We’re introducing a new feature this week where we will start with a quantitative screen and dig a little deeper over a couple of weeks into the investment thesis around the companies that pass the screen.

My quant stock screen for the week is in the software sector (using @ycharts).

My fundamental screen criteria:

Free Cash Flow Yield: >2%

Revenue Growth: >10%

Return on Equity: >15%

Market Cap: >$250MA real decent list of names:$EEFT $VMW $CDNS $MSFT $INTU $ADBE $FICO pic.twitter.com/UWGF7ECeWf

— Thomas George (@thomasg_grizzle) November 19, 2019

We’ll start by taking a look at the overall businesses these companies are in and where their growth is coming from.

| Primary Businesses | Primary Sources of Growth | |

| EEFT | ATMs, POS terminals, electronic payments and credit/debit card services | ATMs and POS |

| VMW | Enterprise software and services for cloud applications, networking, security and digital workspaces | Evenly split between licenses and services; also evenly split U.S. vs International |

| CDNS | Electronics, circuit and chip design software | Design IP segment |

| MSFT | Personal and enterprise software, hardware and cloud hosting | Commercial Windows and Office products/services and Azure cloud solutions |

| INTU | Tax and finance software, services and loans | QuickBooks and TurboTax online ecosystem |

| ADBE | Digital media software and digital experience (marketing/analytics) platform | Digital experience platform |

| FICO | Credit worthiness scoring and data/analytics | B2B credit scoring solutions and services |

Bottom Line: While we think the fintech aspects of both Euronet and FICO are interesting, those aren’t the primary sources of growth for either of those two companies and they are going to be facing ever increasing competition as finance continues to move digital. Microsoft keeps crushing it in growth and results quarter after quarter and their transformation to the cloud has been nothing short of miraculous, but we wonder whether or not they’ve been fully valued as an investment given they now sit at a $1.1T market cap. Grizzle has been an ardent bull of Adobe, with a market dominant position in a growing field, while we continue to believe it’s a good investment we’d rather take a deeper look at some of the names that haven’t been on our radar.

Next week we’ll dive deeper into VMWare, Cadence and Inuit… stay tuned!

Oracle vs Google is an $8B Supreme Court Hearing that could Turn Tech Copyright on its Head

Bottom Line: A legal battle between Oracle (NYSE: ORCL) and Alphabet’s Google (NASDAQ: GOOG) which has been ongoing for over 6 years will be heard by the Supreme Court. At issue is Google’s use of Java application programming interfaces (APIs) which are owned by Oracle in the Android mobile operating system. Oracle claims that they should be compensated for Google’s use of the APIs as Android was a ‘competing platform’, while Google claims the interfaces are critical to allow developers to create cross-platform applications. Oracle is seeking over $8B of the $42B which Android generated for Google between 2007 and 2016. If Oracle is successful it could have an impact on software development costs for the industry as APIs are widely used and relied upon in many applications.

Paypal Adding in Price Discovery to go along with Payments with it’s Honey Acquisition

Bottom Line: Paypal (NASDAQ: PYPL) announced that it has agreed to acquire Honey Science Corporation for $4 billion. Honey, which makes a deal-finding browser add-on and mobile app, currently has 17 million monthly users. Honey users are able to track prices and promo codes, browse offers and participate in a rewards program and currently works across 30,000 merchant websites. The move gives Paypal a broader piece of the e-commerce market as access to Honey’s users will let Paypal interact with them earlier in the buying process rather than just at checkout phase. Also, Paypal’s many merchant partners will be able to benefit by offering targeted promotions to consumers. Honey reportedly had over $100 million in revenue last year and was profitable on a net income basis — a very rare quality indeed these days. With such a high valuation, early investors in the company will have a big payday given that the company had previously only raised $49 million in funding.

Do Microsoft’s 20m Teams Users Really Matter More than Slack’s 13M?

