Bottom Line

Aurora Cannabis (TSE: ACB) is now the largest licensed producer in Canada which bodes well for investors who care about price to sales multiples.

Even though there are some questions around the company’s cost structure and declining patient numbers, nothing in the earnings report changes our view that Aurora is ready for legalization and remains one of the two best positioned targets, along with Aphria, for a beverage giant who wants to enter the market.

Though Aurora is well positioned, there’s no room in the stock for any operational hiccups over the next six months.

We prefer to own cheaper stocks with a margin of safety such as Aphria, CannTrust or HEXO, until Aurora can successfully bring Aurora Sky into full production.

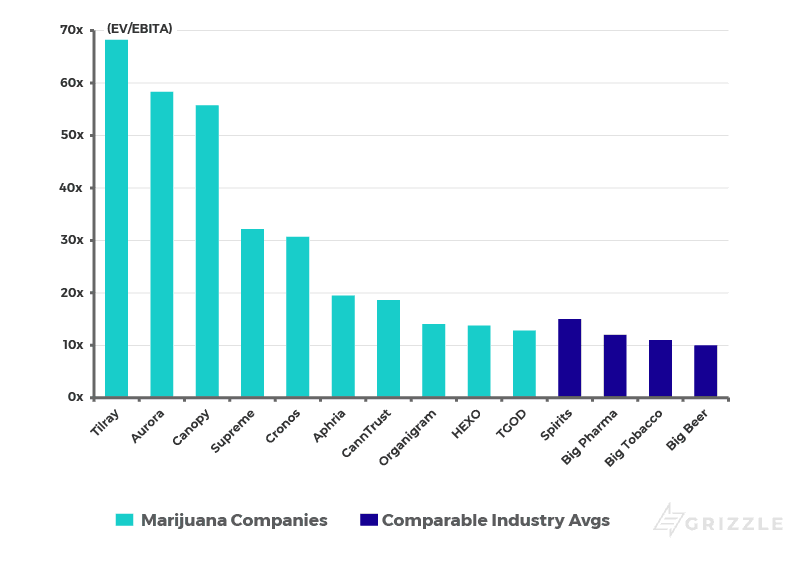

EV/EBITDA in 2020

A Review of the Quarter

Even though M&A is driving strong revenue growth, costs and spending continue to balloon making it hard to tell when the company will become profitable.

Annual overhead and interest costs are running at $250 million a year, requiring 75,000 kg of sales just to break even.

The company says as of September they have 45,000 kg of capacity but they only harvested 8,800 kg from April to June, making us think 45,000 kg is the best case production capacity for the first 3 months of legalization.

With Aurora Sky only 30% planted, and the remaining 70% not fully constructed or permitted, Aurora has a lot of work ahead of it to break even.

We think the break-even point won’t be until some time in the second half of 2019.

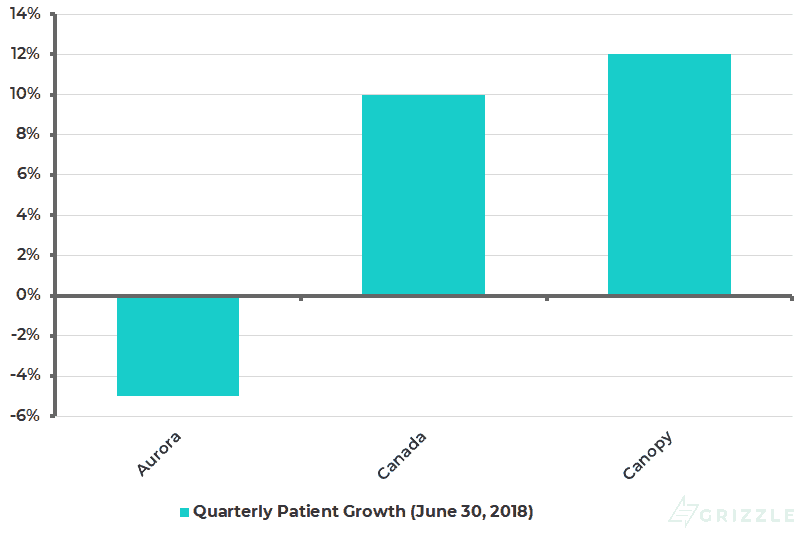

Where Did the Patients Go?

