Time spent in London earlier this week allowed this writer to monitor closer at hand what is undoubtedly the biggest cock up in post-1945 British politics.

That is former British Prime Minister David Cameron’s decision to call in June 2016 a referendum on ‘Brexit’, an error compounded by his precipitous decision to resign a matter of hours after the result was announced, thereby precipitating a civil war in the Conservative Party, a conflict which continues to this day. Such a ‘wobbly’ is not worthy of a product of Eton, Britain’s most famous school. And this writer, unlike most people, still believes in that formerly celebrated British virtue, the stiff upper lip.

The Great British Cock Up

As for the Brexit issue itself, strong views are not held here save to say that the referendum should never have been called.

There was no popular demand for it and it degenerated into a socially divisive vote on immigration because of the EU principle of free movement of people. But it is clear that the ‘deal’ now negotiated by the hapless British Prime Minister Theresa May will satisfy no one since Britain will remain a ‘rule-taker’ from the EU without the benefits of membership. For this reason it is likely not to pass through Parliament, and under Britain’s unwritten constitution, Parliament is sovereign.

The question will then become whether May will agree to a second referendum or be forced to call a general election. So far, the increasingly confident Labour leader Jeremy Corbyn is, sensibly from his own political perspective, keeping his options open. In such a second referendum it is likely that younger people who are generally pro remaining in the EU will come out to vote in force, whereas many did not bother in the first vote thinking that ‘Brexit’ would not win.

From a financial market standpoint, while the outcome of Brexit is clearly very important for Britain, it remains a relative sideshow for the Eurozone. Indeed, the base case here remains that the Brexit debate will be rendered irrelevant by developments in the rest of Europe and most particularly in Italy.

The Uncertain Fate of the Eurozone

Either the Eurozone moves more explicitly to fiscal integration, as advocated by French President Emmanuel Macron, or it would seem only a matter of time before Italy walks out. Britain would never sign up to fiscal union and so there would be a natural parting of the ways if the Macron agenda is adopted, which is why the Brexit vote was unnecessary.

Meanwhile, if the Macron agenda continues to be resisted by Germany, then the breakup of the Eurozone will come sooner or later anyways. But Britain would be saved the real pain precisely because, thanks to the late and great Margaret Thatcher, it is not part of the euro.

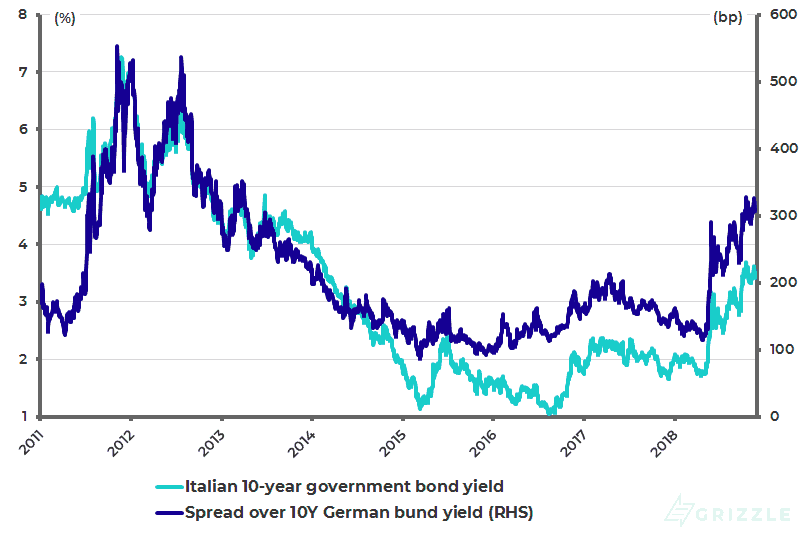

Italian 10-year government bond yield and spread over 10-year German bund yield

The Sad State of Italy’s Economy

Meanwhile, the Italian budget story continues to rumble on with the EU formally rejecting Italy’s budget this week. To be precise, the European Commission rejected on Nov. 21 Italy’s proposed 2019 budget, which projects a fiscal deficit of 2.4% of GDP, and said that “a debt-based Excessive Deficit Procedure is thus warranted”.

