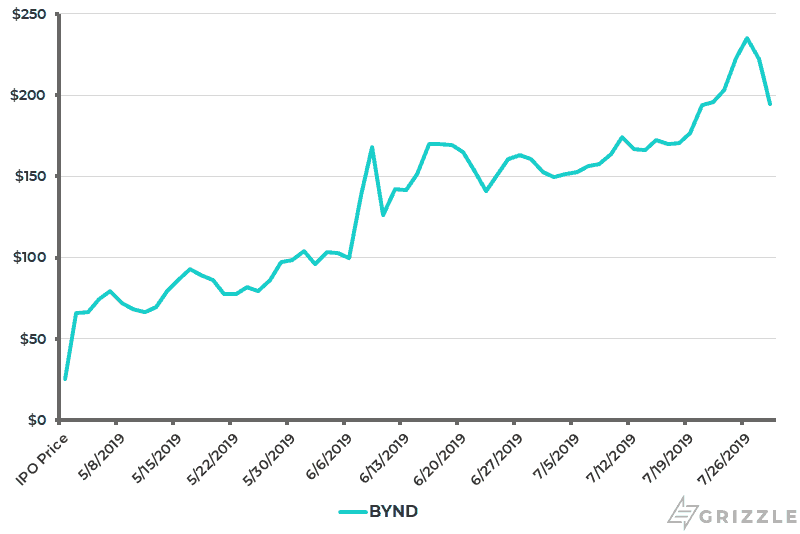

Beyond Meat (NASDAQ: BYND) announced Q2 2019 earnings after the close yesterday, beating analyst estimates significantly across the board once again. If it wasn’t for the share offering (more on that later) the stock would have certainly gapped higher — instead we saw the shares sell down (-12%) — modest in the context of how much the stock had run post the IPO.

Beyond Meat Share Price ($/share)

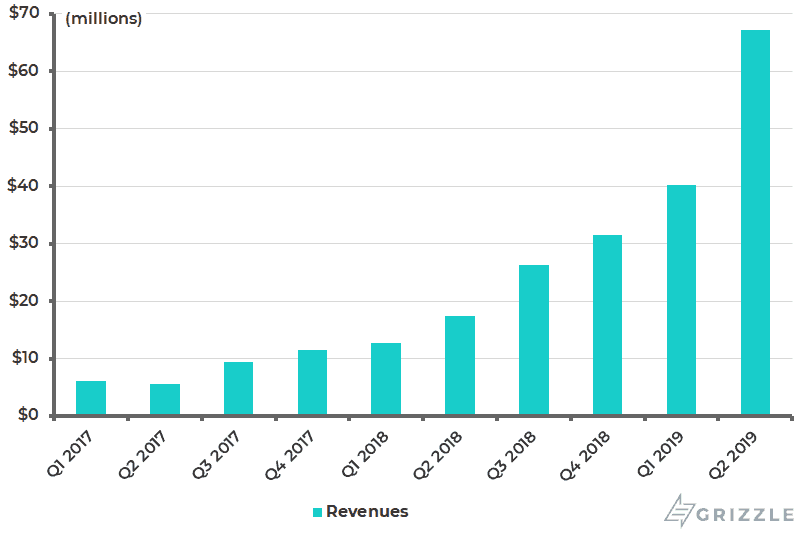

The only number that matters for a hyper growth company like BYND is top line sales; net revenue came in at $67.3m — up +287% year-on-year and +67% year-over-year — it was a significant 28% beat vs. consensus.

Valuation and Upside

Sell-side brokers have been absolutely dummied by Beyond Meat with their target prices sitting $80-100/share lower than where stock trades today.

Grizzle has stood out from the beginning and gotten the call completely right, looking at a company with this level of growth on a 1-year target price view makes absolutely no sense. A current year 50x Price/Sales ratio is beyond meaningless when a company is growing 200-300% per year.

This is disruptive with sales growth 100x relative to the overall market, you value the company exactly as venture capital investors would — taking the long view.

At this juncture we believe our $1,100/share 2030 target price is too conservative (as our financial contemporaries over at Wall Street Bets can confirm), we’ll be updating our model in the coming weeks and revising higher based on the stronger revenue growth and profitability.

