Project management software service provider Atlassian (NASDAQ: TEAM) reported results that crushed consensus estimates and will likely be taken positively by the market.

Revenue of $409 million was 5% higher than the company’s guidance and consensus of about $388 million.

Earnings of $0.37 beat consensus by a whopping 40% and were up 100% from the same time last year.

Revenue grew 37% year over year, compared to 36% growth last quarter and 39% growth at this same time last year.

These were solid top-line results and the market agrees, with the stock up more than 9% in after-hours trading.

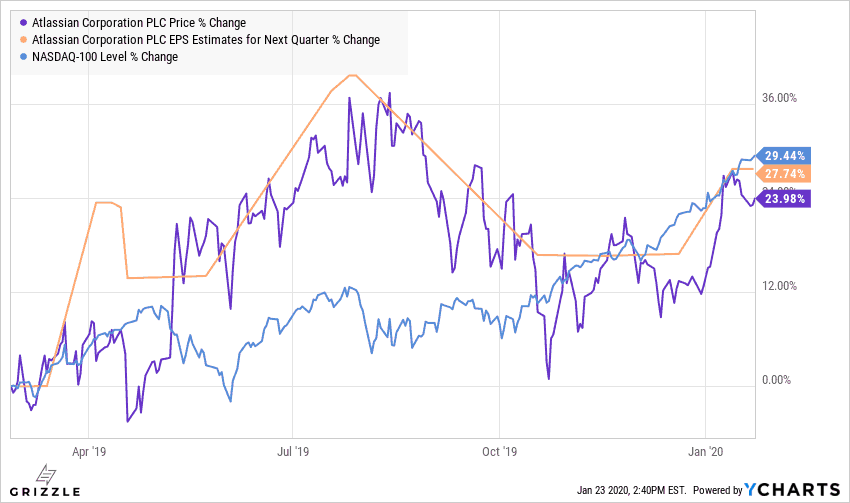

Will the Weak Performance Since September Continue?

The stock price of Atlassian, like all the new-age software providers, is driven primarily by growth expectations and secondarily profitability.

Atlassian has delivered on both but the stock has been underperforming peers since the September rebound in tech stocks.

Stock Performance Indexed to September

We think this is at least partly to do with slowing estimate revisions.

Earnings estimates for the third fiscal quarter are up 27% in the last year but have been falling since July, demonstrating sentiment was souring on the fundamentals of the business somewhat.

After these solid earnings results and a 5% increase to management guidance, we think the stock is primed to outperform peers for the next month or so.

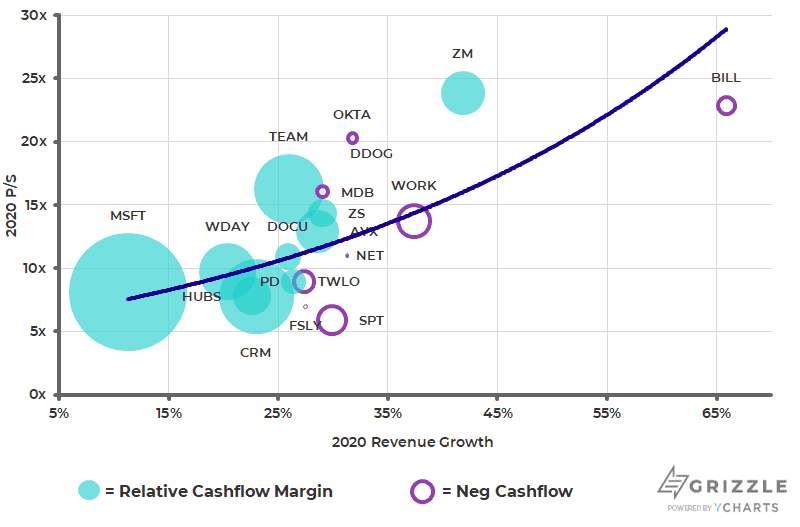

The company is far more profitable than many money-losing peers and the multiple reflects that.

Stocks priced at a premium are more volatile as a small miss to consensus can have a big effect on the stock price.

However, if the company can maintain revenue growth in the 20%-30% range the stock should continue to outperform the broader market.

Atlassian (TEAM) at a Premium Valuation but Justified by Profitability

Regardless of what happens to the stock tomorrow, Atlassian looks to be well-positioned to continue outperforming over the long term.

Internet software has the tailwind of an increasingly digital world, where demand for digital services is growing much faster than the broader economy.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.