There have been two housing cycles in the Anglo-Saxon world that never really corrected in the 2008 global financial crisis but continued to levitate. Both of late have been looking increasingly vulnerable. They are Australia and Canada.

The Royal Commission Causes Bank Stocks to Rally

In Australia, this month has seen the release of the long-awaited final report of the Royal Commission on Australian banks. This followed a nine-month-long public enquiry that revealed a lot of evidence of oligopolistic practices by the country’s four major banks.

Since the recommendations are no worse than expected, the banks’ share prices rallied on the report’s publication on Feb. 4, a move doubtless helped by the general “risk on” environment.

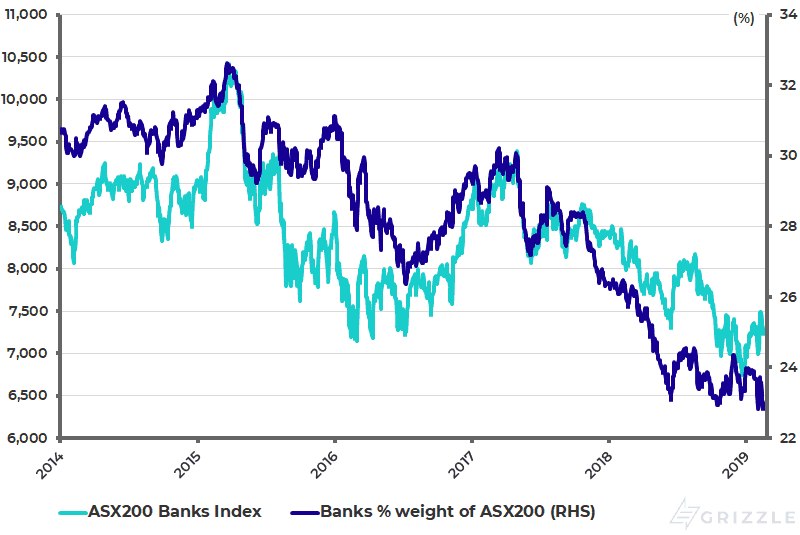

The rally should be seen in the context of the significant domestic underperformance of the Aussie banks in recent years. Australian banks peaked at 32.6% of the ASX200 in March 2015 and were only 22.8% of the index prior to the publication of the final report (see following chart).

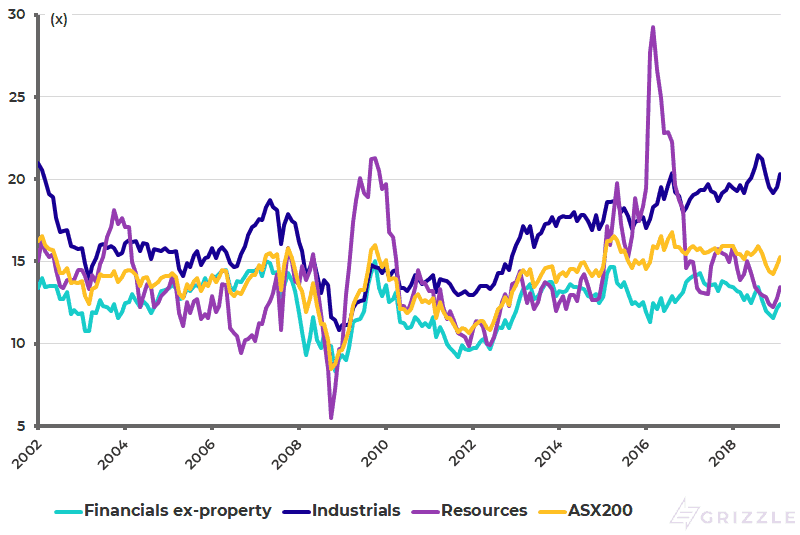

There is clearly potential for renewed outperformance if superannuation inflows start going back into bank stocks. For the record, compulsory superannuation inflows of 9.5% of salaries result in A$1 billion flowing into the Australian stock market every week. These inflows have in the recent past been going into non-bank industrial stocks, resulting in very high valuations. Thus, non-bank industrials trade on 20.3x forward PE compared with 12.4x for the banks and 13.5x for the resource mining stocks (see following chart).

