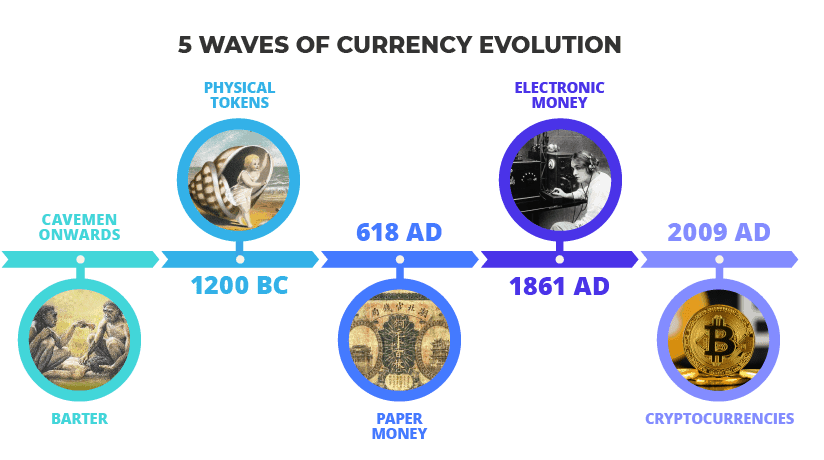

The advent of cryptocurrencies marks the fifth distinct phase in the evolution of money/value exchange. These transitions don’t happen frequently, suggesting all the hype around crypto has a degree of merit. This infographic tracks the history of money to where we are today.

We take a look at each phase and answer the most critical question, what problem the new form of money solved — the more profound the fix, the greater the adoption. Bottom-line, crypto has to be as game changing as moving from cash to credit card to truly be worthy of ushering in a new chapter of value exchange.

Barter

PROBLEM IT SOLVED – Allowed humans to specialize and acquire goods they didn’t have.

The classic scenario that pairs ideal trading partners: Caveman ‘A’ (great at making wheels, not so good at hunting) with Caveman ‘B’ (great hunter, still using a square tire). The downside of the system is that Caveman ‘A’ may have to wait a long time before finding the perfect match.

There’s significant debate whether the barter system was ever the starting point of value exchange. In a 1985 paper, Cambridge anthropology professor Caroline Humphrey stated it was an imaginary construct by Adam Smith (The Wealth of Nations). “No example of the barter economy, pure and simple, has ever been described, all available ethnography suggests that there has never been such a thing”. In her view the anthropological evidence points to the ‘gift economy’ as the origin of value exchange. If you needed something, you simply asked for it.

Barter in the 21st Century

The hipster-tech movement has brought bartering to the digital-age, sites like swapstyle and bunz have tried to create a better barter user experience (heroic task at best).

The informal amphetamine-fuelled ‘stolen goods’ exchange economy is perhaps the best functioning example of the barter system at work. However, swapping stuff with someone on flakka downright sucks, sweet as pie when you chat on the phone, deranged zombie when you meet.

Physical Tokens

PROBLEM IT SOLVED – Tokens facilitated easier trade of goods and also put a specific monetary value of the good provided.

Whether it’s coins, beads, shells, feathers or gold, the idea was to bestow ‘special worth’ to an inanimate object. Once the entire village agrees that a black swan’s feather is ‘worth’ something, the physical token economy begins. Physical tokens broke important barriers to trade. People’s wants don’t always align perfectly for one-on-one trade. Again, this only works when everyone agrees that a black swan’s feather is ‘special’….

Paper Money

PROBLEM IT SOLVED – Allowed societies to move away from the rigid construct of assigning value to inanimate objects (coins), and designating special worth to pieces of paper that could be more readily produced.

The earliest use cases for paper money were during the Tang Dynasty in China (618-907); pieces of paper were used as a form of credit or IOUs, additionally due to the lack of metallic currency, paper notes replaced coins as burial money.

Paper Money and the Gold Standard

The gold standard was a system adopted by central banks around the world, where countries fixed the value of their currencies to a specified amount of gold — a paper note could be freely converted into gold at a specific price.

The system existed from 1870 to 1914, encompassing nearly all countries apart from China. The purpose was to ensure that a country’s money supply was linked to the amount of gold it had in reserves. Gold acted as an anchor of sorts for central banks, preventing the over-issuance of money. A mechanism to keep hyper-inflation in check.

Electronic Money

PROBLEM IT SOLVED – The physical delivery of paper currency or coins between people was time consuming and fraught with risk (e.g. the great gold robbery). In 1861 Western Union established the first telegraph transfer of money. ‘Wiring’ money quickly became the most efficient and safe way to send money over a distance. While electronic money meaningfully increased the ease of money use, this evolutionary phase required a trusted third party or middleman — a critical caveat!

Electronic money evolved through the years, from the early telegraph transfer days to the advent of the internet in 1992, which allowed credit card transactions to flourish globally. In 1998, Paypal addressed the security issue related to using credit cards online by creating a means to transfer money without exposing personal credit card details.

