Alteryx, Inc. (NYSE: AYX), a leading provider of end-to-end analytics platform released their second quarter fiscal 2020 earnings that beat top and bottom analyst estimates, but shares tumbled after-hours due to weak guidance.

Revenues came in at $96.23M, which was higher than analyst estimates of $94.11M by 2.3%, and up by 17.3% year-over-year. This was above management’s revenue guidance of between $91M to $95M.

Regarding its two primary business segments, Subscription-based software license revenue decreased by 5.9% since last year, while PCS and Services revenue increased by 36.3% year-over-year.

The company’s earnings per share was $0.02/sh, which beat analyst expectations of ($0.14)/sh by 114%. This value was also higher than management’s expectations of being between ($0.18) to ($0.12).

EBITDA for the company came in at $6.44M, which was above the street consensus of ($8.54)M by 175.4%

Alteryx’s also grew their client base by 27.2% year-over-year to 6,714 customers.

Outlook

Regardless of great operational performance this quarter, analysts and investors do not seem to be happy about management’s weak expected revenue growth for next quarter.

According to management, revenue for Q3 is expected to be in the range of $111-$115 million, which is below consensus estimates of $119 million.

When Saas Stocks are tanking even when they give guidance that exceeds expectations, it was inevitable Alteryx was going to crash the minute management gave guidance below consensus.

Valuation Overview

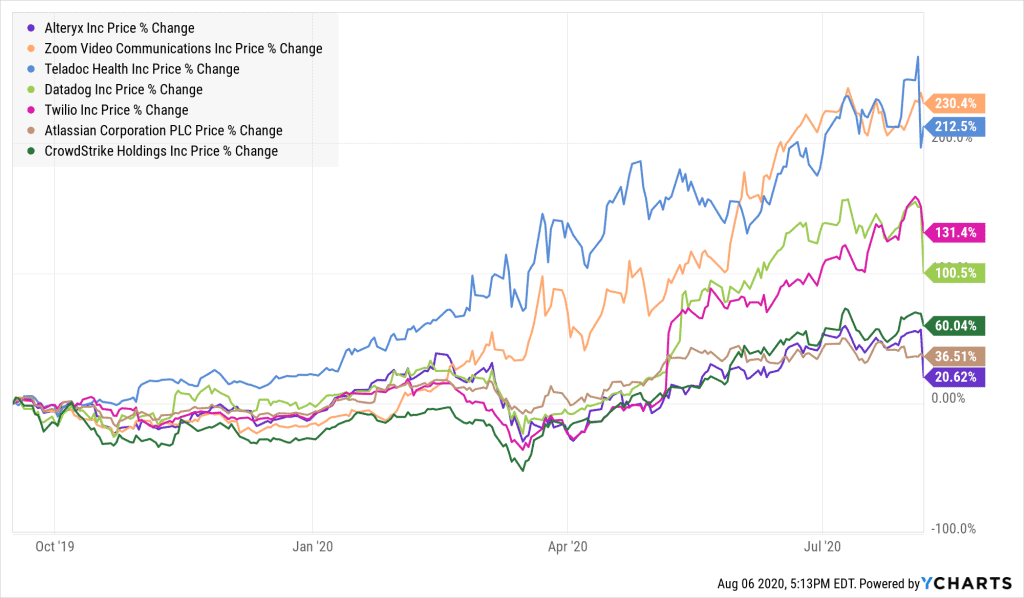

As is the case with most other tech companies seeing a rise in their share prices during this time period, Alteryx shares has risen by 20.62% so far. However, its share performance is on the lower end of the spectrum along with Atlassian and CrowdStrike as shown below.

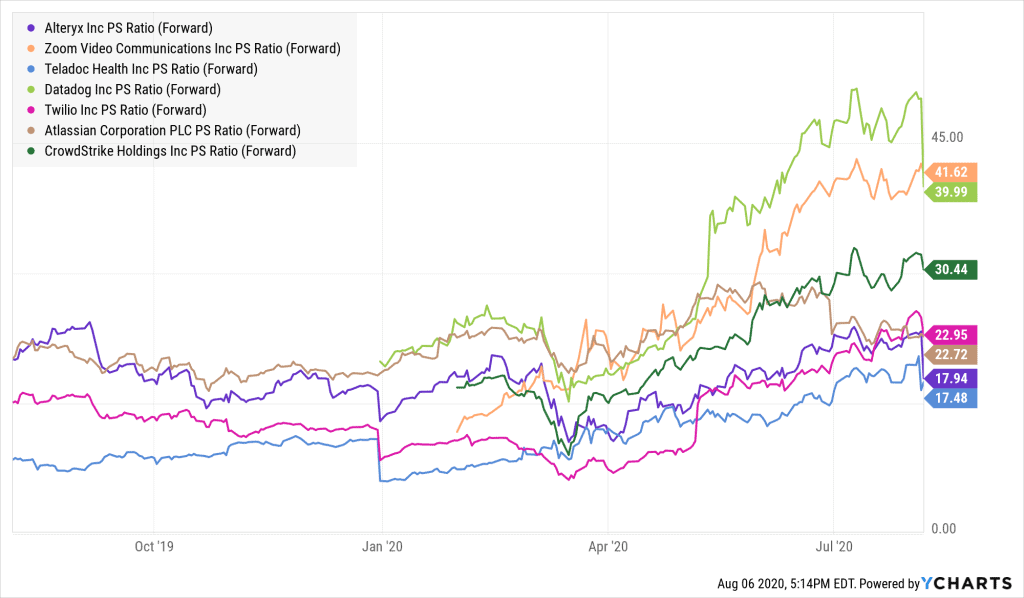

Although having a higher price to sales multiple compared to companies outside of the sector, Alteryx seems to have one of the lowest PS multiple amongst its peers according to the following chart.