ASX200 Banks Index and Australian banks’ Weighting in the ASX200 Index

Australian Banks, Resources and Industrial Stocks Forward PE

Such a renewed flow into bank stocks is certainly quite possible. Still, there remains significant downside for Aussie banks’ share prices if they ever have to cut their enormous dividends. The big four banks have an average 2019 forecast dividend yield of 6.7% and an average dividend payout ratio of 76%. But an average loan-loss provision of only 13 basis points for the four major banks means there is little margin for error in terms of any decline in asset quality.

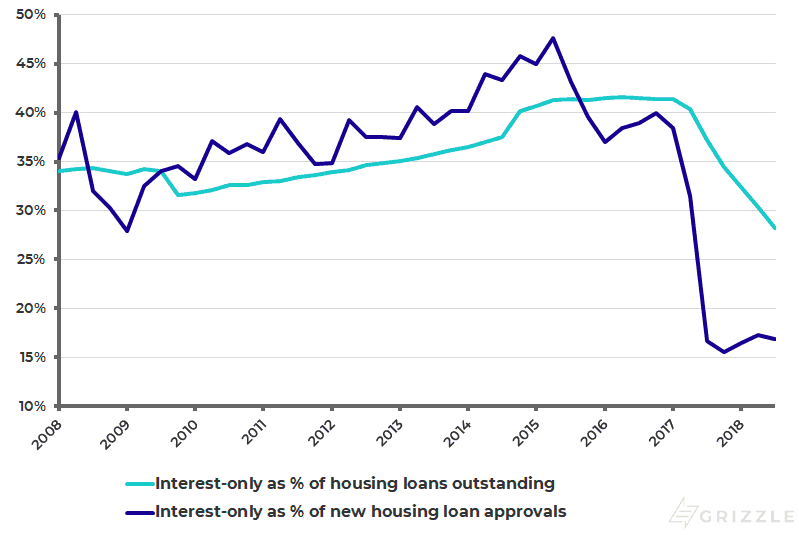

A huge 65% of the four major Australian banks’ loan portfolios are in residential mortgages. While the risk of a bad loan cycle in mortgages is reduced by the reality that mortgages in Australia are “full recourse”, reflecting the country’s colonial era bankruptcy laws, interest-only loans converting to repayment mortgages are an area of obvious risk in terms of asset quality. SME loans could be another. The major banks still have 28% of their mortgage portfolios in interest-only mortgages, though down from a peak of 42% in 2Q16 (see following chart).

Australian Major Banks’ Interest-only Mortgages

Labor Party’s Bank Bashing Could Harm Banks and the Property Market

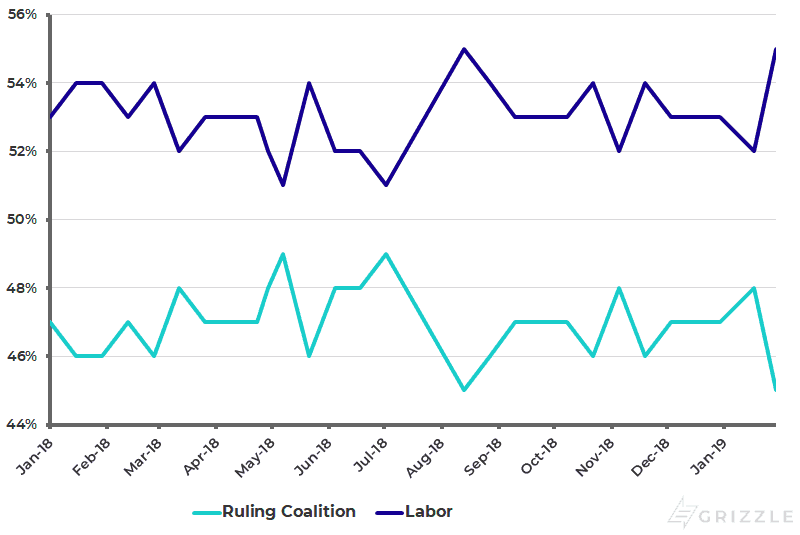

Meanwhile, the Royal Commission’s final report provides an ideal opportunity for the opposition Labor Party to indulge in bank bashing in the run-up to the Federal election due to be held before May 19. The big risk for the banks, and Australia’s property market, is the Labor Party proposal to end the “negative gearing” tax deduction on residential investment property.

