The contrast between the US and China monetary cycles has become crystal clear in recent weeks.

has announced its most significant rate cut since April 2020 while Federal Reserve governors and US economists compete to sound more hawkish as the realisation has dawned how far behind the curve the Fed appears to be.

US money markets are now predicting five rate hikes in 2022.

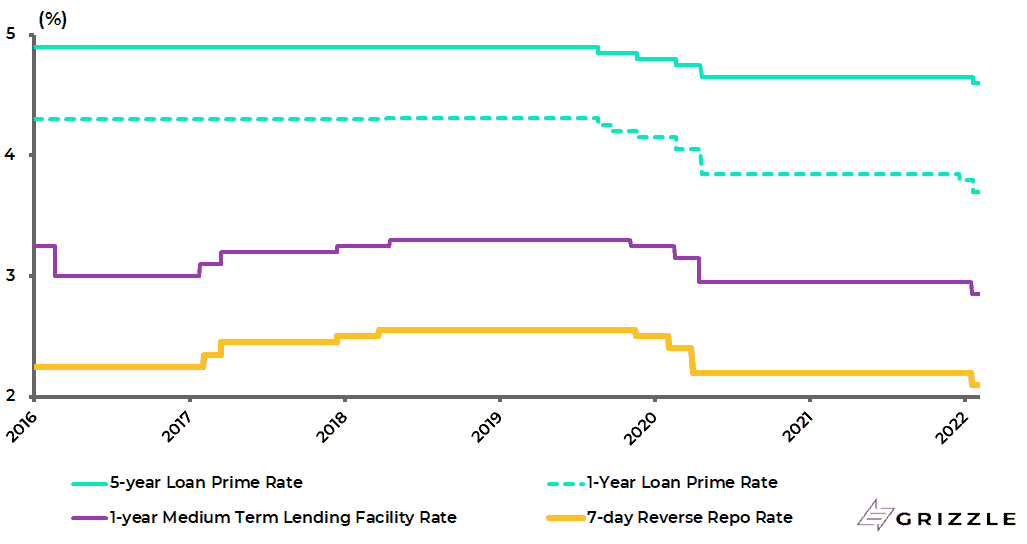

On China, the People’s Bank of China (PBOC) on 17 January cut the one-year medium-term lending facility (MLF) rate and the seven-day reverse repurchase rate by 10bp each to 2.85% and 2.1%, respectively.

The Chinese central bank on 20 February also cut the one-year and five-year loan prime rates by 10bp and 5bp to 3.7% and 4.6%.

China PBOC key interest rates

The rate cuts followed the release of another series of weak Chinese data as a result of the damage done to the economy by the Covid suppression policy.

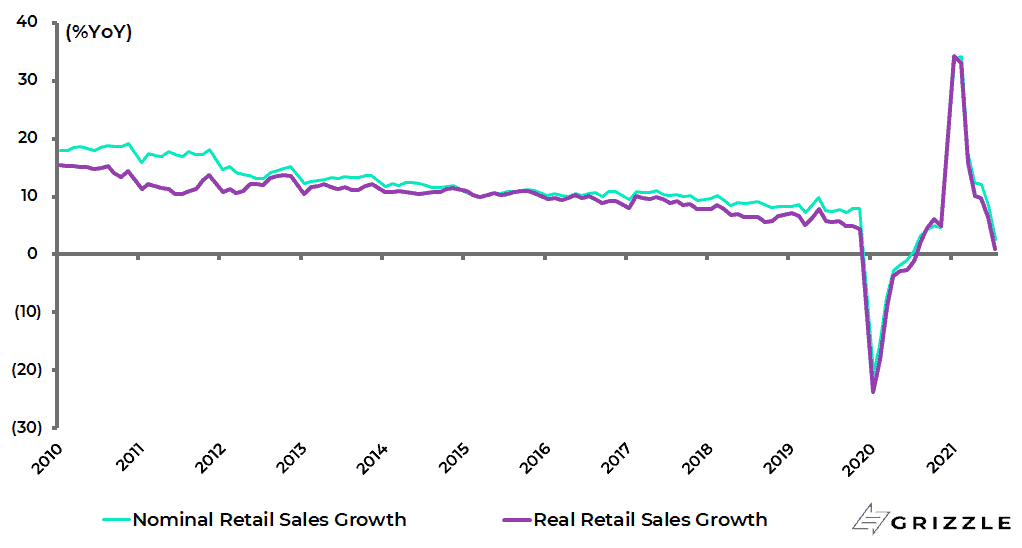

Retail sales, for example, rose by only 1.7% YoY in December.

