Capital markets sell-side research has been known for overly optimistic forecasts (think dot-com bubble).

One of the biggest reasons for this positive slant is the natural conflict of interest between research and investment banking. No companies want to work with a bank whose analysts are bashing their stock. It’s just how the business goes.

Unfortunately for marijuana investors, this time is no different. In this piece we tear apart the estimates that make up Bay Street’s $40 price target for Canopy Growth Corporation (TSE:WEED) so our readers can judge for themselves if positive bias has really permeated the marijuana research houses. Once you see what the future needs to look like to justify a higher stock price you can make more informed investment decisions.

So What’s in a Stock Price?

The average target price of Canopy Growth among the analyst community is $40 per share representing 31% upside from the current price. To fully understand what the marijuana market needs to achieve to justify a $40 stock we will look at output, price per gram, EBITDA margin and the trading multiple of the stock.

Revenue = Price per Gram x Output

We will build up to revenue forecasts by looking at its two components, price per gram and output.

Output – The average analyst forecasts goes out to 2020. In that year they see Canopy producing 311,000 kg, generally in line with management guidance. Nothing crazy going on in this part of the forecast. There is always a risk that construction progresses slower than expected and the volumes are slower to come online, but so far management teams have executed fairly well on their construction timelines.

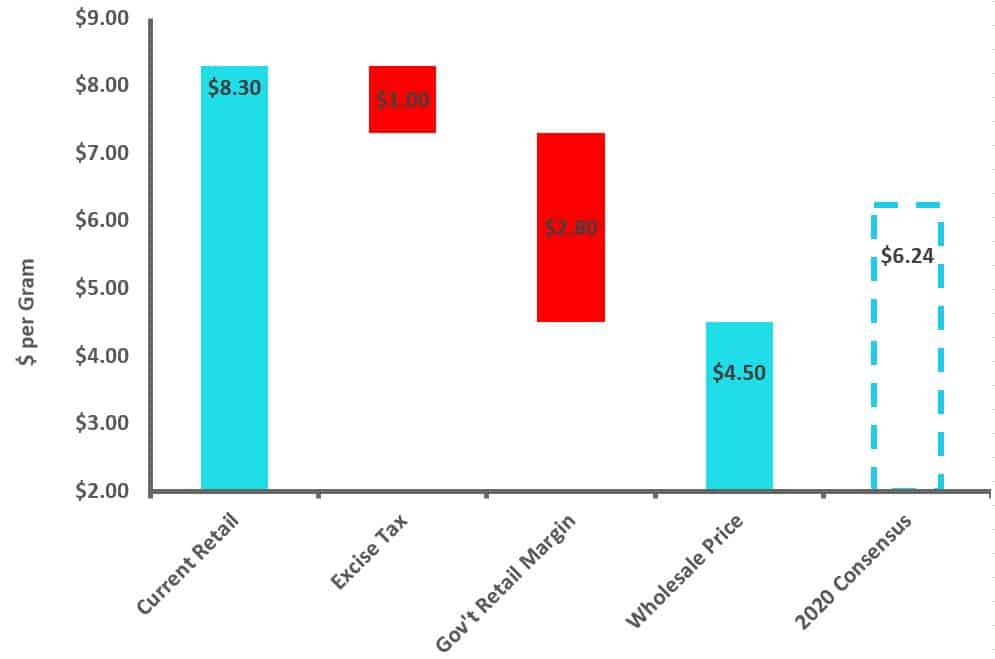

Price Per Gram – This is the most important estimate to determine the value of Canopy Growth. Canopy’s current selling price is $8.30 per gram ($7.20 for flower, $17 for oil). Analysts expect a blended selling price per gram of $6.24 in 2020, 25% lower than today. For reference, pricing in legal US states fell 70%-80% 2 to 3 years after legalization while in Canada prices in the black market are falling 6% a year.

If we assume that 50% of revenue will come from oil sales in the future, similar to Colorado, and flower will sell for $4.50 a gram (close to what the provinces are paying today) analysts are assuming oil revenue will be $10/gram. $10 may be tough to sustain when provinces are currently offering $8 per gram or less for oils.

Important: Canopy doesn’t currently pay excise tax ($1 per gram) and is still selling direct to consumers, generating higher margins than when they start selling to government-owned retail stores (75% of Canada will be serviced by government stores). When we include the excise tax, analysts think prices are only going to fall 12% in the next 3 years.

Spot Legal Prices in the US

Let’s assume the current $8.30 per gram selling price is the maximum customers or insurance providers are willing to pay. Once Canopy becomes a wholesaler it must absorb the $1 per gram excise tax and at least another $2-$3 based on current negotiations with the provinces. So right off the bat in 2019 Canopy could be generating revenue per gram of $4.50, well below analyst expectations and we aren’t even including a decline in pricing from any oversupply of product in Canada.

