China’s abrupt but welcome Covid U-turn creates the best chance in many years for Asia and emerging market equities to outperform on a sustainable basis given the prospect in 2023 for earnings downgrades in America and the reverse in China, the positive implications for commodities of a China reopening, and the likely weakening of the US dollar in the event of the anticipated U-turn by the Fed.

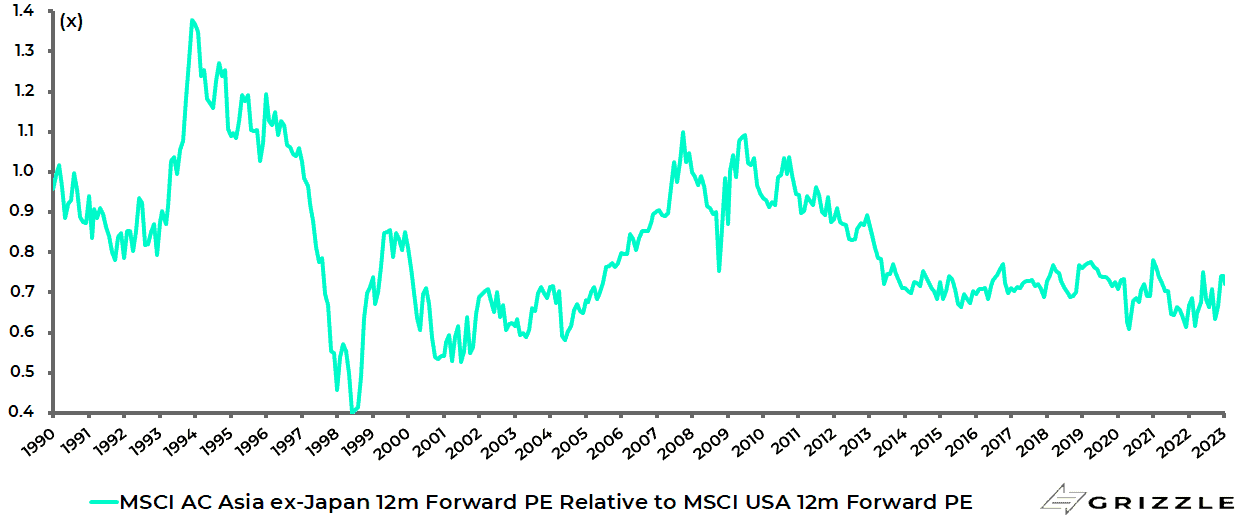

Meanwhile, valuations in Asia also remain far more attractive than in the US. The MSCI Asia ex-Japan Index now trades on 13.5x 12-month consensus forward earnings, or a 28% discount to the MSCI USA’s 18.7x.