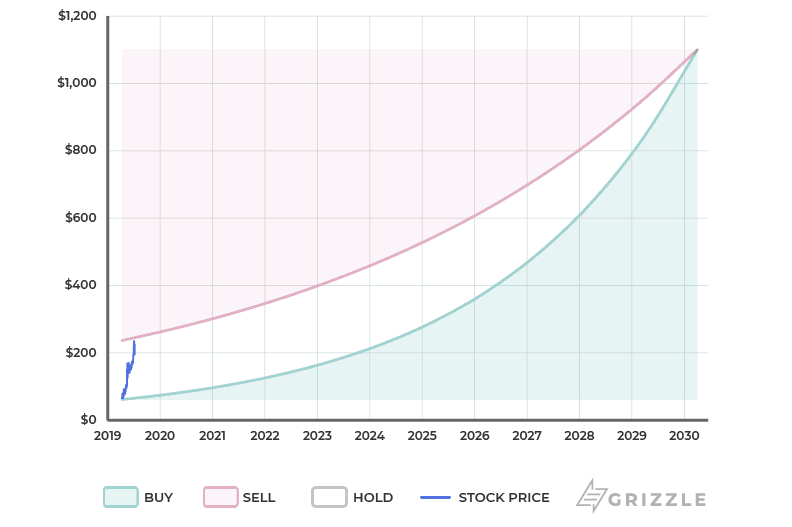

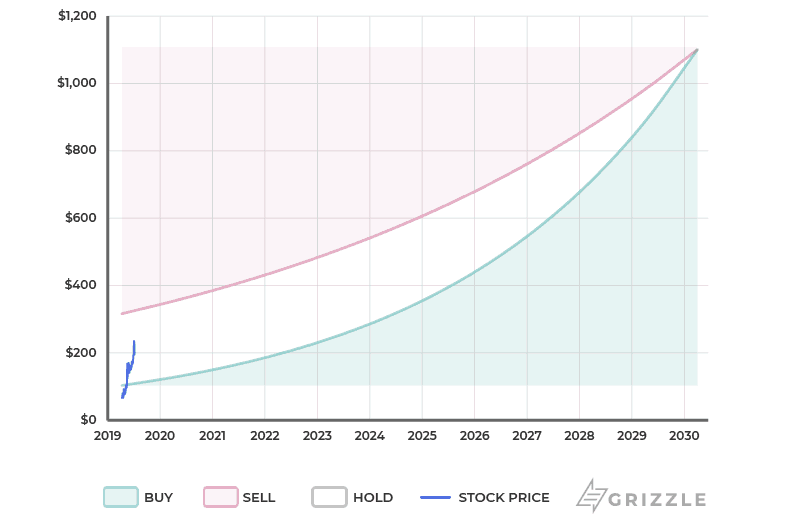

The following graph is the conceptual way investors should look at the near-term price target range vs long-term. We believe BYND is a clear buy if an investor can purchase the company at an implied 30% Internal Rate of Return (IRR) and conversely the investment proposition is challenged below 15% IRR. At the current share price of $195 — the implied IRR is 17% out to our 2030 long-term target of $1,100.

Target $1,100 – IRR Band of 15% (Sell) and 30% (Buy)

With the U.S. Federal Reserve about to embark on rate cuts, we believe investors could easily push the lower bound IRR to 12% — implying a top of the range near-term target of $316/share (FYI – this is exactly how quantitative easing works).

Target $1,100 – IRR Band of 12% (Sell) and 24% (Buy)

Earnings Review

Sales

As we’ve stated numerous time before, Beyond Meat represents nothing short of a consumer cultural phenomena akin to the iPhone. Top line revenue on any comparative basis (year-over-year, quarter-over-quarter, consensus) continues to absolutely crush everything in its way.

Beyond Meat Quarterly Revenue

Earlier this month Grizzle correctly highlighted how well Tim Hortons’ debut of the Beyond Meat breakfast sandwich was in their meal line-up, the shares rallied 40% higher thereafter.

$BYND short sellers have no idea how prolific Tim Horton's is in Canada, the breakfast #BeyondMeat sandwich didn't just do well, sales crushed it! 🚀

So well in fact they immediately launched $BYND burgers 🍔🍔$BYNDQ shorts are in for a world of pain: Q2 Earnings, July 29th 🔥 pic.twitter.com/210hBUG1R1

— Thomas George (@thomasg_grizzle) July 18, 2019

The Restaurant and Foodservice segment was the key driver of sales growth at +483% y/y, not entirely surprising to anyone closely following the fast food sector. The company now has distribution across 53,000 points of sale, this figure stood at 30,000 three months ago.

| Net Revenue (thousands) | Q2 2019 | Growth y/y |

| Retail | $34,120 | +192% |

| Restaurant & Foodservice | $33,131 | +483% |

| Total | $67,251 | +287% |

Source: Company Filings

Operations

CEO Ethan Brown stated on the conference call the company has the necessary capacity to meet the blistering growth in demand, adding new manufacturing lines and securing the required protein supply.

Beyond Meat delivered another outstanding quarter on the operational front, it’s clear this company is not only built for rapid growth but also delivering profitability.

