Bottom Line

This quarter’s earnings confirmed our suspicions that the legal cannabis market in Canada has flatlined.

Sales countrywide are not growing meaning licensed producers are just fighting among themselves for market share of a stagnant pie.

Investors need to think long and hard before owning Canadian grower stocks as stock prices now depend on a successful launch of the edibles market later this year.

For Aurora investors, there is some good news.

Aurora, surprisingly is taking market share away from others and finding a way to grow revenue even though the larger market has gone ex-growth.

We estimate Aurora now owns 37% of the Canadian cannabis market, up from 27% last quarter.

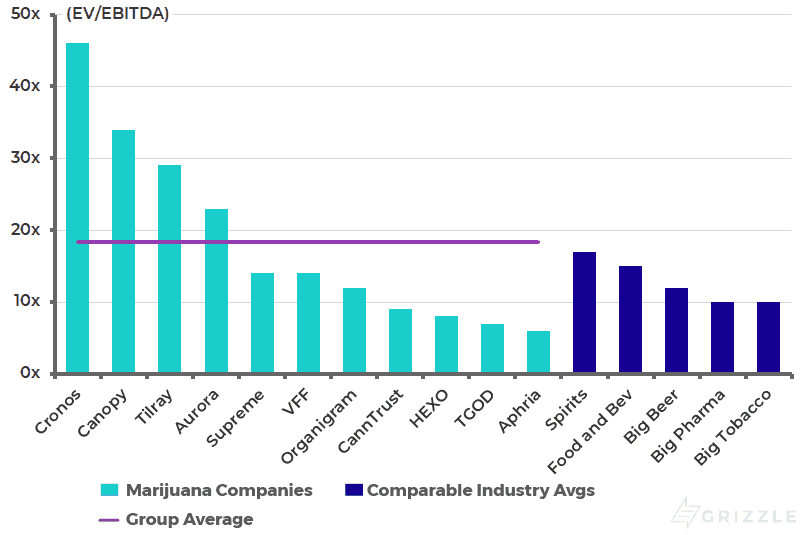

Aurora is trading at more than 100x EV/EBITDA with a 37% market share in Canada. This is a clear indication investors expect revenue to skyrocket from here.

Investors need to understand Aurora needs the rollout of edibles and vape pens to be a home run, otherwise stock prices across the sector are at risk.

Estimated 2020 EV/EBITDA

Operations Review

Aurora generated revenue of $65.15 million in Q3, with $58.6 million of that coming from cannabis sales. Sales of 9,160 kg were up 30% from last quarter, a solid outcome.

Revenue per gram declined 6% driven by lower flower prices, partly offset by higher prices for oils. The decline was 2% higher than the market average though results vary widely with Cronos seeing pricing up 8% while selling prices for Organigram fell 19%.

Revenue Per Gram

Production costs also up, but by a lesser extent, up 12% QoQ to $27.4 million. This gave Aurora lower product costs per gram, down $0.5 to $3.00 per gram compared to the previous quarter. This puts them in the middle of the pack among peers.

All-in Production Costs Per Gram

The net effect was a gross profit of $31.3 million, good for an impressive 35% increase over last quarter.

On a per gram basis, the gross margin increased by 3% driven by operating costs that fell more than revenue per gram. Management is clamping down on expenses in a bid to reach positive EBITDA, which they claim they will achieve by fiscal year-end.

On a per gram basis, Aurora now has the highest gross margin among peers at $3.4 per gram.

Gross Profit Per Gram

Using EBITDA as a proxy for cashflow, only one cannabis company, Organigram, is currently profitable. Aurora is moving in the right direction but still losing almost $40 million a quarter so has a lot of work to do.

EBITDA per Gram

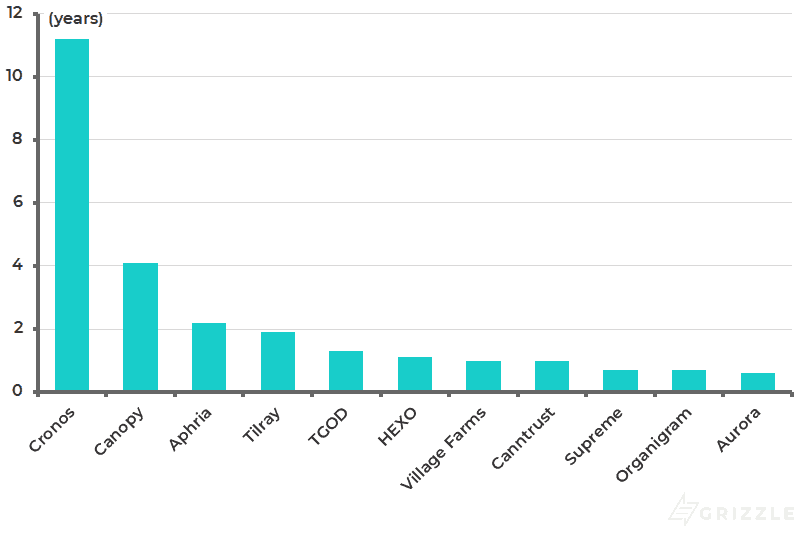

When looking at their liquidity levels, they currently hold $391 million in cash and equivalents. At their current quarterly burn rate, this leaves them with just over half a year of cash remaining.

Aurora is up against the wall to either turn a profit by year end or go back to the market for more money.

Years of Cash Remaining

Other Developments

On April 2nd, a short form base shelf prospectus was approved, allowing them to offer up to $750US million of common shares, warrants and debt securities for the next 25 months.

Yesterday, Aurora filed a prospectus supplement, worth $400US million for sale of common share on the NYSE.

So while dilution looks imminent, the company has solid plans to acquire the cash needed to fund operations until they are cash positive.

Finally, investors interested in the organic cannabis market were able to get their first look at Whistlers operations. At full scale, their operations will produce 5,000 kg annually. they are expected to bring all facilities online by the end of 2019.

At a purchase price of $158.1 million (common shares and contingent cash), Aurora is valuing Whistler’s cannabis production capabilities at over $31 per gram. A steep price no matter how you bake in IP and experience into Whistler’s valuation.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.