MSCI AC Asia ex-Japan 12m forward PE relative to MSCI USA 12m forward PE

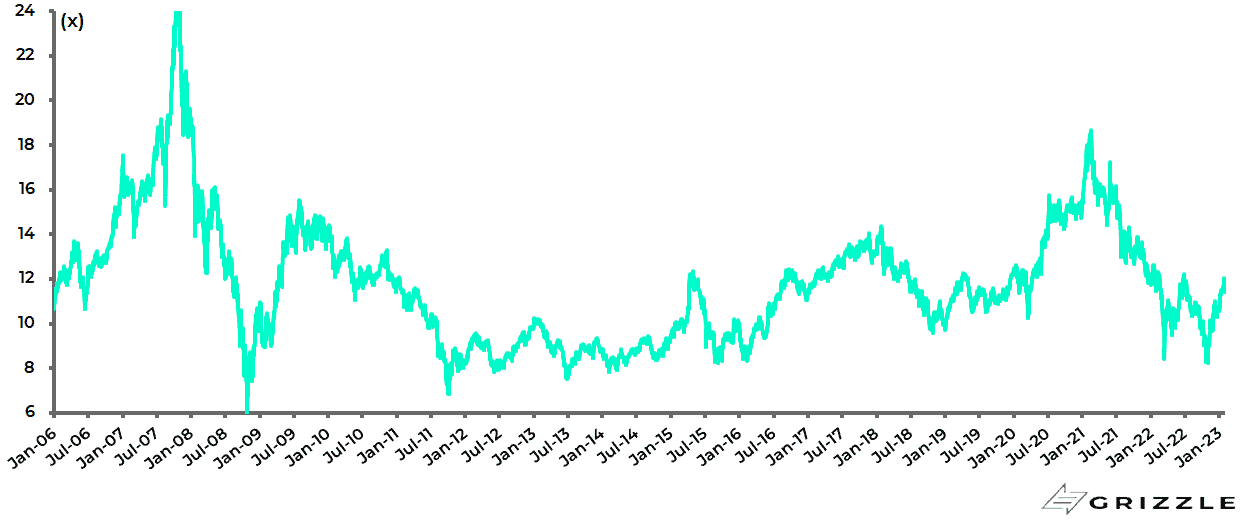

As for China, the MSCI China now trades at 11.4x 12-month forward earnings, though up from a low of 8.25x reached in late October.

MSCI China 12m forward PE

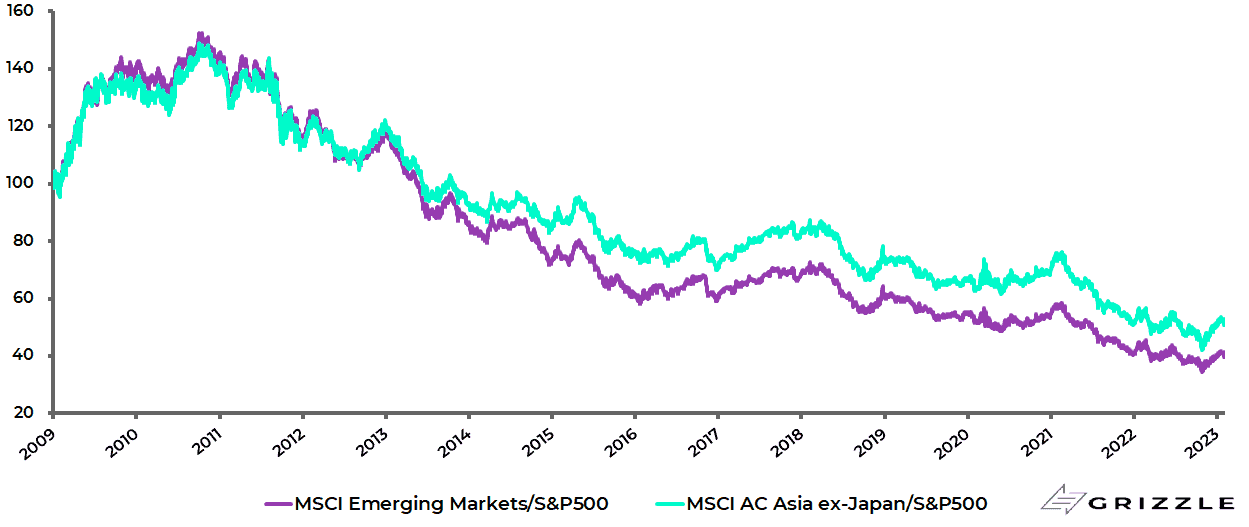

Sustained outperformance for Asia and emerging markets is certainly long overdue since the S&P500 had, as at the end of 2021, outperformed the MSCI AC Asia ex-Japan and the MSCI Emerging Markets indices by 188% and 271%, respectively, since October 2010.

Still last year, the US market performed almost in line with the global benchmark.

The MSCI America underperformed marginally, declining by 20.8% in 2022, compared with a 19.8% decline in the MSCI AC World.

While the S&P500 marginally outperformed declining by 19.4%.

MSCI Emerging Markets and Asia ex-Japan relative to S&P500

India Expensive in the Near Term, Attractive Longer Term

If Asia looks better in aggregate on comparative valuations, there is one market where valuations are undoubtedly challenging.

That is this writer’s long-term favourite, India.