Aurora announced a surprising decrease in medical patients, down 5% to 43,308 from 45,775 last quarter.

Patient numbers in Canada as a whole continue to grow 10% a quarter and competitors all announced increasing patient numbers in the quarter, making this decrease that much more of an anomaly.

Without more colour on what drove the loss of patients, we worry that Aurora may be losing market share in Canada, which would be concerning this early in the market’s development.

Aurora Lagging Industry Patient Growth

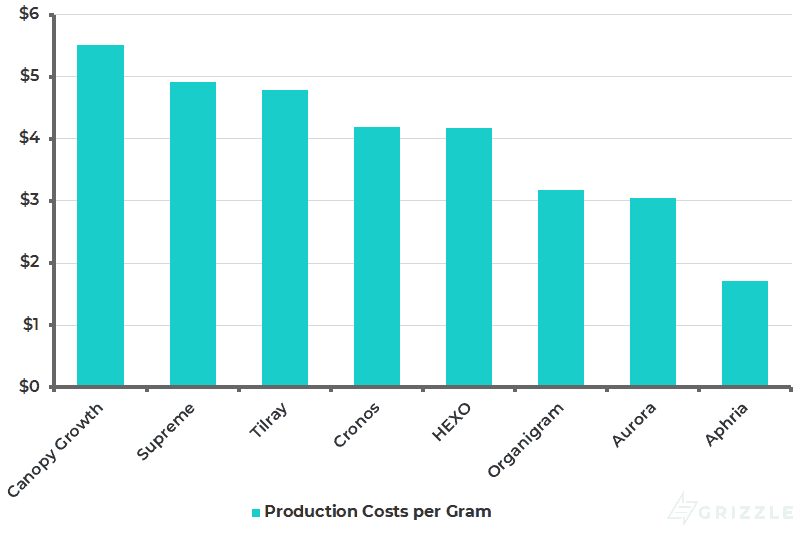

Production Costs Down, Growing Costs Up

Cost of sales were $3.90 per gram in the last 12 months, but Aurora brought its cost structure down significantly in this last quarter and now has a cost of production of $3.05 per gram, on the lower end of industry peers, a very positive development.

Production Costs per Gram

However, underlying cash growing costs increased 11% quarter over quarter to $1.70 per gram even though the weather was much warmer.

This tells us growing costs are only going higher as winter weather approaches and greenhouse heating costs spike.

Cash growing costs need to be under a dollar for industry players to turn a profit once lower legal prices arrive.

Aurora Sky Only 18% Planted

The market will likely be disappointed with the progress at Aurora Sky.

The company disclosed that only 18% of the facility is planted while another 12% of space is currently being planted.

The remaining 70% of the growing capacity still needs to finish construction and be licensed.

Management may have overpromised on Aurora Sky by telling the market:

The stock may be up today, but management should be careful about over-promising and under-delivering in the future.

Expect an Equity Raise Soon

Investors should also expect a new equity raise in the next few months as the company is burning $260 million a quarter with only $90 million in the bank.

Even with the new $250-million BMO debt facility, they will run out of money either by the end of December or the following quarter unless they do an equity raise, cut their investment spending or find a way to break even.

Last year the company raised $256 million through convertible debt and equity issuance and we expect the next 12 months to be more of the same, diluting shareholders further.

Overall Great Growth, but Questions Remain

By buying competitors, Aurora has managed to take the crown as the largest producer this quarter, demonstrating improved market share through acquisitions.

Declining patient numbers do throw some cold water on the revenue growth, however, and investors still have to worry about some operational hiccups at Aurora Sky which is running behind schedule.

The next two quarters will be crucial for Aurora to demonstrate to investors it is well positioned to take advantage of the $8 billion recreational cannabis opportunity.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.