Global oilfield services firm Baker Hughes (NYSE: BKR) announced results that sorely missed expectations.

Revenue came in at $6.35 billion, 2% behind consensus of $6.47 billion, while earnings per share of $0.07 missed the consensus estimate of $0.31 by 75%.

Even if we back out impairments, EPS of $0.27 missed consensus by 13%. Baker Hughes put up the first adjusted EPS miss in the group and the market will likely not be happy.

Results included write-downs and impairments of $216 million, a regular occurrence for Baker Hughes lately.

Full-year revenues were up 1% compared to 5% growth in 2018 over 2017, demonstrating a tough environment for oil and gas companies.

In the medium term, there is not much to get excited about with flat oil prices and belt-tightening among many customers.

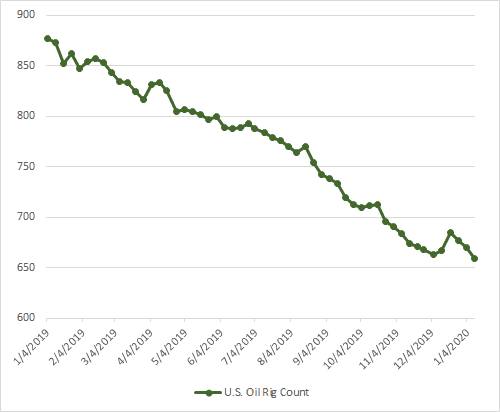

Results were disappointing with revenue in the U.S. falling 11% compared to a U.S. rig count that declined only 5% in the fourth quarter.

Weak pricing obviously continued in the U.S. as oil producers pull back on activity in key shale basins to rationalize spending.

Even though the analyst community likes to back out every write-off and call it one time, impairments like the ones Baker Hughes saw this quarter are why this sector has trouble earning its cost of capital over time.

Write-offs are portrayed as being one time but looking through history we can see it has certainly not been a one-off with regular write-offs during periods of contraction and falling oil prices.

U.S. Oil Rig Count Decline Continued in the Fourth Quarter

Segment Performance

In the fourth quarter, the Turbomachinery (LNG) and Digital Solutions groups were the worst-performing segments for the company, down 8% and 5% on a year-over-year basis while Oilfield Services was the best performing up 7% year over year.

OFS Revenue in the U.S. was down 11% over last quarter while international revenue increased 4%.

North America continued to see weak results from a pullback in rig count and a fall in pricing and shale activity.

Energy Off to a Tough Start in 2020

So far this year, oilfield service stocks and energy stocks in general, are underperforming the broader market as stock prices cool off after international tensions between Iran and the U.S. caused oil prices to spike temporarily.

Baker Hughes stock is down 4.5% this year while competitors Schlumberger and Halliburton are down about 4.5% and 2% respectively. U.S. equipment provider National Oilwell Varco is down more than 7%.

This compares to the S&P 500 which is up 1% for the year.

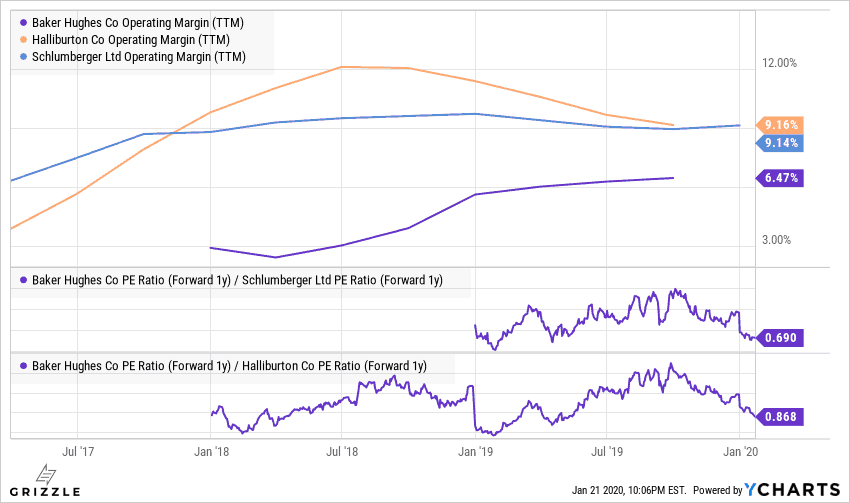

Baker Hughes is more diversified than peers but is still being hit by stagnant oil prices and rising material and labor costs.

The company is less profitable than peers Halliburton and Schlumberger which is reflected in the multiple discount.

Baker Hughes multiple has been falling against peers in the last few months even as the margin profile improves.

The weak stock performance in 2020 so far is likely due to market expectations of upcoming weakness in non-drilling related businesses.

Baker Hughes Less Profitable and Trades at a Discount to Peers

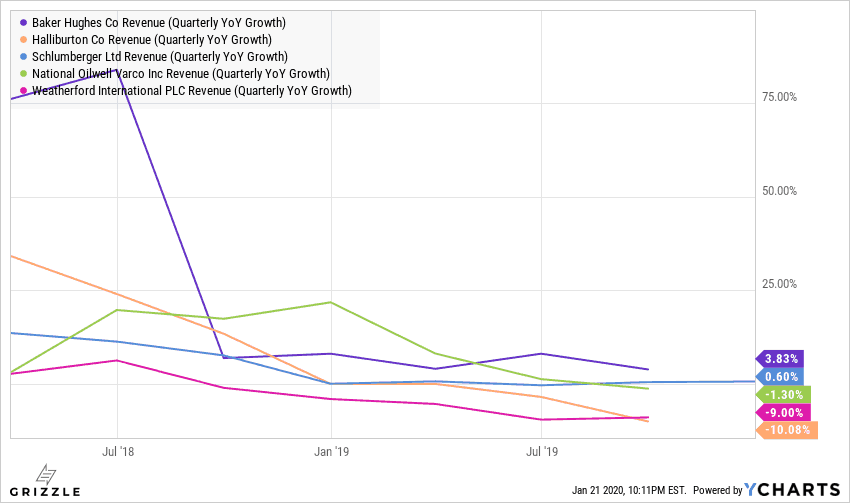

The problem all these companies face is that revenue growth is slowing, dragging stock prices down with it.

After 12 years of investing in oil and gas markets professionally, our advice is to avoid these stocks until the oil price is rebounding in the early days of an economic recovery.

All other times, this sector is going to underperform long term growth stories in technology where your money should really be invested.

BKR Revenue Growth Best in the Group

Ongoing geopolitical strife has not had a meaningful positive impact on oil prices yet, likely due to the significant excess capacity of OPEC.

The transition away from fossil fuels to renewables also represents an existential threat to the industry and will not help the flow of investor dollars into the sector in our opinion.

We think investors would be better served investing in tech names instead of an oil industry that has failed to generate meaningful gains for investors for far too long.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.