The cock-up that former British Prime Minister David Cameron created has become ever clearer. This is a reference, of course, to the seemingly interminable Brexit saga. The decisive vote in Westminster earlier this month has made it self-evident that Theresa May, the hopeless Britain Prime Minister, is now a servant of Parliament. This is as it should be since Parliament is sovereign in Britain.

The Time to Buy British Stocks

The vote also makes it crystal clear that there is not a majority for a so-called “hard” Brexit in Parliament. For this reason the risk-reward ratio favours buying into the shares of domestic British companies, most of which are cheap because of the Brexit uncertainty.

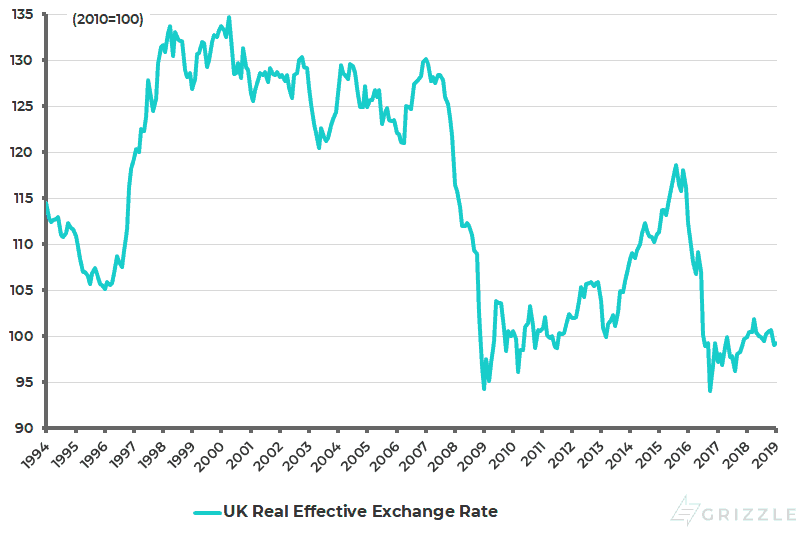

This is because sterling is cheap (see following chart), while the economy is unlikely to suffer the shock the likes of the Bank of England look for with its rather absurd forecast of an 8% decline in British real GDP if such a “hard Brexit” actually occurs.

UK Real Effective Exchange Rate

Potential Options for Britain

What about the far more scary prospect of a Labour Government led by the wonderfully old-fashioned Jeremy Corbyn? It is difficult to see how this is going to happen in the near-term since it is hard to see how the Conservatives could lose a vote of confidence. Indeed for this to happen would require the pro Brexiters on the right-wing of the Conservative Party to vote with the socialist Corbyn, which seems highly unlikely.

That leaves the question of what sort of deal May the plodder can offer to Europe after consulting with Parliament. The reaction of Europe to any such proposed new deal, assuming optimistically some form of soft Brexit option can be agreed, may well be dismissive. In my view that would be the right response from Brussels. For that would leave Parliament facing the reality that the only timely way of addressing this issue is a new referendum.

The doubtless well-intentioned May continues to oppose this option for fear of overturning the “popular” vote. But what about the 48% who voted “Remain” and the 28% of the electorate who did not bother to vote at all in the June 2016 referendum? In the absence of such a new referendum the saga can run and run. But a hard line from the European Commission can force a quicker resolution. In the meantime, Brexit is very important for Britain but a sideshow for Europe and the world economy.

The “Japanification” of Eurozone Banks

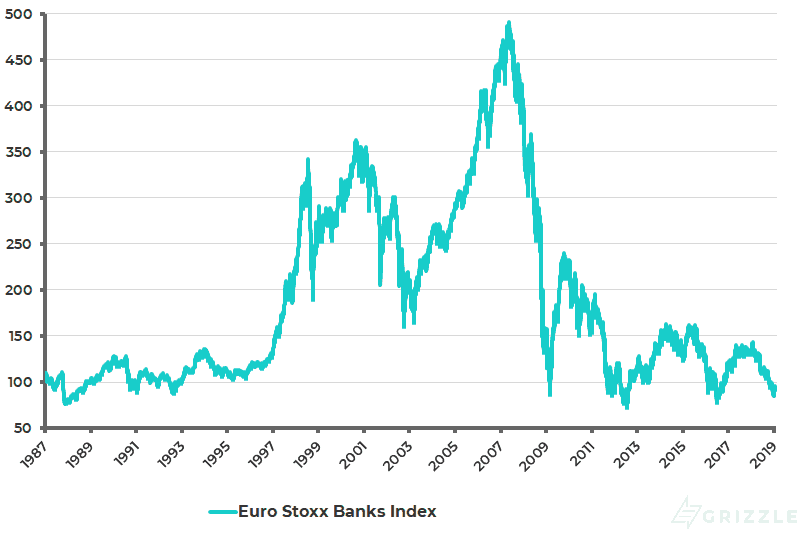

None of the above is to say that the rest of Europe is in great condition. While Brexit has been making the headlines the long-term chart below shows the scary condition of European banks with the Euro Stoxx Banks Index not so far above its previous lows reached since 1988. Indeed this chart represents what could be termed the “Japanification” of Eurozone banks as ultra-low bond yields continue to make it hard for these banks to make money. The ten-year German government bond now yields only 0.19%.