Swedish Case Study

The Swedish government is actively promoting it’s role ushering in a new era of money where paper money no longer exists — with a the goal of becoming the ‘First cashless society’. Only 20% of all transactions in Sweden are made using cash, compared to the global average of 75%.

Launched in 2012, the Swish mobile app payment system allows money to be transferred between bank accounts in real time and has an adoption rate of over 50% of Sweden’s population. A piece in the Guardian noted that even Swedish churches have started to use Swish, displaying their phone number at the end of the service to transfer offerings electronically.

Kenyan Case Study

M-Pesa, Kenya’s mobile payment service is the best example of how electronic currency can flourish in developing nations with limited banking infrastructure. Over 90% of the adult population in Kenya uses M-Pesa as a way to transfer money through text messaging — the electronic funds sit on the SIM card itself.

Cryptocurrencies

PROBLEM IT SOLVED – The biggest obstacle for mass adoption of Bitcoin as a functional currency is whether the innovation actually solves pressing problems with the current system, which is a hybrid of cash and electronic money.

5 Primary Advantages of Cryptocurrencies

Decentralization – Avoiding banks and governments as the trusted middlemen.

Privacy – digital currencies offer the anonymity of cash, coupled with the digital usability of credit cards.

Security – the ledger (history of all transactions) is designed in a way that it can’t be manipulated (immutable) — the power of the blockchain technology.

Global – Ability to transfer value globally without exchange fees, the first truly global currency (a direct competitor to the current de facto global standard – US dollar).

Devaluation Resistant -The Bitcoin blockchain is embedded with a defined factor of scarcity, the maximum amount of Bitcoin that will ever be in circulation is 21 million, this provides a perceived safe guard against devaluation or excessive coin creation.

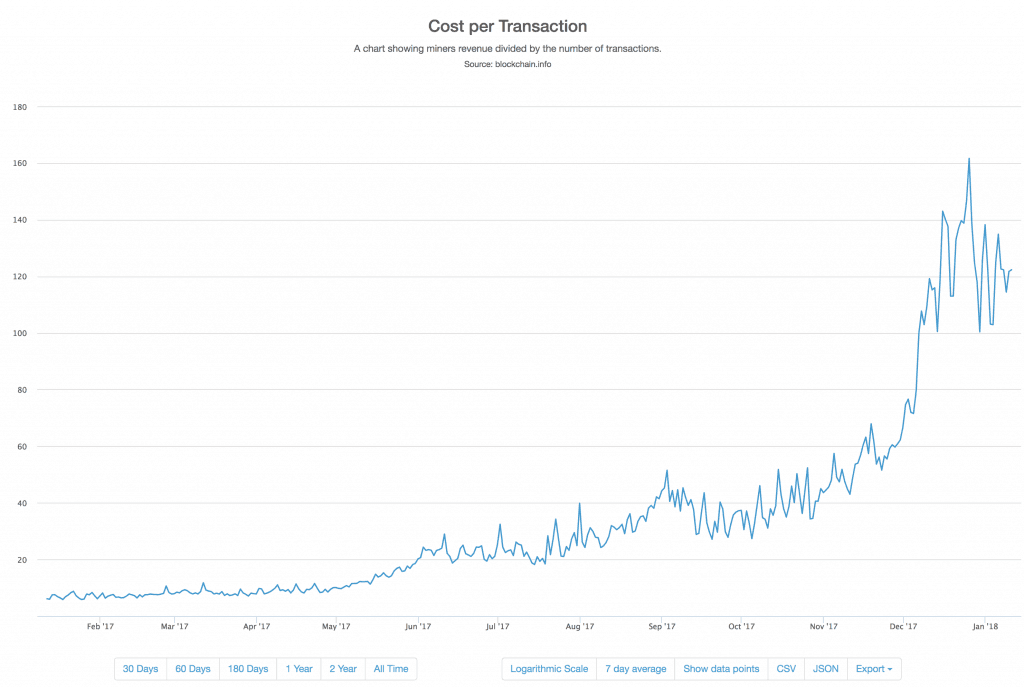

In many ways Bitcoin is the ideal ‘fuck you’ to the out-of-touch Davos establishment. There’s a certain unique enjoyment watching central bankers squirm en masse. However, digital currency, in the current popular form at least (Bitcoin), does have significant practical challenges to becoming a truly functional transactional asset, namely: speed (Bitcoin: 7 transactions per second max vs. Visa: 4,000 transactions per second max) and cost ($120 per average bitcoin transaction).

We absolutely appreciate the fact there are many competing digital currencies that address many of the shortcomings of Bitcoin, but as it stands today Bitcoin is the benchmark.

Conclusion

If we have formally entered the era of ‘establishment’ distrust, digital currency is truly the fifth wave in the evolution of money. It shares many important libertarian traits with gold, devaluation resistance the most important, and thereby is a direct competitor to gold as a store of wealth. The more important question is what the world would look and function like without governments controlling the levers of money supply, apocalyptic to some, utopia to others.

Users should be aware that if they click on a cryptocurrency link and sign up for a product or service, we will be paid a referral fee. This in no way affects our recommendations, which products we choose to review or our advice which is the sole opinion of the authors.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.