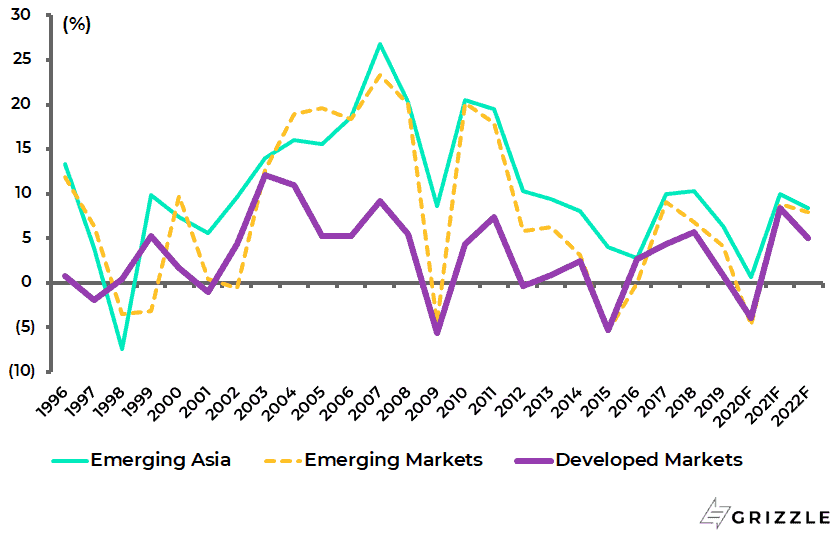

That was the period between 2002 and 2008 when nominal growth grew by an annualised 11% on a global basis in US dollar terms, while the US Dollar Index declined by 41% from its 2002 high to 2008 low.

Emerging and Developed Markets Nominal GDP Growth in US Dollar Terms

The important point to highlight is that the increase in nominal growth was much more dramatic for Asia during that period and translated into a dramatic outperformance for both Asia and emerging markets in a global equity context since Asia is by far the biggest component (80%) of the MSCI Emerging Markets Index.

Thus, emerging markets’ and emerging Asia’s nominal GDP rose by an annualised 19% and 18%, respectively, between 2002 and 2008, while developed market nominal GDP was up an annualised 8% over the same period.

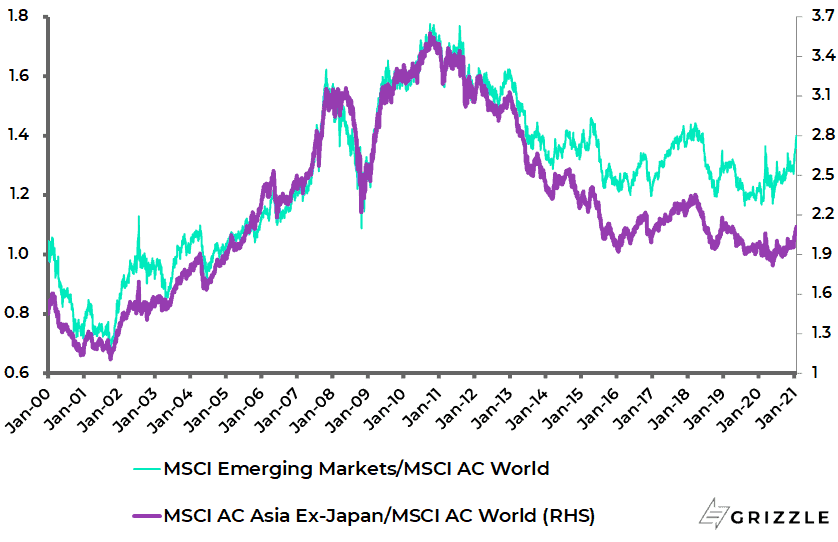

MSCI Emerging Markets and Asia ex-Japan relative to MSCI AC World

A Pickup in Inflation Depends on Global Success Fighting COVID-19

If the case for a weaker US dollar is reasonably clear cut in a world where the Fed remains doveish, and the Democrats control Washington, the case for a pickup in inflation in the US is much more controversial.

What is evident is that core inflation is likely to exceed the 2% target in the March-April period of 2021 if only because of the base effect.

The US core PCE price index declined by 0.1% MoM and 0.4% MoM in March and April 2020.

US core PCE inflation

The issue is what happens thereafter.

The surprise will be if inflation stays above that level and rises, which in this writer’s view is very likely in the context of a reopened global economy where monetary and fiscal policy remain so accommodative.

Clearly, the big risk to this pro-cyclical view is the efficacy of vaccines as they are rolled out, most particularly against the new seemingly more infectious Covid variants.

This is certainly a challenge.

But the good news is that there seems considerable confidence that in the case of the messenger RNA (mRNA) technology used by the likes of Moderna and Pfizer, the vaccine can be easily tweaked to adapt to the new variant.

But the issue will be whether regulatory approval can be as rapid.

The views expressed in Chris Wood’s column on Grizzle reflect Chris Wood’s personal opinion only, and they have not been reviewed or endorsed by Jefferies. The information in the column has not been reviewed or verified by Jefferies. None of Jefferies, its affiliates or employees, directors or officers shall have any liability whatsoever in connection with the content published on this website.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.