China retail sales growth

A key issue for China in coming months is whether the Covid suppression policy will be relaxed to adjust for the practical realities of Omicron variant given how infectious it is.

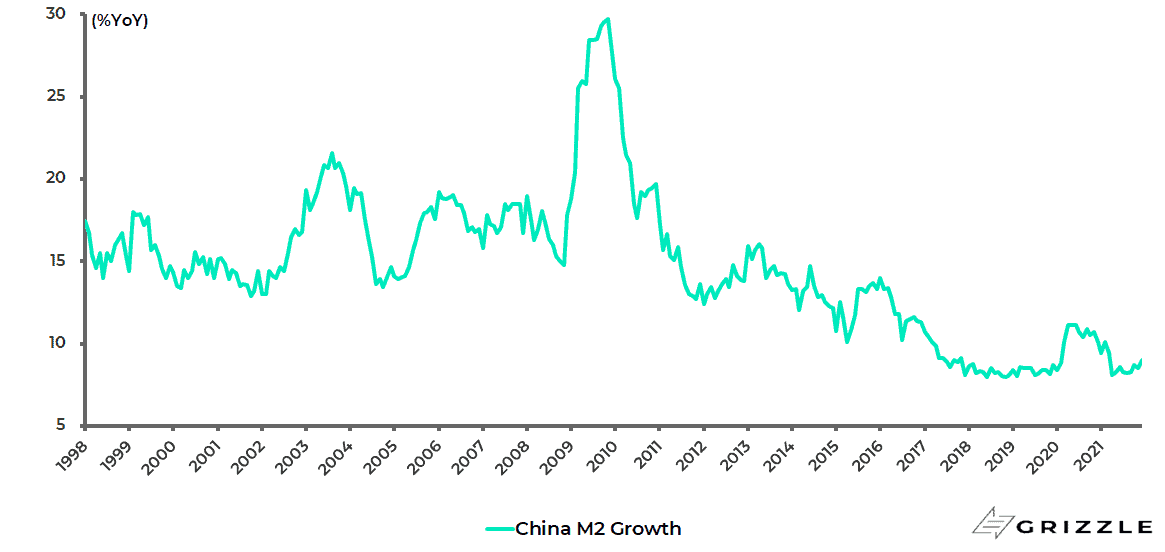

Meanwhile, it is worth recording that China M2 growth picked up in December while credit growth should turn up in the present quarter as credit quota are allocated.

China M2 growth

The other issue is whether the PBOC will relax the requirement to keep credit growth in line with nominal GDP growth, which has been the focus of the deleveraging policy in recent years.

Quantitative Tightening is the X-Factor to Watch

But it is in America where the prime market focus remains.

While a far more hawkish Fed is fast being discounted in terms of rate hikes, there is room for more damage to be done to the profitless tech thematic if the Fed moves sooner and more forcefully than previously expected on the quantitative tightening issue.

