Bottom Line: Beyond is the Benchmark for Faux Meat

Beyond Meat (NASDAQ: BYND) smashed Wall Street quarterly estimates once again, establishing themselves firmly as the titan of faux meat. However, the stock was down 10% after-market as investors scale back their risk appetite (coronavirus) — investors likely wanted a larger margin of safety for guidance in 2020.

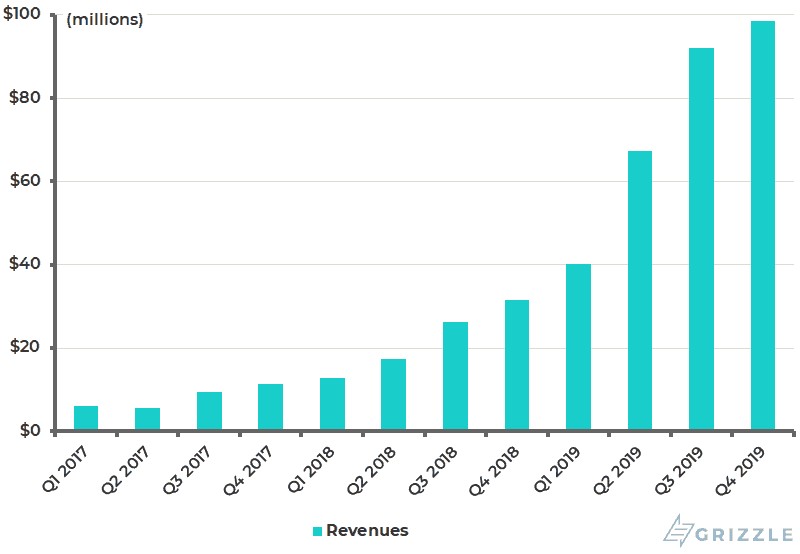

For Q4 2019 the company beat on revenue by +21% ($98.5 million) and EBITDA by +55% ($9.5 million). The beats are impressive as this is seasonally their weakest quarter.

| Q4 2019 Estimate | Q4 2019 Actual | % Beat | |

| Revenue | $81.5 million | $98.5 million | +21% |

| EBITDA | $6.1 million | $9.5 million | +55% |

| EPS | $0.00 | $-0.01 |

Full year results highlight the high torque growth driving the company, a company that is growing top line by 239% year over year in 2019. Impressively during the period Beyond grew manufacturing capacity by 2x comparing Q4 2019 vs. Q4 2018.

| FY 2018 | FY 2019 | % Growth | |

| Revenue | $87.9 million | $297.9 million | 239% |

| EBITDA | $-19.3 million | $25.3 million |

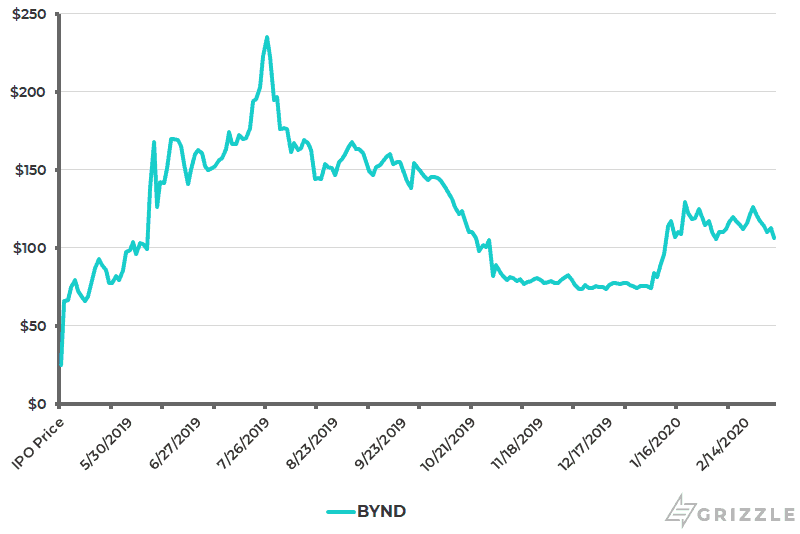

The stock had staged a significant recovery from the lows in November/December ($75-80/share range) to a recent January peak of $129/share. The coronavirus market overhang ultimately dragged Beyond down with the rest of the market by the end of February.

We continue to believe that Beyond Meat is one the best growth stocks in the entire market on a 5-10 year view. It’s meaningless to bemoan a high current year price-to-sales ratio for a company that is growing 100-200% yearly.

The big caveat for all growth stocks is the coronavirus, there is literally zero appetite for risk in the market. We continue to own a core long-term position in BYND and will look to strategically add options and shares once this risk cloud passes.

Outlook

Beyond provided 2020 guidance that was in-line with the Street expectations on revenue, however, EBITDA margin guidance was 180bps light versus consensus.

With respect to the in-line guidance on the top line, CEO Ethan Brown stated on the conference call that it only includes established ongoing partnerships. The outlook doesn’t include prospective new business through the course of the year, such as a full roll-out of McDonalds or expansion into China. The pipeline is very deep, we’re comfortable that Beyond will continue to upsize this outlook through the year.

Since the IPO, Beyond Meat management has consistently been conservative on revenue guidance, in June of 2019 their full year outlook was $210 million of annual revenue — actual revenue came in 42% higher by year-end ($298 million). We expect a similar dynamic to play out for full year 2020.

Regarding the muted margin guidance, Brown stated that the company will significantly ramp up marketing spend to combat meat industry funded misinformation PR campaigns. Frankly this is the cost of disruption and we believe it’ll provide long-term brand ROI.

| 2020 Consensus | 2020 Company Outlook | Difference | |

| Revenue | $498 million | $490-$510 million | in-line |

| EBITDA Margin | 10.3% | 8.5% | -1.8% |

The company remains focused on the goal of delivering price parity by 2024 in 1 SKU. Brown stated that a combination of lower commodity input pricing, labour, and distribution optimization would be the key levers to deliver on this goal. This is the holy grail for alternative meat, price in-line or better than existing animal based protein.

Beyond currently has manufacturing capacity for gross revenue of $700 million, by year end the company will have scaled this to $1 billion (+42%). Capex outlay for the year is expected to be in the range of $40 million, double that of 2019.

Operations

Beyond is firmly #1 in alternative meat, they only have 6 product SKUs and 4 of them are the the best selling in the entire category, outperforming their nearest competitor (Impossible) by a factor of 2. They are the 800-pound incumbent guerrilla.

Beyond’s strategic food service partnerships continue to explode with Starbucks announcing a national launch in Canada, McDonald’s Canada test expansion, Dunkin Donuts national launch, Carls Jr expanded offering and Subway Canada expansion.

Q4 Revenues grew 212% year-over-year, driven by volume increases in the retail and restaurant channel. Of the 650K food service outlets in the U.S., Beyond is in less that 4% of them — there is still plenty of opportunity to increase penetration in this important channel.

Beyond Meat Quarterly Revenue

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.