Expected Retail Prices in 2020

EBITDA Margins

Marijuana stocks are priced on an Enterprise Value (value of stock plus debt less cash) to EBITDA multiple because of their lack of net income. The ultimate EBITDA margin Canopy can achieve once the market has matured will determine the cashflow potential of the business and the future value of the stock.

The Industry Today

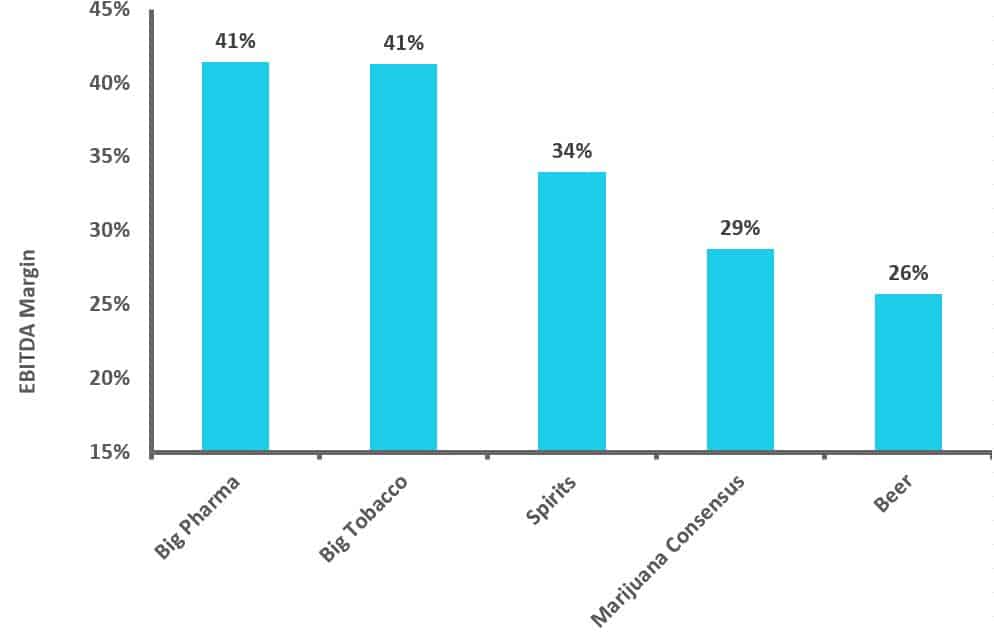

Licensed producers as a group generate negative EBITDA, and even the most profitable producer, Aphria, only has a 10% EBITDA margin if we adjust stock-based compensation to a more normal level (5% of revenue).

Consensus expects 29% EBITDA margins in 2020, which are doable if the industry operates like the beer, spirits, or pharmaceutical industries. Forecasting EBITDA margins is the most uncertain part of this entire analysis due to the uniqueness of the marijuana industry and lack of historical precedent.

The ultimate margin will all depend on how far management can drive down payroll, R&D, and marketing costs and the revenue per gram they can generate by selling internationally and to the provinces.

EBITDA Margins of Industries Compared to Marijuana

It All Comes Down to the Multiple

The multiple of EBITDA the market is willing to pay is the single largest determinant of where Canopy’s stock price can go. This is also where we see the most downside for stocks if investor sentiment weakens. The multiple is determined by a few factors such as revenue growth compared to the broader market and how profitable the company will ultimately be (EBITDA margin).

A $40 target price for Canopy implies a 17x multiple on 2020 EBITDA of $560 million. This is higher than all the industries analysts like to compare marijuana to such as beer (10x), Big Pharma (12x), Tobacco (12x) and even wine and spirits (15x). If Canopy doesn’t grow revenue 160% a year and achieve an EBITDA margin of 29%, the multiple is going to fall.

If you buy Canopy Growth Corp at $30 what are you betting on?

When you buy a stock expecting to make money you are betting that the future will look better than the past. In the case of Canopy Growth, Bay Street analysts are betting that the following four things will happen.

- Canopy will sell marijuana (flowers, oils, edibles) for $6.24 per gram ($4.50 for flower, $10 for extracts) on average in 2020.

- EBITDA margins will be 30% in 2020, up from -33% in the most recent quarter.

- The stock justifies a multiple of 17x EBITDA in 3 years, 50% more than the average stock in North America and 10x higher than commodity producers such as oil companies and gold miners.

- New greenhouses will grow 311,000 kg annually of marijuana, up from 8,000 kg today.

As the above illustrates, a $40 Bay Street price target bakes in a very Utopian future — strong pricing, big margins, high multiples and lightning fast growth. As an investor you never want to buy a stock when it is pricing in perfection and unfortunately this is just the situation the marijuana capital markets find themselves in today. When the black market (i.e. home grow) can make you a 200%+ return even if you lose half your crop, why would anyone get involved with low margin of safety marijuana stocks. As always buyer beware.

READ THE MARIJUANA EXPORT MIRAGE FOR AN IN-DEPTH REPORT ON THE STATE OF DEMAND FOR MEDICAL MARIJUANA OUTSIDE OF CANADA

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.