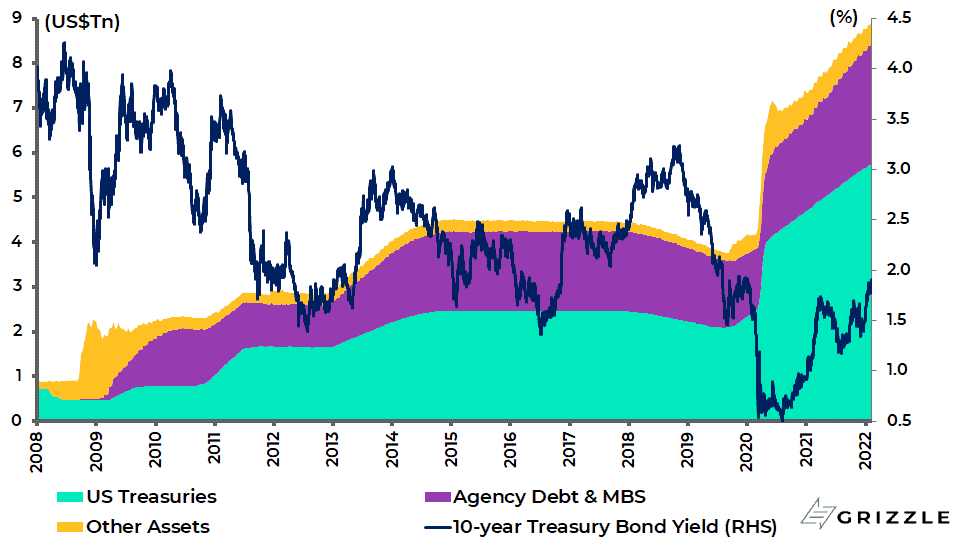

In this respect, the Fed balance sheet, which should total US$8.95tn by the end of March, has now become a prime focus for markets.

This is because quanto tightening is a much blunter tool than rate hikes.

There is also a lack of precedents.

The only significant attempt to shrink the balance sheet in the modern era occurred between October 2017 and September 2019 when, first, Janet Yellen and Jerome Powell from February 2018, sought to normalise monetary policy by reducing the balance sheet by US$710bn or 16% from US$4.47tn to US$3.76tn. (There was also a brief period of quanto tightening in 2012 when the balance sheet was reduced by 4.5% to US$2.8tn.)

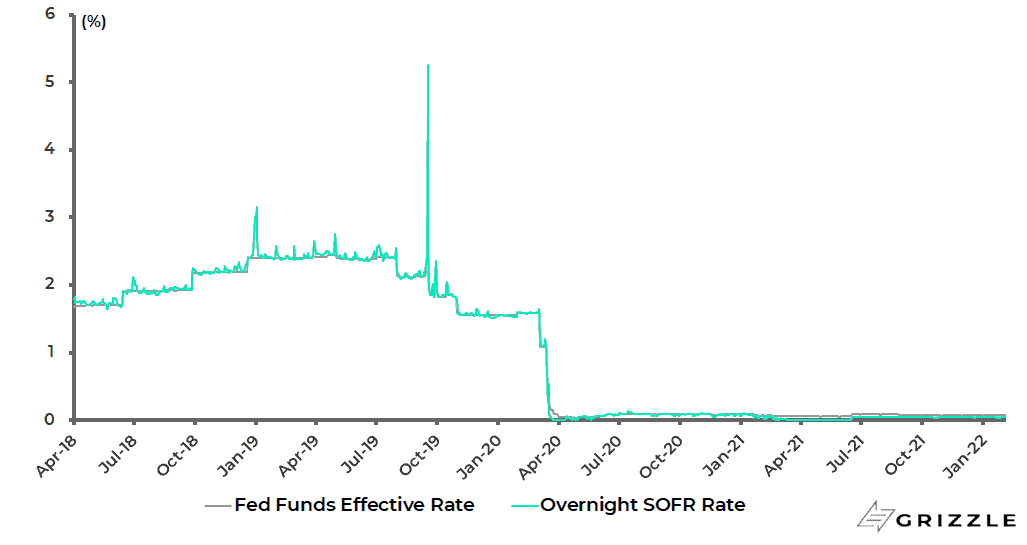

The experiment under Powell ended with a surge in rates in the repo market in September 2019.

Fed funds effective rate and secured overnight financing rate (SOFR)

This previous experience will make investors naturally nervous about the impact of quanto tightening, with the analogy that of a mainlining addict being deprived of his daily fix.

Before the Jekyll and Hyde act staged by the Fed in the past two months, this writer would have assumed, as would have the vast majority of investors, that the Powell Fed would be in no hurry to start contracting the balance sheet after ending quanto easing and would let rate hikes do the tightening work to begin with.

But it has become clear of late that there are those on the Fed who want to move sooner, though Powell left the timing of the commencement of balance sheet contraction open in his testimony on 11 January.

Still, there is no doubt that investor focus on the balance sheet issue is rising, as a result of recent Fed chatter.

One example is a remark by Atlanta Fed president Raphael Bostic in an interview with Reuters last month that the Fed should reduce the size of the balance sheet by at least US$100bn a month, with the aim to reduce it by at least US$1.5tn (see Reuters article: “Fed’s Bostic says three hikes, fast balance sheet runoff needed for inflation fight”, 11 January 2022).

Certainly, such a policy of balance sheet contraction, when assets are sold beyond the natural “running off” of maturing securities, would be way more aggressive than previous expectations.

Such a policy would also in the first instance likely put more upward pressure on long-term Treasury bond yields.