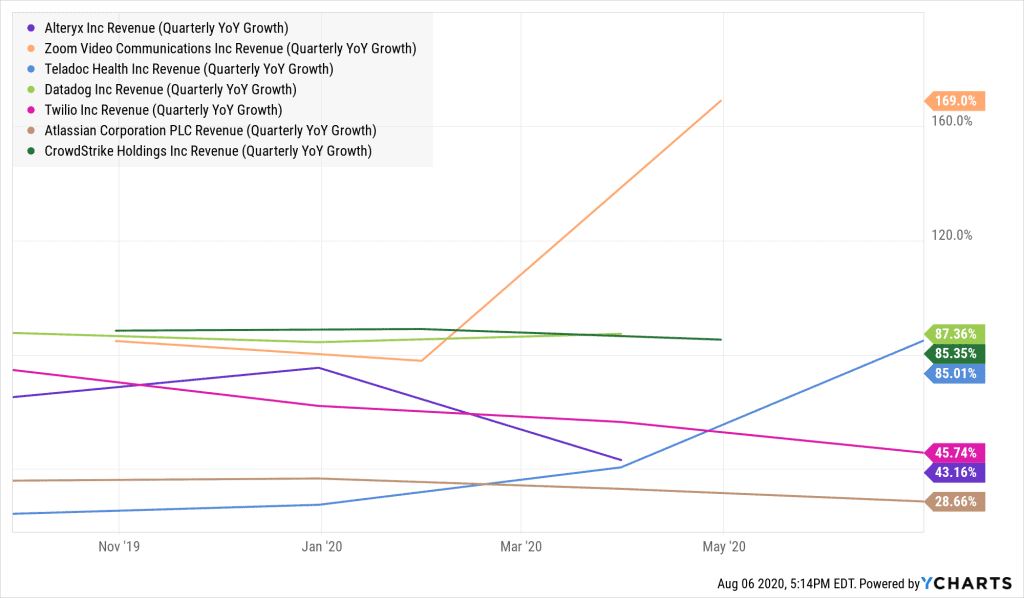

This is justifiable when considering the fact that its quarterly year-over-year revenue growth ranks second last, at 43.16% as shown below.

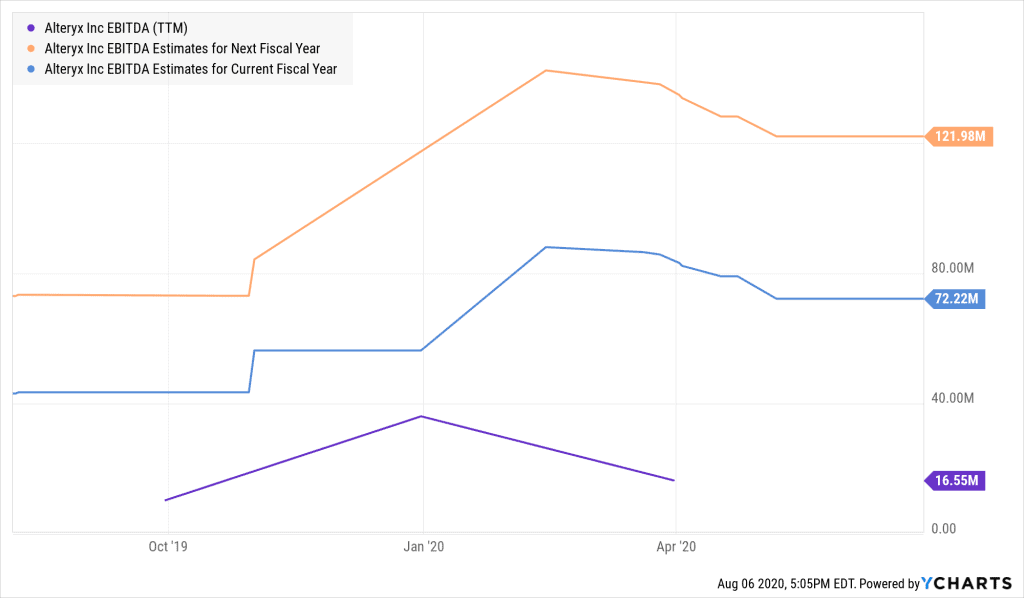

However, due to the fact that the street expects this company to see a 336% upside for its EBITDA to run in the current fiscal year, and 68.9% of upside from the current fiscal year’s EBITDA to their next fiscal year, suggests that Alteryx will continue to be a viable contender in the tech space.

Final Remarks

If you wish to invest your capital into Alteryx, keep in mind that most tech stocks have already risen up significantly so far, and any further let down in revenue growth will see its shares meet the same fate as it is experiencing currently after-hours.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.