Italy still has a government controlled by political parties who are ideologically opposed to the fiscal straightjacket implied by the 1992 Maastricht Treaty and therefore remains on a direct collision course with the European Commission. The Maastricht Treaty requires governments to limit their debt to 60% of GDP. Meanwhile, the conflict between Rome presumably will be happening in the run-up to the May European parliamentary elections which, given the growing threat from populist parties, will be the most closely watched European parliamentary election ever.

Now it remains true that Economic Development Minister Luigi Di Maio, the head of the Five Star Movement, and Interior Minister Matteo Salvini, the head of the League and now the most popular politician in Italy, have remained at pains to stress that they are not advocating leaving the euro.

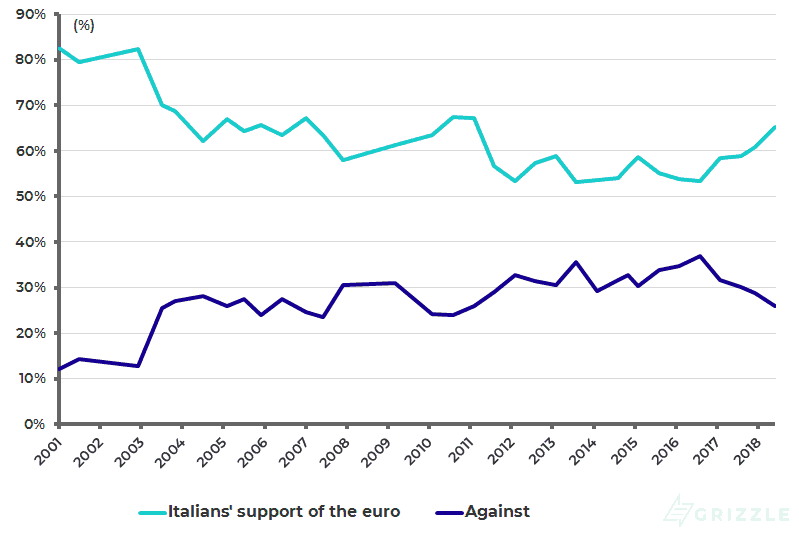

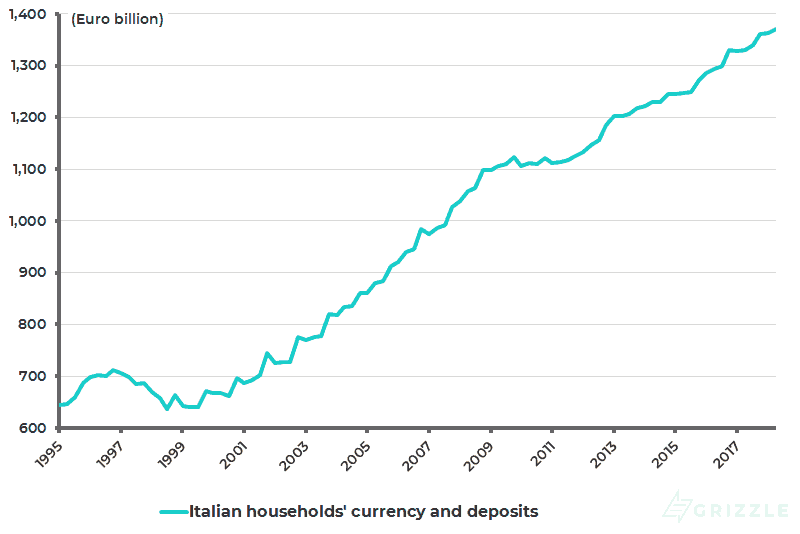

These comments reflect the fact that opinion polls still suggest Italians do not want to leave the euro and a departure from the single currency would clearly threaten the value of Italians’ personal savings which are not inconsiderable. Thus, the latest Eurobarometer survey conducted in September and commissioned by the European Parliament shows that 65% of Italians surveyed were in favour of the single currency, compared with 26% against it (see following chart). While Italian households’ cash and deposits totalled €1.37 trillion at the end of 2Q18 (see following chart).

