Bottom Line

Though earnings did not include results from early recreational sales, Aurora gave us some clues about how they are positioned to capitalize on legalization.

Most importantly, management says that facilities now up and running can produce 70,000 kg of cannabis a year, enough for the company to break even at worst in 2019.

A quarterly run rate of 70,000 kg should be apparent by Aurora’s 3Q earnings (calendar ending June 2019).

Avoiding a big negative cost surprise, Aurora should be generating positive EBITDA (earnings before interest, taxes and depreciation) in 2019, which is a big deal.

Aurora looks surprisingly well positioned for recreational sales with a 20% market share of medical patients in Canada and 30% of initial sales in Ontario, the largest province by sales.

Anecdotally, Aurora products were easy to find in the first week of legalization and Aurora is one of the few brands that are being restocked on the Ontario Cannabis Store website.

Aurora looks to be leading when it comes to meeting supply agreements and distributing products, though we will have to see what the other large producers say on their earnings calls to be sure.

This quarter was just a taste so investors should withhold judgment until they see how the first 3 months of legalization went for Aurora.

We need to see the final cost structure and most importantly legal market pricing before we can be confident what cash flow and earnings will look like in 2019 and 2020.

Operations Review

Aurora did see increasing operational costs again this quarter as marketing expenses and increasing headcount all contributed to higher costs.

Management did say marketing costs should be down quite a bit due to cannabis ad restrictions going into effect on October 17th.

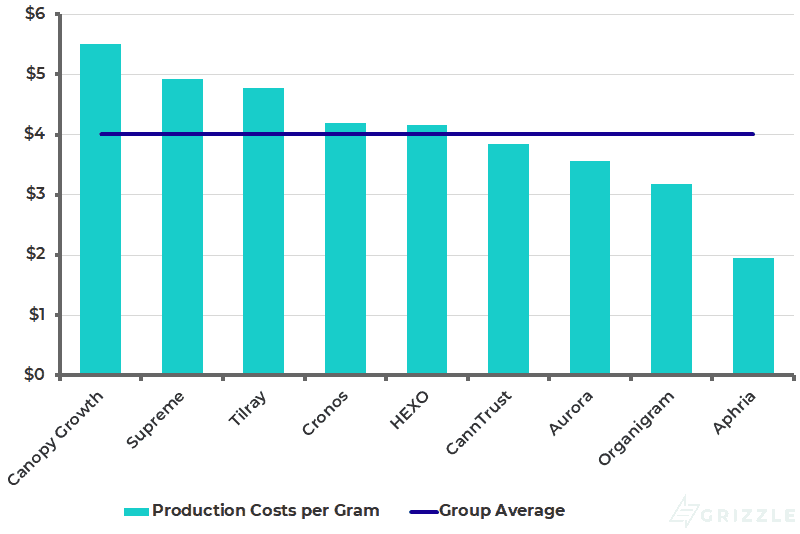

Overall production costs on a per unit basis were basically flat, down 1% to $3.57 per gram in the quarter, putting Aurora’s cost structure near the bottom of the peer group (bottom 30%).

Keep in mind we ignore growing cost information fed to us by management and stick with total production costs which are easily available from all producers, allowing a more realistic comparison between companies.

All-in Production Costs Per Gram

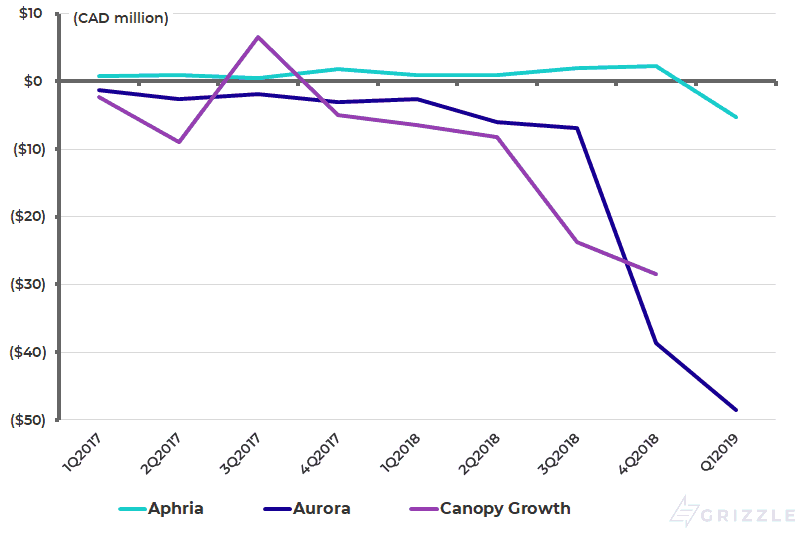

We have been keeping track of quarterly EBITDA for the big three producers and Aurora continued to see a growing EBITDA deficit.

This should be the worst the deficit will ever be before significant recreational sales kick in the following quarter.

Aurora should have breakeven EBITDA in their third-quarter earnings (June 2019), if they can produce the 70,000 kg of capacity they say they have.

Quarterly EBITDA for Top 3 Producers

Valuation

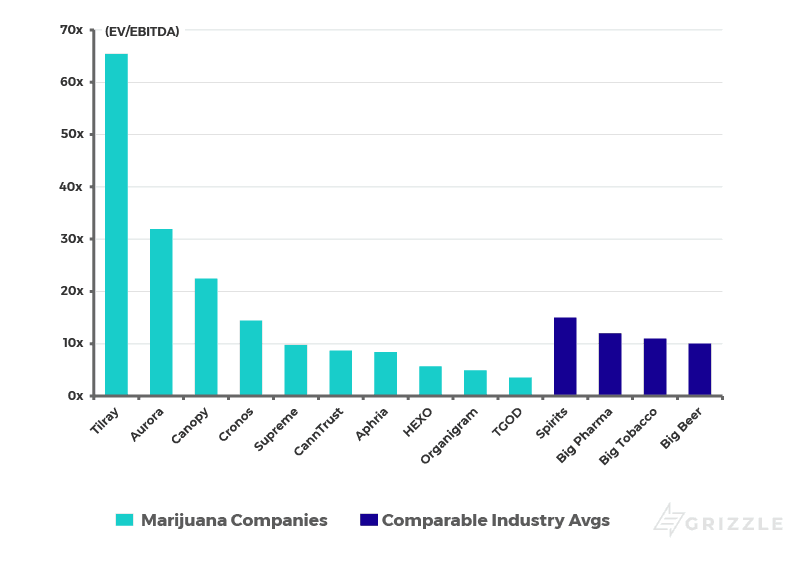

Aurora remains one of the more expensive cannabis stocks trading at 24x expected EBITDA in 2020.

Aurora may be one of the market share leaders so far, but we would be wary of paying for perfect execution before the company has been tested in the legal market.

With so many large cannabis operators trading for much cheaper, including U.S. names, we would recommend investors put their money into cheaper producers until Aurora can prove they are worth the premium price through class-leading profitability or flawless execution.

The next two quarters will be an exciting time for investors as they start to see who the real operators are and which companies are creating the brands and products consumers want to buy.

Enterprise Value to EBITDA in 2020

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.