Aurora Cannabis Inc. (ACB) announced a deal this morning to buy MedReleaf (LEAF), another licensed producer, for $3.2 billion CAD.

The deal will be all stock and amounts to a payment of 3.575 Aurora shares for each share of MedReleaf or $29.44 per MedReleaf share. Based on MedReleaf’s latest debt and cash balance the enterprise value of the deal is ~$3 billion.

For Grizzle’s full valuation of MedReleaf click HERE

Bottom Line

Aurora bought CanniMed for a disastrously high multiple (55x funded capacity) earlier this year and now is overpaying for what is basically high cost greenhouse capacity.

Valuations are already inflated in the legal marijuana sector, so most of the deals we have seen this year were at prices that make generating a reasonable return almost impossible.

MedReleaf has a cost structure 60% higher than Aurora and will drive up Aurora’s cash costs in the coming quarter.

We recommend MedReleaf investors sell their shares before the deal closes if the stock approaches $29 per share or sell their converted Aurora shares as soon as the deal closes at the latest. There are much better values and less risk to be found outside of the marijuana industry.

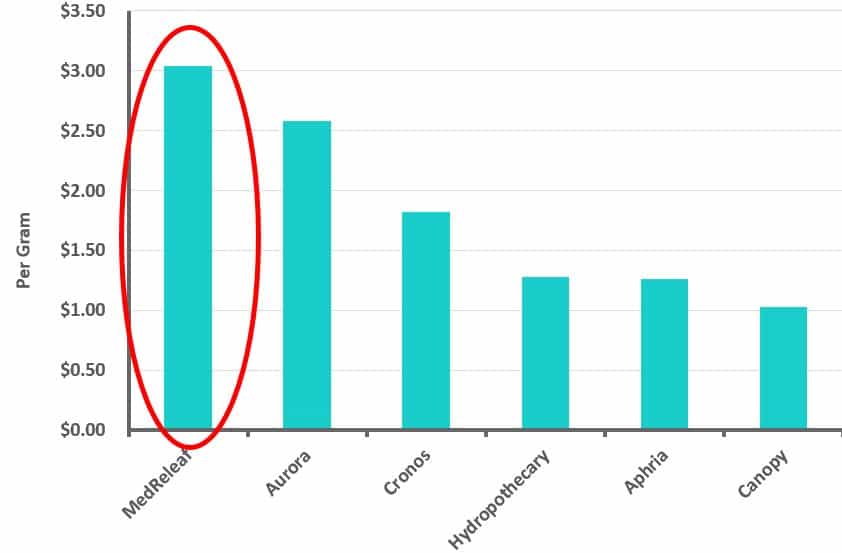

Licensed Producer Costs to Grow and Process Marijuana

Dollar per Funded Capacity

Aurora is paying $21.30 per gram of funded capacity (140,000 kg). To make a 10% return on this kind of premium, Aurora will have to sell MedReleaf volumes (dried and oils) for $12 per gram for the next 10 years. Given that dried flower is selling for $4.50 to the provinces and oil is already selling for about $12 per gram to medical consumers, but falling in price every quarter, we don’t see how blended pricing will come anywhere close to $12 per gram.

Enterprise Value to EBITDA

The $3 billion enterprise value of this deal equates to lofty multiples of EBITDA. Aurora is paying 22x consensus EBITDA in 2021 ($134 million), and even higher multiples of EBITDA in 2019 and 2020 at 58x and 26x respectively.

These multiples are way above even the wine and spirits companies, which are the favourite comparable for analysts due to their strong profitability and high multiples at 15x EV/EBITDA. Grizzle thinks marijuana is a commodity just like oil, gold, or wheat and should trade at a 6x multiple, making the value of this deal even more eye-watering.

Aurora-MedReleaf Deal Multiple Compared to Industry Peers

Closing Thoughts

Aurora Cannabis is growing marijuana for $1.53 per gram and building greenhouses for $1.10 per gram of capacity. Why is management willing to pay $22 per gram for the greenhouses of another licensed producer with growing costs 60% higher than their own ($2.44 per gram)?

The deal rationale doesn’t make sense and once prices start falling and legal supply overwhelms legal demand in 2019, as Grizzle expects, Aurora will never be able to earn an adequate return on this deal.

Investors should park their money elsewhere until the marijuana valuation bubble pops.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.