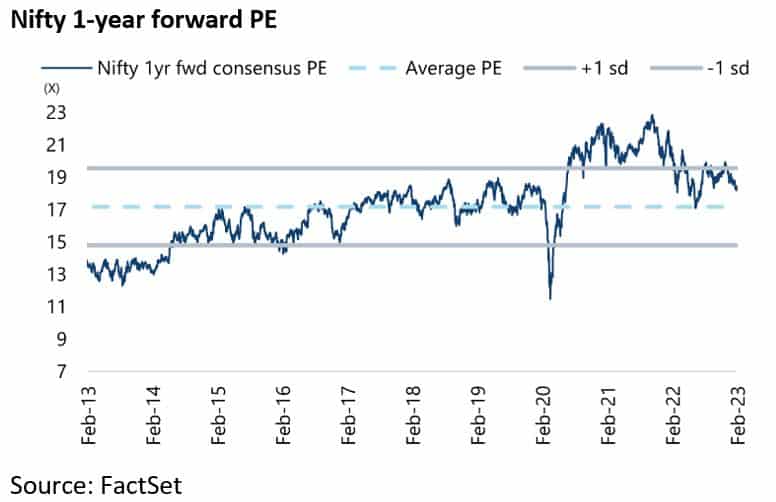

The Nifty Index now trades at 18.4x 12-month forward earnings, compared with a historic 10-year average of 17.2x.

If this is somewhat of a concern tactically, India remains by far the best domestic demand story structurally in the Asia and emerging market universe.

It is also the case that there should be some valuation discount as regards China given the sheer unpredictability of policy responses witnessed over the past two years. Still, such longer-term considerations should not stop investors betting on China reopening now.

Treasury Bonds Positioned Well Compared to Stocks

Meanwhile world stock markets faced two conflicting drivers at the start of 2023, one negative and one positive.

The negative is the mounting prospect of a US recession later this year for a US stock market which, despite the 19.4% decline in the S&P500 in 2022, has not yet fully discounted the earnings downgrades that would eventuate in such a recession.

For the equity correction last year was primarily about multiple contraction driven by higher interest rates.

This is why the Ark Innovation ETF, with its profitless tech thematic, ended 2022 down 80% from its high recorded in February 2021.