Eurobarometer survey: % of Italians support or against the euro

Italy household savings as % of gross disposable income

A Potential Political Explosion

The above means that the best way forward to build a consensus in Italy for more radical action, vis-à-vis Brussels, is to push for a more expansionary budget, which is precisely what is now happening, and then see the degree of resistance or pushback encountered from the European Commission. In this respect, it should be remembered that Italy’s budget plans include both the introduction of a form of universal basic income for the poorest, as well as overturning the recent reform of the pension system by lowering the retirement age again from 67 to 62.

This confrontation can easily become politically explosive if, in due course, Brussels is compelled by its own rules to impose EDP penalties on Italy, such as fines, around the same time as the European parliamentary elections are about to take place. This would give those Italian politicians really in favour of leaving the euro the ideal excuse they are looking for to exit.

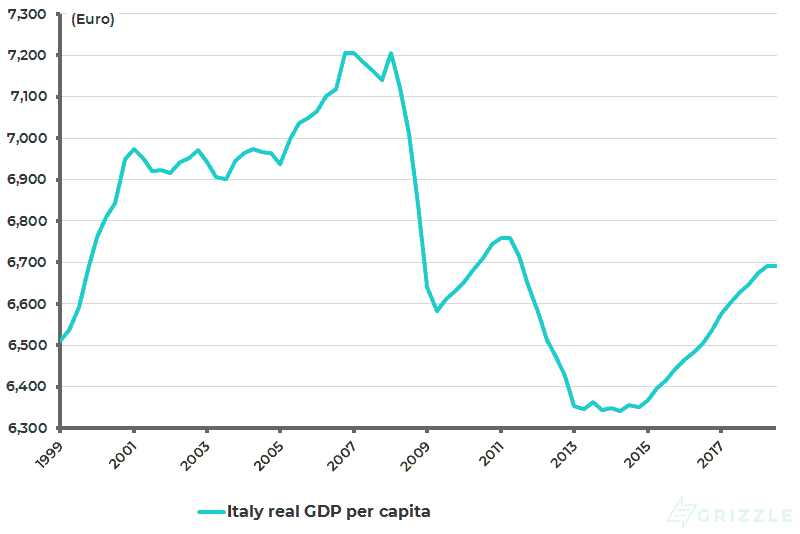

Meanwhile, if the European Union is not going to follow the agenda of French President Emmanuel Macron towards greater fiscal integration, then Italy really has no option but to leave the Eurozone sooner rather than later given the horrific lack of growth since the formation of the euro in 1999. This is a point most clearly demonstrated by the lack of growth in GDP per capita during this 19-year period. Thus, Italian real GDP per capita has risen by only an annualized 0.1% since 1Q99 (see following chart).

Italian real GDP per capita

What Will Become of Brexit?

Returning to the subject of Brexit, faced with this growing existential threat represented by Italy, there has been a limit to which the EU can move to accommodate Prime Minister May during the 17-month-long negotiation conducted by the EU’s chief negotiator, Michel Barnier.

The choice will then be left with the Brexiters inside the Conservative Party, in terms of whether they want to trigger a so-called ‘Hard Brexit’ by voting against the fudged deal now agreed by May and the EU. The only reason for them to vote for such a fudge would be fear of a Labour Government led by Jeremy Corbyn.

The views expressed in Chris Wood’s column on Grizzle reflect Chris Wood’s personal opinion only, and they have not been reviewed or endorsed by Jefferies. The information in the column has not been reviewed or verified by Jefferies. None of Jefferies, its affiliates or employees, directors or officers shall have any liability whatsoever in connection with the content published on this website.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.