A write-down is like a restaurant dish that goes viral.

Everyone talks about it, but no one takes the time to figure out how the dish is made and why it looks and tastes so good.

Write-downs sound like some boring term an accountant thought up, which is actually true, but more than that, write-downs can have non-boring real-world consequences for companies and stock prices.

The official definition of a write-down:

A write-down is basically telling current investors they overpaid for their shares of the company.

Write-downs also signal you are backing a management team that is either bad at forecasting industry trends or bad at negotiating deals.

Neither is good news for the company’s ability to generate attractive returns on your money.

If Write-downs are “Non-Cash” Why Should I Care?

Even though no cash leaves a company’s bank account, in a best-case scenario write-downs tell you important information about the quality or lack thereof of the management team and at worst leads to bankruptcy and big losses for stockholders.

Where write-downs matter most is if a company has debt on the balance sheet.

Most debt contains covenants, which are basically rules the lenders think up to try and decrease the risk they don’t get their money back when its due.

Covenants say things like “You can’t sell assets unless you pay us back first” or “Our debt is secured by your office building and any new debt you issue needs to wait in line behind us to get paid”.

If a company trips one of these covenants, they are in what’s called “technical default”.

A study looking at 87 technical defaults found stock prices fell 20% leading up to the default and another 3.5% on the day the default was disclosed.

Some companies suffered losses as high as 48% on the day the default was disclosed to investors.

Technical defaults rarely cause a company to declare bankruptcy, but from a stockholder’s point of view it doesn’t really matter as you are taking big losses regardless.

Technical Defaults and Aurora Cannabis

Aurora Cannabis (NYSE: ACB; TSE: ACB) has been the poster child for all the excesses of the early days of cannabis legalization.

The company was willing to pay any price to gobble up assets and show the market blistering growth.

Heavy cashflow losses were generated in the process and as a result Aurora turned to The Bank of Montreal (TSE: BMO) in late 2018 to continue funding these losses.

BMO agreed to provide up to C$360 million of secured debt maturing on Aug. 29, 2021.

Aurora has already borrowed C$196 million and we believe only has another C$20 available that isn’t revolving (i.e. short-term debt).

Facility D can only be drawn to pay for construction of Aurora Sun and with Aurora Sun construction halted, the ~C$100 million facility D is off-limits.

Aurora’s BMO Credit Facility ($ millions)

| Facility | Outstanding | Total | Notes |

| A | $2 | $50 | Revolving |

| B | $144 | $150 | Repaid Quarterly |

| C | $50 | $64 | Must be Drawn by 12/31/2019 |

| D | $97 | Only available for Aurora Sun |

Now here’s where all the details start to matter.

To convince BMO to loan them the money, Aurora had to agree to certain debt covenants.

From our explanation of debt covenants you know Aurora is now being watched closely by their lenders, and if financials deteriorate enough to trip the covenants, Aurora could quickly be staring down the barrel of a “technical default”.

How Likely is an Aurora Technical Default?

The most important covenant Aurora signed reads:

Based on our estimates and using the company’s most recent balance sheet, Aurora’s required ratio currently sits at 0.15 to 1, well below the allowed maximum of 0.25 to 1.

However, depending on the size of write-downs coming in future quarters, this covenant will look a lot worse.

| Balance Sheet at of September 30th 2019 (In Millions) | |

| Total Funded Debt | 656 |

| Adjusted Shareholders Equity | 4,466 |

| Funded Debt to Equity Ratio | 0.15 |

*Capital Leases Added to Debt. Full covenant definitions at the bottom of the document.

The most likely write-down will come from Aurora’s goodwill and intangible assets.

These assets were created when valuations across the space were frothy to say the least.

With stock prices cut in half and greenhouses selling for pennies on the dollar, we don’t see any way Aurora can convince their auditors to let these values stand.

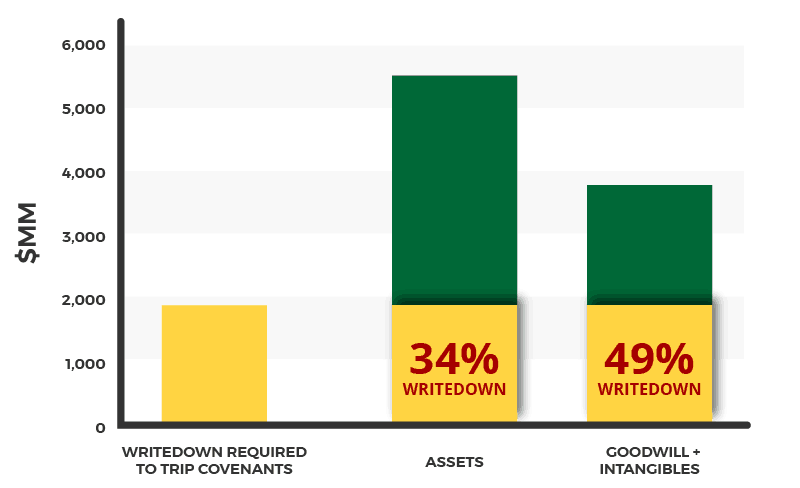

Aurora has C$3.9 billion of goodwill and intangibles, a full 70% of the total book value of the company.

[su_panel background=”#C6E1FF” color=”#110076″ border=”px none ” shadow=”px px px ” radius=”4″ text_align=”center” class=”dw-editor-note”]A write-down any larger than C$1.9 billion would cause Aurora to violate their covenants. Aurora is likely in a heated debate with their auditors as we speak to avoid a write-down of this size.

With cannabis stocks as a whole down 50% and Aurora down more than 60% in the last year, we think it’s highly likely write-downs could exceed C$2 billion.

[/su_panel]Others share our view, with a Bloomberg article quoting an analyst who expects a write-down close to C$2 billion.

Size of the Write-down Required to Create a Technical Default

How Will This All Play Out?

Our best guess for how the timeline plays out looks like this:

- Aurora begins writing down assets next quarter, culminating in a huge goodwill write-down in the June 2020 earnings release when goodwill impairment testing usually takes place.

- Equity value falls below the minimum required in the covenants, tripping a technical default.

- Aurora announces it is in negotiations with secured lenders.

At this point, the timeline is less linear, but we think goes one of two ways.

Scenario 1: BMO Wants Their Money Back

BMO along with other lenders could demand immediate repayment of all C$196 million.

The lenders will make this choice if they think the chances of getting their money back are only going to get worse if they let Aurora stay in business.

Aurora will have to show them a blockbuster rollout of cannabis 2.0 products and a clear roadmap to cutting costs and reaching profitability or else the technical default will turn into a real default.

This scenario is the worst case for investors as the stock price will be trading for pennies at that point.

Scenario 2: Aurora Negotiates a Deal

If the lenders think they will eventually get their money back in 2021, Aurora will be allowed to pay a substantial penalty and renegotiate the covenants.

Lenders will now have Aurora on a very tight leash with veto power on raising new debt, not to mention many other operational decisions.

Aurora is now less nimble than it already was and will have a very hard time raising more debt to keep the lights on, making an eventual default still a possibility.

Though this scenario will allow Aurora to keep operating in 2020, without a dramatic change in profitability the company will just bleed cash to pay interest and won’t be able to come up with the C$200 million due in August 2021.

The Bottom Is Not in for Aurora Stock

We likely haven’t seen the low point in Aurora stock.

Any investors looking to bottom fish should wait to see how large the write-downs are and if BMO decides there is a future for this company.

Until Aurora can resolve the ongoing cash squeeze, the selloff will continue.

APPENDIX

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.