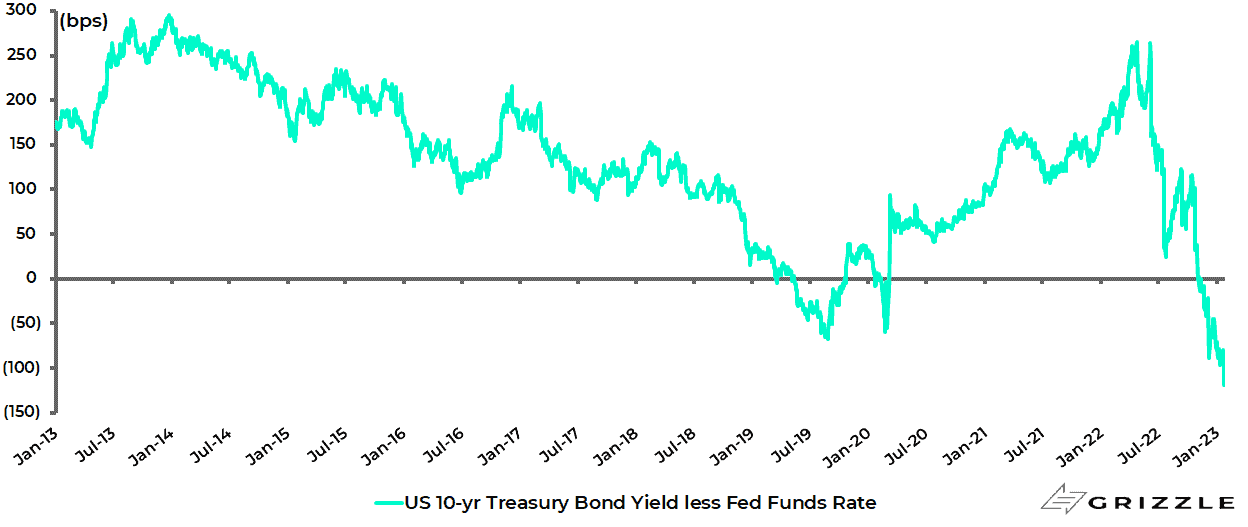

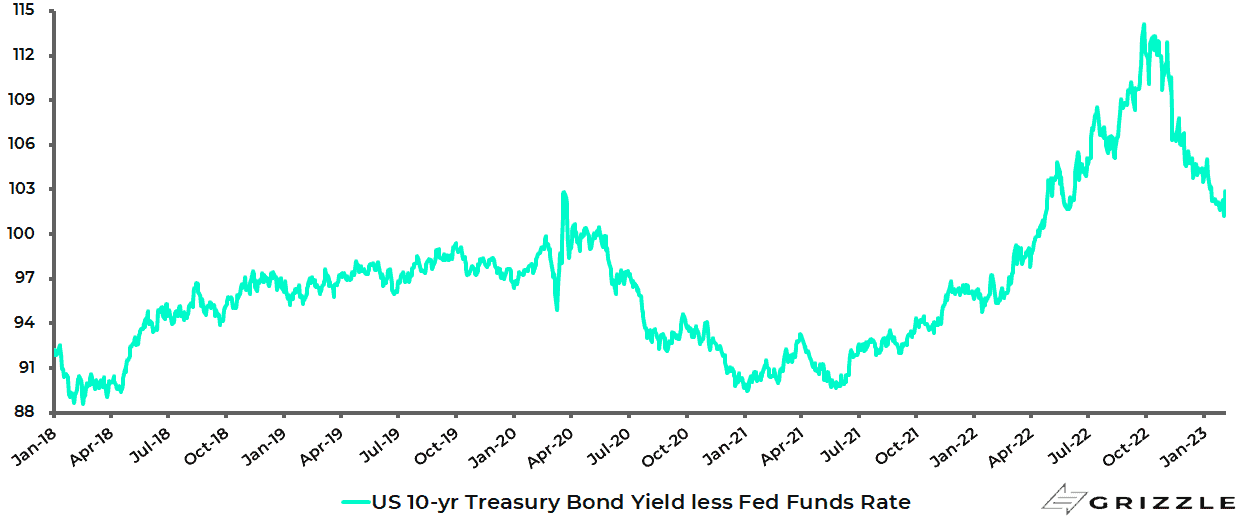

If this is the negative, and it is a negative that in this writer’s view has yet fully to play out, the positive is the potential for a dramatic U-turn in Federal Reserve policy in 2023 when the American central bank suddenly focuses on the mounting recession risk, a risk which has already been signaled by the inversion of the yield curve since mid-November, in terms of the 10-year Treasury bond yield declining below the federal funds rate.

The spread between the 10-year Treasury bond yield and the Fed funds effective rate declined from 116bp in late October to a negative 14bp in mid-November, and is now minus 106bp.

US yield curve (10Y Treasury bond yield – Fed funds effective rate)

The key point will then become whether the Fed gives greater priority to fighting recession over getting inflation below its 2% target since it is unlikely, though not impossible, that headline inflation will have fallen below that level by then.

The Dollar has Likely Peaked

Meanwhile, the view remains that monetary tightening expectations peaked for this cycle after Fed chairman Jerome Powell’s press conference following the November FOMC meeting on 2 November.

At that point money markets were projecting a peaking out of the so-called terminal rate in this cycle at 5.15%.

They are now projecting the terminal rate peaking at 5.0% which implies only 44bp more of rate hikes.

Such an outcome also suggests the US dollar may have peaked.

For now the US dollar index is down 10.3% from the peak reached in late September, a peak which almost coincided with the peaking out of monetary tightening expectations.

US Dollar Index

Still it should be noted that there is a possibility of one last spike in the US dollar in this cycle driven by a deleveraging dynamic on rising recession concerns in an environment where nominal growth is slowing, in terms of dollar revenues, but economic actors still need to service US dollar debts.

The US$13tn of outstanding US dollar-denominated debt owed by non-bank borrowers outside America is clearly an issue here, as well as the US$19.8tn and US$18.8tn of American corporate and household debt.

Still, any such dire outcome will only serve to accelerate a Fed U-turn since it will likely trigger a related surge in credit spreads.