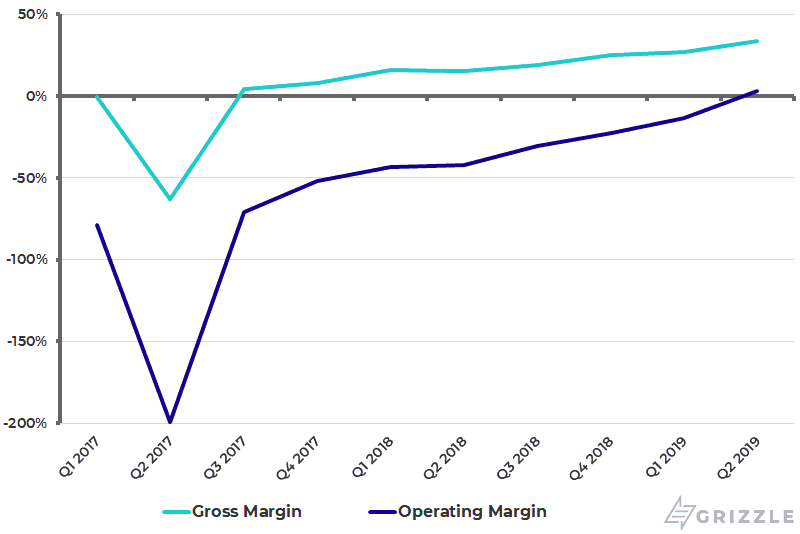

Gross profit increased 770% y/y to $22.7m, and gross margin continues to experience sequential quarter-on-quarter improvement from 27% in Q1 to 34% in Q2. Management is comfortable targeting a mid to high 30% margin longer-term.

The biggest pivot on the quarter was operational income. Beyond Meat flipped positive on adjusted EBITDA for the quarter at $6.9mm vs a loss of $5.6mm from the previous year. Sell-side consensus had an expected EBITDA loss of -$441k, so a very big beat on the operational front.

Beyond Meat – Gross Margin and Operating Margin

CFO Mark Nelson outlined the following key levers for gross profit improvement on a go forward basis: volume leverage, internalization of manufacturing, packing cost reductions, tolling fee efficiencies, and better supply chain logistics.

Headline Earnings per Share (EPS) came in at -$0.24/share which was significantly lower than analyst consensus of -$0.08/share. However net income was impacted by a one time non-cash expense related to the re-measurement of warrant liability (related to the IPO). On this adjusted basis EPS stood at positive $0.05/share — a beat vs consensus.

Outlook

The company continues to guide to Q2 and Q3 being the strongest quarters for revenue and profit contribution. Given the strong results YTD the company increased their 2019 revenue guidance from $210mm to $240mm.

Additionally, the company is now guiding to positive EBITDA for the full year vs their previous guidance of break-even.

It’s important to note that Tim Hortons’ new Beyond Meat Burger and Dunkin’s Breakfast Sausage aren’t included in full year guidance — so we’ll likely continue to see management take the top end of guidance higher as the year progresses.

This is a company that is executing on all cylinders and is on target with branding and consumer tastes. Grizzle continues to view this as one of the most powerful secular growth opportunities in public capital markets. Portfolio Managers are starved for growth in their portfolios — this is a clear winner on multiple fronts.

VC & Insiders Selling Shares in Stock Offering

Shortly after the earnings release, Beyond Meat announced a share offering of 3 million shares comprised of primarily pre-IPO investors selling — with only 250,000 shares being issued by the company.

Venture Capital firms Kleiner Perkins and Obvious Ventures are the large blocks that are selling (9% of their shares each). CEO Ethan Brown is selling 3%, while the CFO and CGO are selling 14% and 11% respectively. These aren’t earth shattering figures and allows a level of liquidity gained for early investors and management.

Obviously this share offering has taken some wind out of the supercharged stock, however we believe it dampens the impact of the coming share unlock in October.

| Entity | Total Shares | Shares Offered | % Selling |

| Kleiner Perkins | 7,751,463 | 704,496 | 9% |

| Obvious Ventures | 4,462,542 | 405,580 | 9% |

| Ethan Brown (CEO) | 1,604,027 | 45,000 | 3% |

| Mark Nelson (CFO) | 464,850 | 64,562 | 14% |

| Chuck Muth (CGO) | 218,765 | 24,616 | 11% |

| Gregory Bohlen (Director) | 797,224 | 72,456 | 9% |

Source: Company Filings

What About the Shorts?

Short sellers are deeply in the red on Beyond Meat. They continue to endure and take their lumps as short interest are remained steady in the 40-45% range with borrow rates in excess of 100%. Ihor Dusaniwsky is always on point with the short interest play-by-play.

$BYND short int is $1.21 bn; 5.14 mm shs shorted; 43.88% of float; 135.87% borrow fee & 150% on new borrows. Shs shorted declined by -283k last week as recalls and mark-to-market losses mount. Shorts are down -$155 mm,-13.81%, for the week, including up $82 mm today. pic.twitter.com/8U0yEaJitA

— Ihor Dusaniwsky🇺🇦 (@ihors3) July 29, 2019

In the interest of full disclosure, employees of Grizzle personally purchased and currently own stock in Beyond Meat. See the Content Disclosure section on our Terms and Conditions page for more details.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.