This is because the market will sell Treasuries because the process of balance sheet contraction implies the Fed selling some of its Treasury bond holdings or at least not reinvesting them as they mature.

Still, this is only the initial reaction.

When it Comes to QE and Bond Returns, Think in Reverse

The history of the quanto easing era shows that, contrary to the views maintained by central banks and most conventional economists, quantitative easing ends up in practice being bearish for long-term Treasury bonds while, conversely, quantitative tightening is bullish.

This is because the former is an effective form of monetary easing and the latter is perhaps an even more effective form of monetary tightening.

The above counterintuitive dynamic is clear from the chart below of the relationship between Treasury bond yields and the Fed balance sheet during the quanto easing era.

Federal Reserve balance sheet and US 10-year Treasury bond yield

So if the Fed really does embark on the sort of quantitative tightening programme now beginning to be talked about, and that remains a big if, this writer may have to review the current recommendation maintained here since the end of March 2020, namely that investors should sell all Treasury bonds as well as all G7 government bonds.

But in the meantime, there will be continuing political pressure on the Fed to be seen to be doing something about inflation in the run-up to the November mid-term elections.

In this respect, it is a very long time since there has been political pressure in America on the Fed to tighten.

Also, with the base effect on inflation not due to kick in positively until the March CPI report, which will not be released until 12 April, there is plenty of scope for markets to worry more about tightening in the next few months even if the eventual outcome ends up being nothing like as dramatic as markets have started discounting, in terms of both the number of rate hikes and the scale of balance sheet contraction.

Inflation is Real This Time

There is another point.

This is the first monetary tightening cycle since at least the early 1990s when the Fed is tightening because it is perceived to be way behind the curve in terms of managing inflation.

And there is no doubt that the Fed is massively behind the curve in terms of the 7% CPI inflation print in December and its own 2% target.

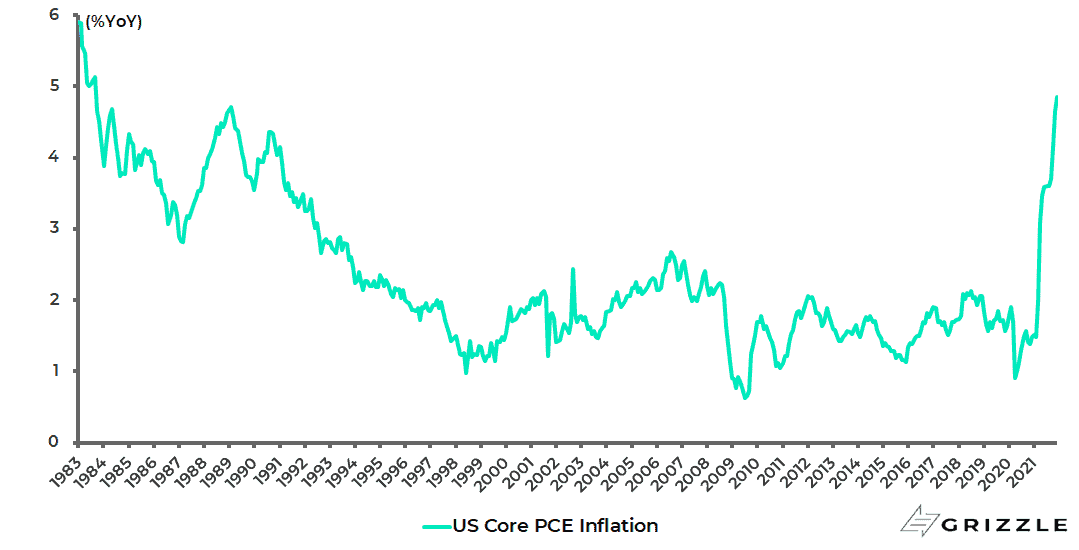

It is even 2.9 percentage points above its target on its favoured core PCE inflation, which was running at 4.9% YoY in December, the highest level since September 1983.

US core PCE inflation

Source: US Bureau of Economic Analysis

The views expressed in Chris Wood’s column on Grizzle reflect Chris Wood’s personal opinion only, and they have not been reviewed or endorsed by Jefferies. The information in the column has not been reviewed or verified by Jefferies. None of Jefferies, its affiliates or employees, directors or officers shall have any liability whatsoever in connection with the content published on this website.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.