Beware the Great Passive ETF Unwind

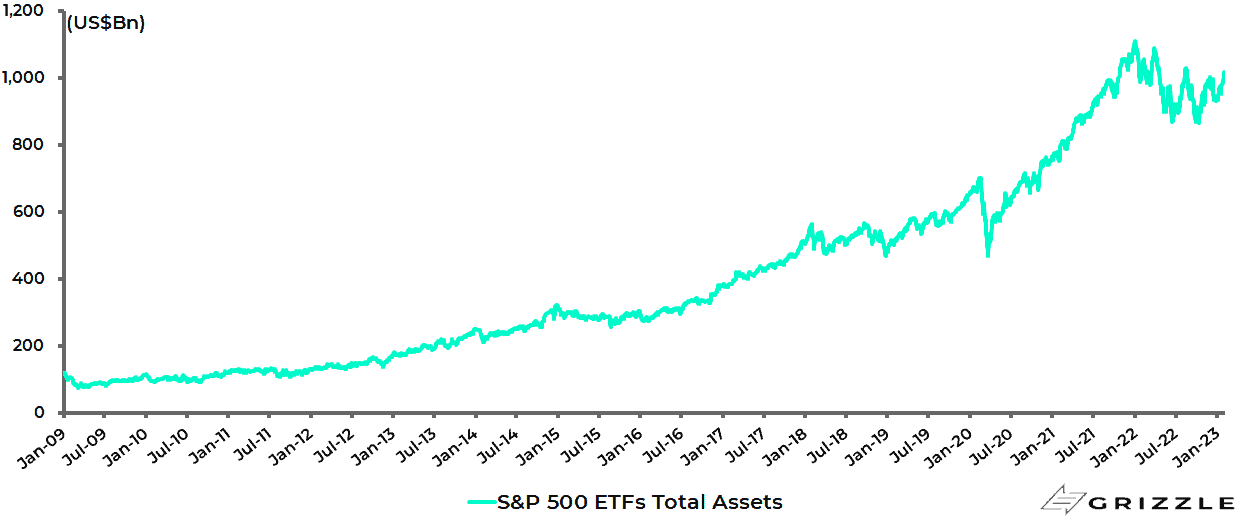

Meanwhile from a US stock market perspective, investors should also remember the potential for the long overdue unwinding of passive-driven investment strategies.

S&P500 index ETFs peaked out at a size of US$1.11tn on 3 January 2022 and have since then barely declined to US$1.01tn.

S&P500 ETFs total assets

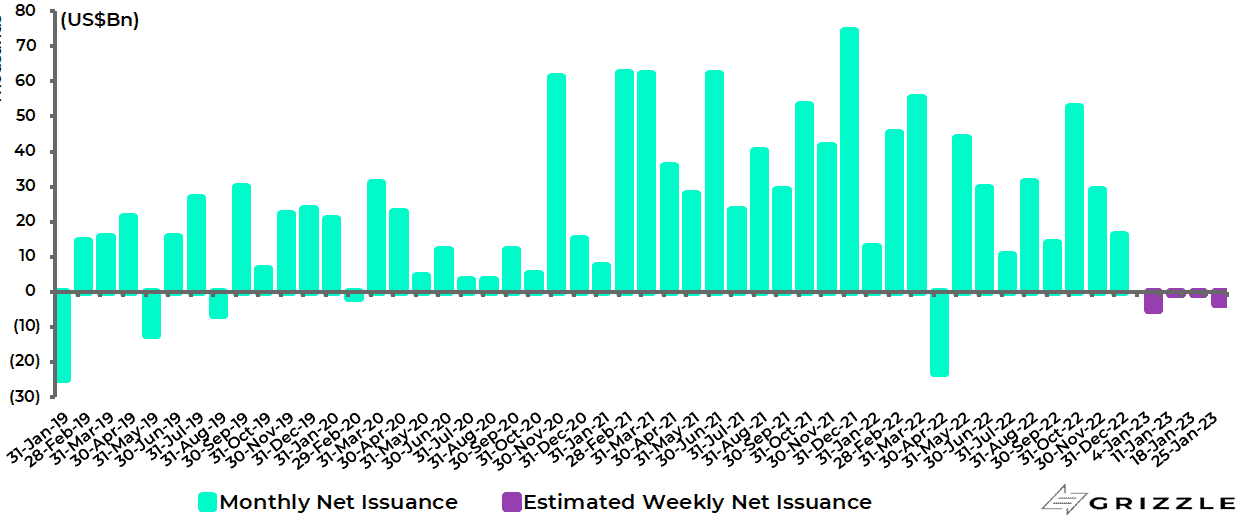

It is also the case that there has, so far, been only one month of net outflows out of domestic equity ETFs during this Fed tightening-triggered bear market.

Indeed US domestic equity ETFs recorded net inflows of US$318bn last year despite an outflow of US$23.2bn in April.

US Domestic Equity ETF Flows

The views expressed in Chris Wood’s column on Grizzle reflect Chris Wood’s personal opinion only, and they have not been reviewed or endorsed by Jefferies. The information in the column has not been reviewed or verified by Jefferies. None of Jefferies, its affiliates or employees, directors or officers shall have any liability whatsoever in connection with the content published on this website.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.