Bottom Line

Aurora has arrived as a major player in the recreational market capturing ~20% market share of rec volumes in the quarter ending December.

However, the rapid ramp in revenue and most importantly profit that investors have been waiting patiently for is on track to take much longer than expected.

It’s now looking likely that investors will have to wait until 2020 for positive earnings and EBITDA.

To break even Aurora needs to triple production to 80,000 kg per year, but is only on pace to sell 28,000 kg in 2019 based on this quarters run rate. Maintaining their share of the recreational market would only equal 22,000kg of sales in 2019 at the market’s current growth rate.

[su_panel background=”#150093″ color=”#ffffff” border=”0px solid #cccccc”]Given that recreational demand in Canada was only up 3% in December over November, a 65% annual growth rate, Aurora is going to have to either drastically increase market share or hope consumers start flooding dispensaries if it hopes to turn a profit in 2019.[/su_panel]In 2017 management was talking about having 200,000 kg of sales capacity by the end of 2019, which could have generated $240 million of EBITDA, however, with the slow growth in sales volumes and market demand, we think Aurora will be lucky to sell 50,000 kg, generating $83 million of EBITDA at a 30% margin in 2019.

On the conference call, management promised falling production costs, better pricing and good growth in production through the rest of 2019.

At the current stock price, they are on the hook to deliver just that.

Operations Review

Aurora grew revenue 220% quarter over quarter on a reported basis, but when using Pro-forma revenue for last quarter that included soon to close acquisitions, growth was less impressive at 133%.

For reference, the three other producers to announce recreational sales (HEXO, Organigram and Aphria) grew revenue 400%, 530% and 160% respectively in the same quarter.

Aurora saw production costs per gram actually increase 3% over last quarter even though cannabis volumes sold almost tripled. Aurora is not yet showing any indication that scale is benefitting production costs.

All-in Production Costs Per Gram

Revenue per gram fell 25% from $9.90 to $7.40 per gram as lower pricing from the government-run distribution monopoly fed through the financials.

Gross margin fell hard in the quarter as revenue per gram fell but production costs did not. Gross margins were down 42% quarter over quarter to $3.70 per gram which still compares favorably to other producers who have been averaging $3.20 per gram.

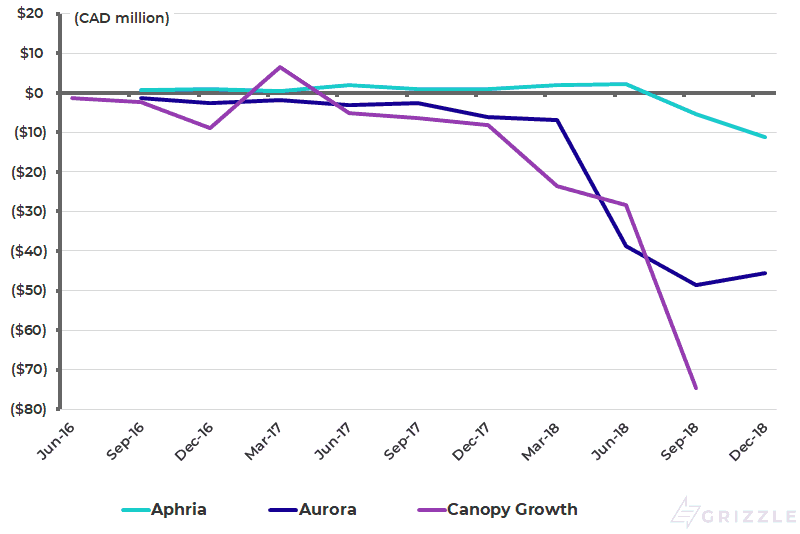

Aurora didn’t see any improvement in the EBITDA burn which is running around $184 million of cash out the door on an annualized basis against market expectations of $100 million of EBITDA generated in 2019.

It has us a bit concerned that revenue doubled but the EBITDA burn rate did not improve.

Quarterly EBITDA for Top 3 Producers

Valuation

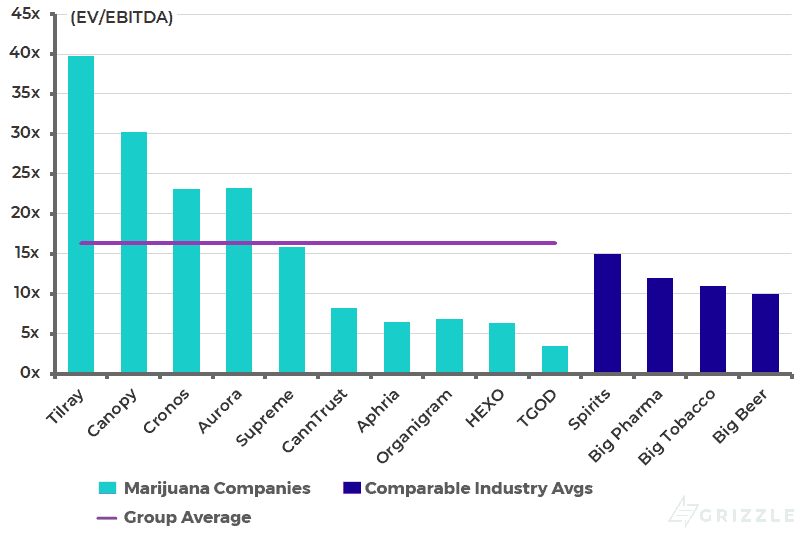

Aurora remains one of the more expensive cannabis stocks trading at 23x expected EBITDA in 2020.

Risks are growing that our 2020 EBITDA estimate, which gives the company credit for fully funded capacity is going to be too optimistic. If this is the case, Aurora is actually trading much higher than 23x EBITDA.

Aurora may be one of the market share leaders so far, but we would be wary of paying for perfect execution before the company has been tested for a few more quarters in the legal market.

With so many large cannabis operators trading for much cheaper, including U.S. names, we would recommend investors put their money into cheaper producers until the Canadian recreational market shows it is working off the growing pains of legalization.

Sentiment is far too rosy for the current slow growth the industry has been facing.

Regardless, the next few quarters will be an exciting time for investors as they start to see who the real operators are and which companies are creating the brands and products consumers want to buy.

Enterprise Value to EBITDA in 2020

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.