Bottom Line: Numbers matter, but the context of those numbers is also very important. In sheer numbers, Microsoft (NASDAQ: MSFT) is beating Slack (NYSE: WORK), with the company recently reporting that it has 20 million daily active users compared to Slack’s 13 million (last reported in October). Microsoft’s showed impressive growth of over 50% from its last reported count of 13 million daily team users in July. The news hit Slack’s stock hard as it was down as much as 10% the day of Microsoft’s announcement. But the context of the numbers is that Microsoft counts a user as someone who starts a chat, places a call, shares a file, edits a document or participates in a meeting using Teams. Given that Teams is bundled in with Office 365 subscriptions and tightly integrated with Word, Excel, Powerpoint and Outlook, we would hazard to guess that many of those users are getting counted through the editing documents/participating in meetings categories. Those integrated functions are convenient in large organizations but they aren’t the kind of sticky functionality that engages users to stick with a platform in our opinion. Slack thrives on its stickiness given its multitude of integrations and streamlined design so we wouldn’t count them out yet. As a commenter from Twitter pointed out, just cause you have bigger numbers doesn’t mean you’ll always have the winning platform in the end.

Reminds me of Google+ and Twitter back in the day https://t.co/ZUFTUrouHB pic.twitter.com/aPElVK73PU

— Carolyn Penner (@cpen) November 19, 2019

The Growing Esports Ecosystem

Bottom Line: The competitive gaming or esports industry is starting to ramp up. While gaming tournaments and events have been drawing the interest and eyeballs of fans for a few years now, interest from venture capital is starting to pump even more money into the industry. Game publishers are likely to be the biggest winners in the industry as their franchises and games gain attention, fans, and ultimately, players. But there is a whole set of technology around the ecosystem that is ripe for monetization of events which is still in its early days.

Ford is Betting on an Electric Future with one of its Biggest Brands

Bottom Line: With the unveiling of the Mustang Mach-E, Ford (NYSE: F) has radically departed from the storied Mustang brand’s roots. The new Mach-E, a four-door all electric utility vehicle is a stark contrast to the classic Mustang image of a two-door sports coupe that Ford has been producing since 1964. While electric vehicles (EVs) have yet to penetrate the American market deeply, representing less than 1% of the vehicles on the road, Ford expects EV sales to grow to over 1.5 million/year in the U.S. by 2025. Betting one of your biggest brands on those projections is a big risk, one that even earned the congratulations of another famous risk-taker betting that the future of cars will be electric.

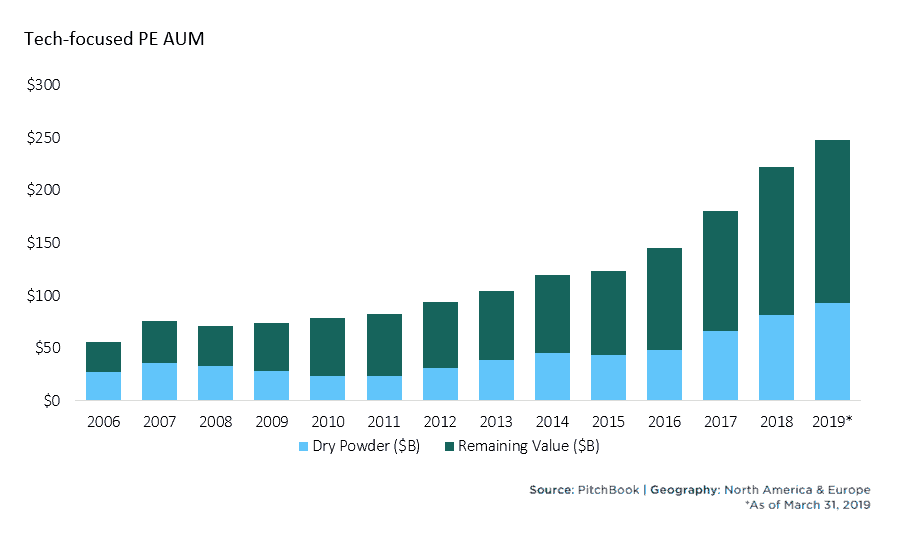

Tech Investing Chart of the Week

We’ve all seen how the huge sums of money and soaring valuations that Venture Capital has been pumping into tech startups have been treated by the public markets… ahem WeWork, Uber, Lyft, etc. But Private Equity markets haven’t been immune to the spending spree going on in tech either.

TOP TECH STOCKS NEWS

- After New Guidance, Will Sonos Tread Water or Break Out?

- Splunk (SPLK) Stock Rises After Hours Following Strong Q3 Revenue Beat

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.