Euro Stoxx Banks Index

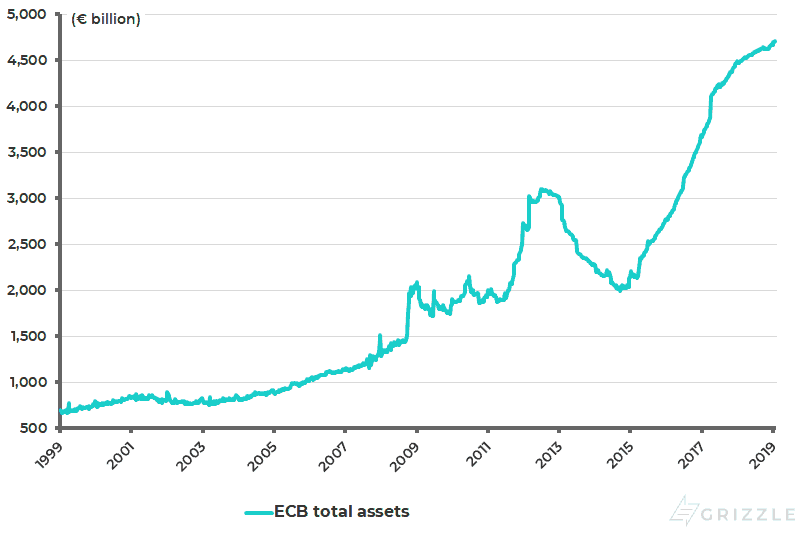

In an announcement this week, the European Central Bank (ECB) has begun to move off its normalization narrative, in terms of monetary policy and ending quantitative easing, when ECB Governor Mario Draghi acknowledged in a press conference that the economic outlook had deteriorated since December when the ECB stopped its balance sheet expansion.

The ECB balance sheet has risen from €1.988 trillion to €4.706 trillion since its quantitative easing began in October 2014 (see following chart). Draghi’s comment came at a time when it has become hard for the ECB to ignore the deteriorating external data and the negative implications this has for employment.

ECB balance sheet

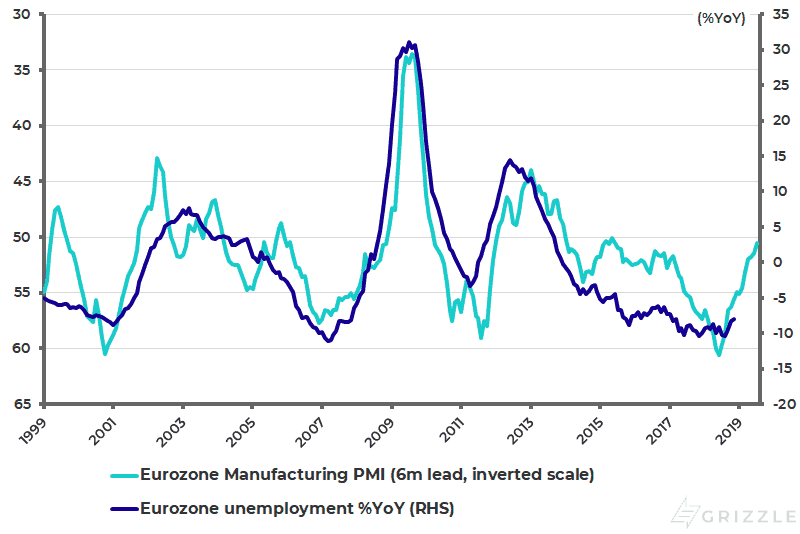

The correlation between the Eurozone Manufacturing PMI, with a six-month lead, and unemployment growth has been a negative 0.82 since 2000, and this PMI has declined by 17% from 60.6 in December 2017 to 50.5 in January 2019 (see following chart). Still, so far, there has yet to be a visible deterioration in domestic demand. The key country to watch in this respect, with its exports declining by 0.4%MoM and being flat YoY in November, is Germany, the core of the Eurozone.

Eurozone Manufacturing PMI and Unemployment Growth

The ECB’s reluctance until last week to move away from the normalization narrative has been in part political since it would be preferable for ECB President Mario Draghi not to start a new initiative in monetary policy prior to his departure from the scene at the end of October, with his last monetary policy meeting due to be held on Oct. 24. For this reason, a successful trade deal between the U.S. and China could be the sort of positive catalyst required to allow Draghi to maintain the normalization course in terms of resisting renewed balance sheet expansion. But in the absence of such a development, and a trade deal by the March 1 deadline remains the base case here, the risk remains that Draghi will have to suffer the embarrassment of a U-turn path prior to his departure. For now, however, the ECB balance sheet is on hold with the ECB re-investing maturing bonds.

Meanwhile, market focus on the systemic political risks surrounding the Eurozone, and in particular Italy, will resume with the European Parliamentary elections in May when the populist parties will be seeking to build a presence to pursue reform from within in the Eurozone legislature.

The views expressed in Chris Wood’s column on Grizzle reflect Chris Wood’s personal opinion only, and they have not been reviewed or endorsed by Jefferies. The information in the column has not been reviewed or verified by Jefferies. None of Jefferies, its affiliates or employees, directors or officers shall have any liability whatsoever in connection with the content published on this website.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.