The investment wisdom has it that the middle ground is always the sensible approach in politics. This can be seen, for example, in a series of articles triggered by the U.S. Democratic presidential candidates’ recent efforts to paint themselves as socialists.

Most of these articles make the point that it is possible to have capitalism in the context of modern welfare states. See, for example, an article by former Federal Reserve vice chairman Alan Blinder in a recent Wall Street Journal (“Democrats, stop pretending to be socialists”, March 15, 2019 [paywall]). The article concluded: “It isn’t hard to smooth the sharpest edges from unfettered capitalism – with social insurance, progressive taxation, a social safety net and the like – without destroying the vibrancy and magic of capitalism. It works.”

This may be the case, but I have significant reservations in the sense that income tax levied above a certain percentage of income massively distorts the incentives created by capitalism. It is also the case that “capitalism” has long ceased being practiced in the banking sector with the distortions provided by taxpayer-funded bailouts and regulatory imposed “risk-based” capital adequacy models where government bonds are treated as zero risk weighted. This is why the Democrat left and the Republican free market right were correct when they both called for nationalization of the U.S. banks that required taxpayer bailouts during the 2008 crisis.

But the point this week is not to dwell on history. Rather, it is to observe that the Democrat left and the free market Republican right are both converging on the same view as regards the long-overdue regulation of “Big Tech”.

Move Fast and Break Things

One and a half years ago, I read an excellent book that highlighted both the insidious “echo chamber” dynamic of social media as well as Big Tech’s commercial exploitation of individual data and its successful capture of Washington during the Obama administration via aggressive lobbying. The author of that book (Move Fast and Break Things, Little, Brown and Company, April 18, 2017), Jonathan Taplin, has an interesting background as both a music producer and an investment banker.

The arguments in that book have since become much more widely accepted, though it should be conceded that baby boomers like Taplin seem much more concerned about the privacy issue than millennials. I was reminded of all this reading now that Democratic presidential candidate, Senator Elizabeth Warren, has publicly called for a break up of “Big Tech” on the antitrust angle and also called for an unwinding of acquisitions where “Big Tech” has successfully identified potential threats to its winner-take-all models and purchased them. The most obvious examples here are Facebook‘s acquisitions of Instagram in 2012 for US$1 billion and of WhatsApp in 2014 for US$19 billion.

I have to admit to not sharing Senator Warren’s views on most economic issues. But there is complete agreement on “Big Tech”, and from a more Republican right-wing perspective it has also been interesting to see Republican Senator Ted Cruz making approving comments of Warren’s proposals.

The policies she is proposing are almost exactly what is proposed in Taplin’s book or a more recent book that looked at Facebook (Zucked: Waking Up to the Facebook Catastrophe, Penguin Press, Feb. 5, 2019) by Roger McNamee who, interestingly, was an initial investor in Facebook. And Facebook and Google are the main companies in the immediate line of fire with Amazon and Apple, in that order, falling not so far behind.

The Warren call is also topical at a time when Facebook is seeking to start monetizing Instagram and WhatsApp, and when Mark Zuckerberg has put on record that he is fundamentally aiming to shift Facebook’s core strategy from the advertising-driven “public sharing” model to an encrypted system based on privacy where only people sending and receiving messages will be able to see them.

This is probably a smart decision if Facebook wants to survive, and also complements the recent news reports of Facebook’s plan to develop a digital currency. Thus, Facebook is reportedly planning to roll out a cryptocurrency over the next year that will allow users to send money to their WhatsApp contacts across international borders (see New York Times article: “Facebook and Telegram are hoping to succeed where Bitcoin failed”, Feb. 28, 2019).

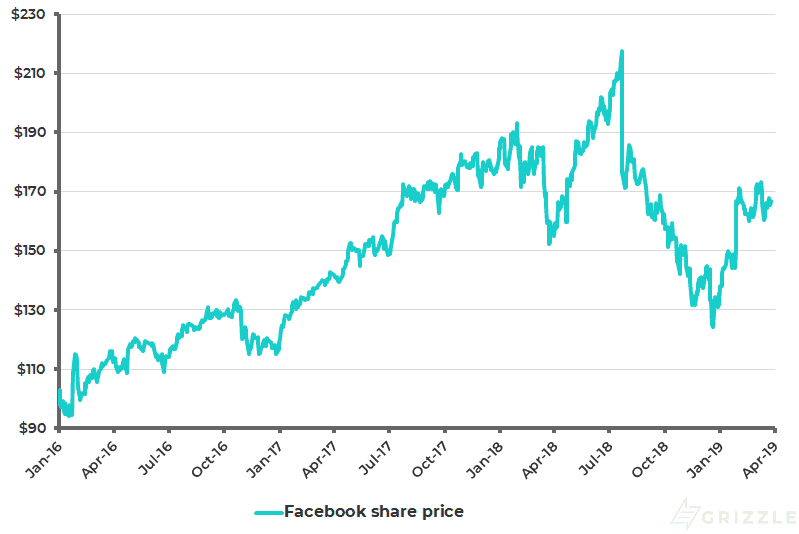

Facebook Share Price

The Future of Facebook

Meanwhile, if Zuckerberg does not succeed in implementing the change, the likelihood is that the current model will hit a brick wall, either because Facebook becomes even more “uncool” than it already is or because it is heavily regulated or, perhaps most likely, a combination of both. Meanwhile, the disruption of traditional media by the grotesque “news feeds” has long been obvious.

It remains amazing to me why major media ever allowed “Big Tech” to display their content free of charge. But for a long time the Big Tech companies were able to have the best of both worlds by claiming they were not media companies but only utilities. That is no longer the case. The editorial obligation of social media to try and monitor what is on their platform means soaring costs as they try to perform an editing function in terms of which they have no competence. Meanwhile, the latest outcome of the insidious feedback loop, encouraged by the obnoxious “algos”, was a Facebook 17 minutes live stream of a gunman attacking worshippers in two mosques in, of all places, New Zealand.

Still, Zuckerberg is obviously very smart, and presumably understanding the old model has passed its “sell-by” date, he is clearly switching direction. Maybe he can pull it off.

The views expressed in Chris Wood’s column on Grizzle reflect Chris Wood’s personal opinion only, and they have not been reviewed or endorsed by Jefferies. The information in the column has not been reviewed or verified by Jefferies. None of Jefferies, its affiliates or employees, directors or officers shall have any liability whatsoever in connection with the content published on this website.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.