Beyond Meat (NASDAQ: BYND) announced earnings results for Q1 2020 today that were ahead of analyst estimates. We broke down the stellar results and the structural upside in the stock on GRIZZLE live:

https://youtu.be/y5vPDBiM8WY?t=1122

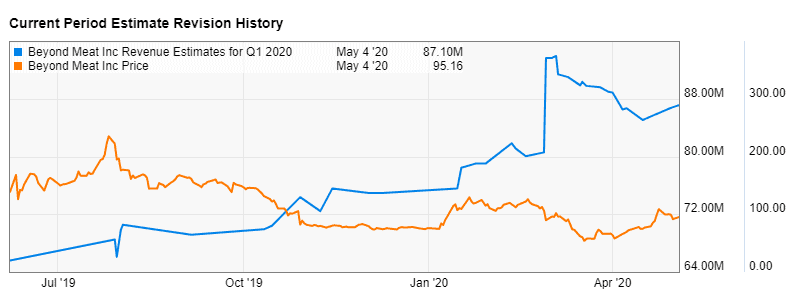

Revenue came in at $97.1 million, which beat analysts’ estimates of $87.1 million (+11% vs consensus).

EPS came in at $0.03/share, which beat analyst average estimates of $-0.08/share.

EBITDA came in at $12.7 million, significantly beating analyst estimates of $1.2 million (+958% vs consensus).

Analyst Q1 2020 revenue estimates had increased by 16% since the beginning of the year, Beyond beat those elevated estimates by a strong margin.

The company’s food-at-home demand channel has benefited as a result of the coronavirus pandemic.

CEO Ethan Brown noted in the conference call that the uptick in food-at-home wasn’t enough to offset the reduction in US Foodservice business over the near term. He noted that the US Foodservice division fell -25% month-over-month March vs. February.

Due to the uncertainty related to COVID-19 the company stated that it is suspending it’s previously announced 2020 Outlook. The company continues to be very conservative with respect to guidance, they have beat analyst top and bottom line estimates every quarter since going public.

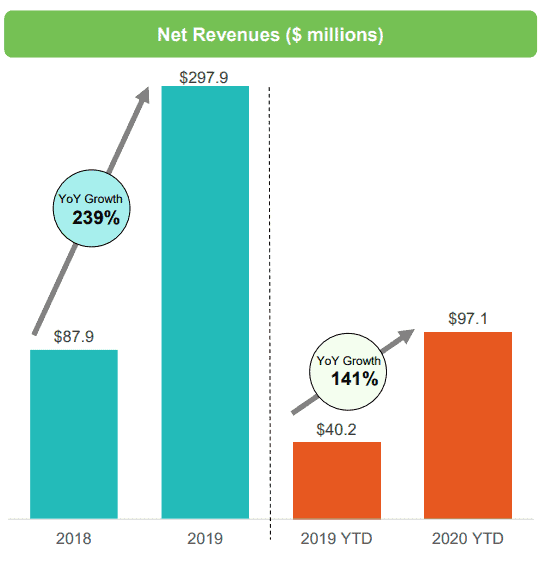

The company grew net revenue by 141% year on year, with strong robust growth in each of it’s divisions: U.S. Retail $49.9 million (+157% y/y); Foodservice $22.6 million (+156% y/y) and International Foodservice $18 million (+106% y/y).

Adjusted EBITDA (operating income) came in at $12.7 million and associated margin of 13% – an margin uplift of +1,840 bps versus Q2 2019 (-5.3% EBITDA margin).

The CFO noted on the conference call that Costs-per-goods-sold (COGS)/pound was the lowest in the history of the company.

Outlook

The company continues to execute on it’s business model at a rate that is significantly ahead of market estimates.

We believe the company is well positioned to capture market share relative to animal protein. In 2020 we’ve seen a significant disruption in the meat processing supply chain which presents Beyond an excellent opportunity to accelerate public brand awareness.

We continue to believe that Beyond Meat is one the best growth stocks in the entire market on a 5-10 year view. It’s meaningless to bemoan a high current year price-to-sales ratio for a company that is growing 100-200% yearly.

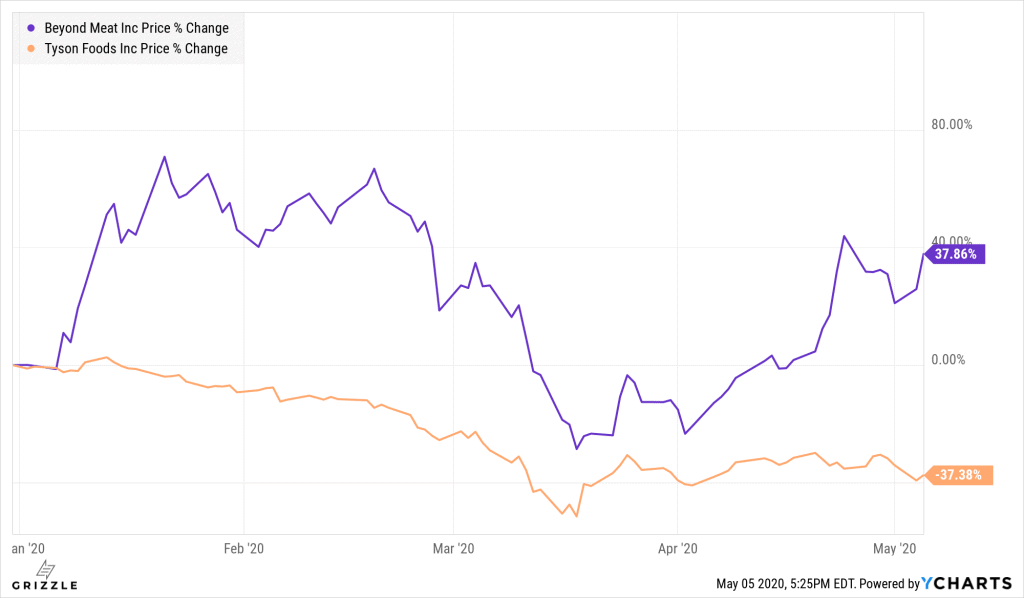

The long-term structural trade is going long plant-based protein and going short factory process meat. Beyond Meat has outperformed Tyson Foods by 75% year-to-date.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.