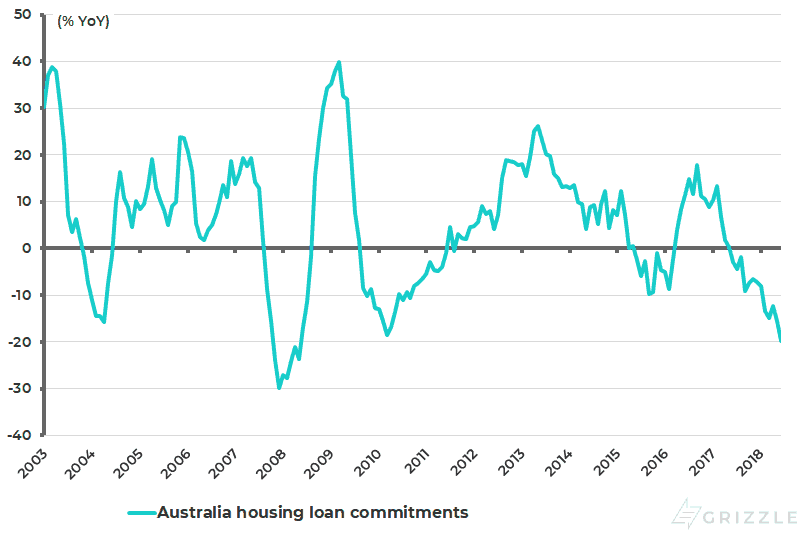

The above is relevant since Labor is still leading in the polls. A poll conducted on Feb. 6-11 by Essential Research shows Labor with a two-party lead of 55-45 against the ruling Coalition (see following chart). While it is quite understandable why a socialist party should want to end such a tax break that favours the wealthy, since only people with some capital can own a residential property, the hope of both the banks and leveraged owners of investment property will be that the growing evidence of a property downturn, and a related decline in property-related lending (housing loan commitments declined by 19.8%YoY in December, see following chart), will prompt a Labor Government, if elected, to refrain from implementing such a policy. This is certainly possible since the homeownership rate in Australia is 65%. This is also probably the reason why the Royal Commission pulled its punches in terms of not coming up with more aggressive recommendations in terms of tougher regulation.

Australia Federal Election Voting Intention – Two-party Preferred Estimates

Australia Housing Loan Commitment Growth

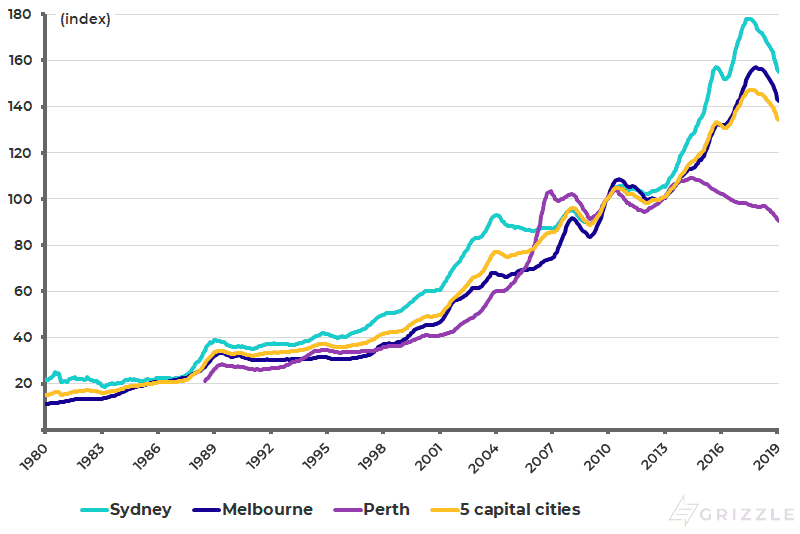

For now, the latest evidence is that house prices continue to decline in Sydney and Melbourne. The CoreLogic Sydney and Melbourne home price indices declined by 10.1%YoY and 9.0%YoY on Feb. 17, and are down 12.9% and 9.4% from their peak reached in 2017 (see following chart). This is the context of Australia’s huge household debt. The household debt to GDP ratio is running at 189%, with mortgage debt at 140% of GDP.

CoreLogic Australia Hedonic Home Value Index

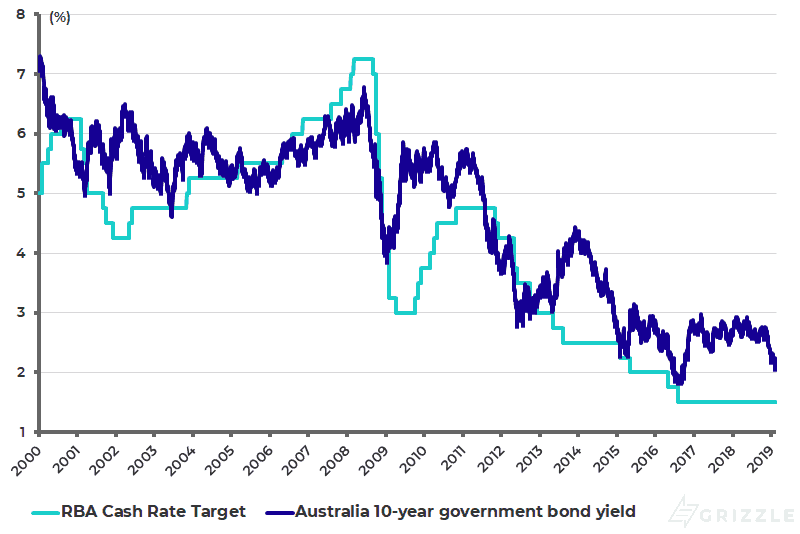

This growing evidence of domestic asset deflation in a country with such high household debt is presumably why the governor of the Reserve Bank of Australia, Philip Lowe, stated in a speech earlier this month that the next move in the cash rate could be down, as well as up. This was the first admission by the central bank that it may have to cut rates again. The cash rate is now at a record low of 1.5% (see following chart).

Australia 10-year Government Bond Yield and RBA Cash Rate Target

While it may have suited the Aussie central bank politically to concede that another easing may be necessary at a time when the Fed had just done its dovish lurch, in terms of what has been called “Powell’s Pivot”, the reality is that the driver in Australia’s case is purely domestic considerations. All this means that investors should remain “long” long-term Aussie government bonds in a context where the cash rate could end up at zero.

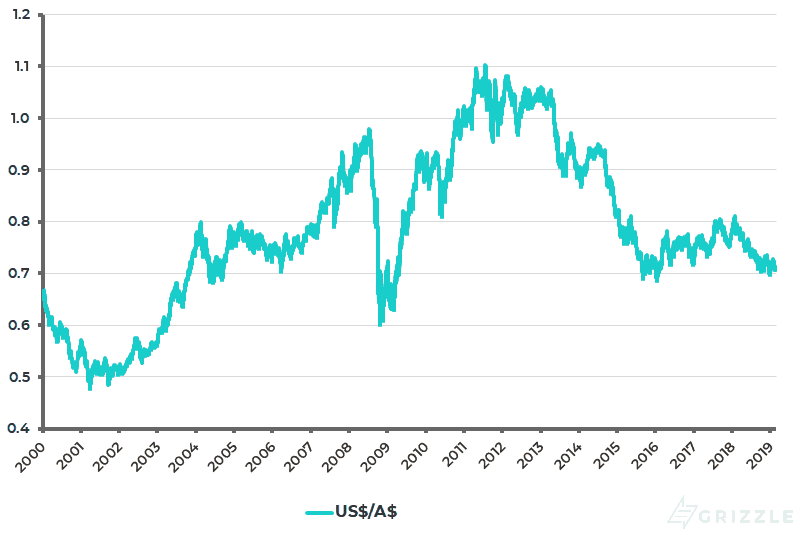

Further monetary easing represents an obvious risk to the Australian dollar, which has already declined by 35% against the US dollar from the high reached in July 2011 (see following chart).

Australian Dollar Against the US dollar (U$/A$)

The views expressed in Chris Wood’s column on Grizzle reflect Chris Wood’s personal opinion only, and they have not been reviewed or endorsed by Jefferies. The information in the column has not been reviewed or verified by Jefferies. None of Jefferies, its affiliates or employees, directors or officers shall have any liability whatsoever in connection with the content published on this website.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.