C3ai is yet another hyped up software as a service (Saas) stock going public this month.

However, with massive consumer companies like DoorDash and AirBnb hogging the spotlight, this may end up being the low-key IPO of December.

To help you decide if you should ignore the big guys and put your money into C3.ai’s relatively puny $3 billion IPO we are going to break down the valuation in detail and how you should trade it.

C3.ai in 2 Paragraphs

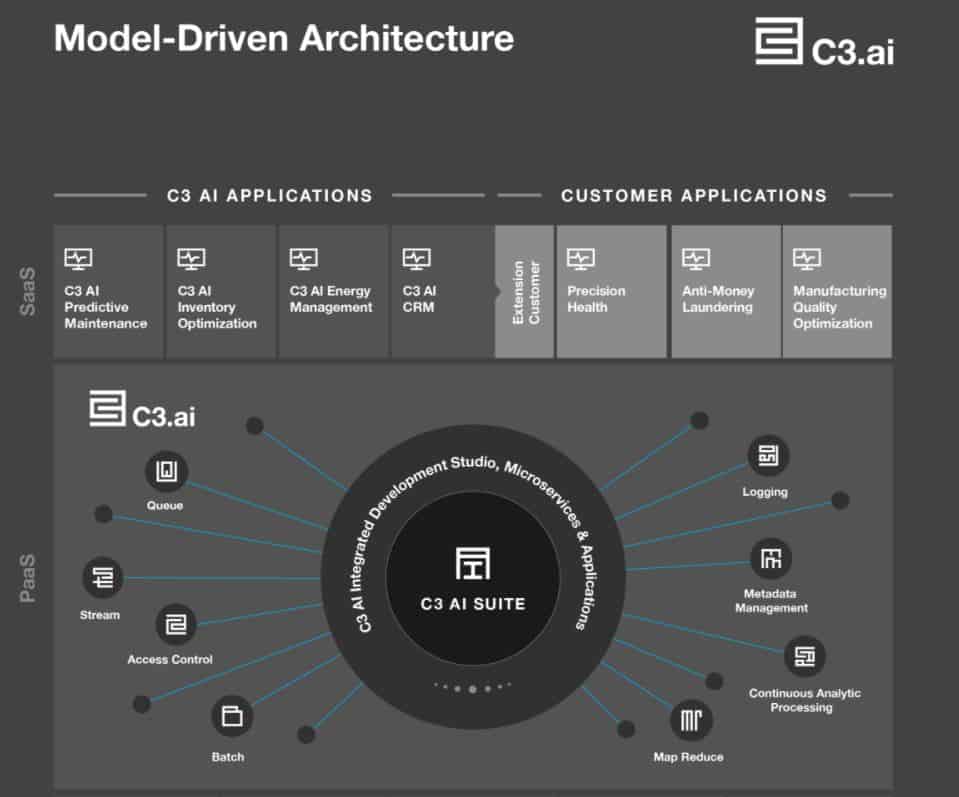

In simple terms, C3.ai provides a software platform companies can use to create artificial intelligence applications to help them run their business. Using C3.ai companies can save hundreds of coding man hours and lots of money by building software in less time. Even more important is the software integrates with many more third-party software programs than a custom-built solution.

In the old days of coding, large teams wrote custom code that often broke and only integrated with very specific outside systems. C3.ai allows fewer team members to write more programs in less time and have them work with many different third-party programs, not just one.

C3.ai Product Offerings

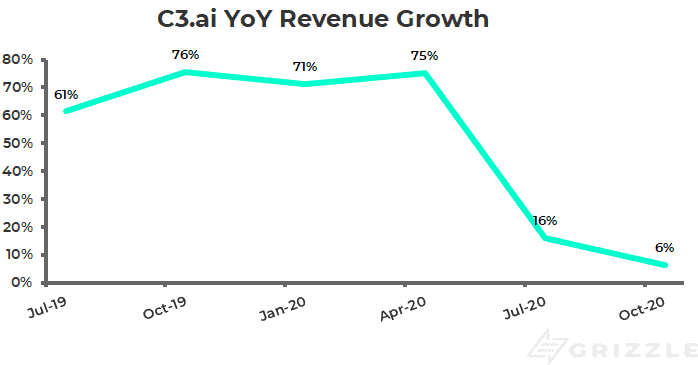

Houston We Have a Growth Problem

C3.ai sells software for a subscription fee. This is called software as a service or SaaS.

Like any other Saas business in 2020, the value of the stock depends on how fast the company is growing revenue.

More revenue growth = higher stock multiple

Starting our valuation with revenue growth quickly revealed the company’s biggest flaw.

Growth is just not there.

C3 entered 2020 growing at 75% a year, a blistering pace that put it up there with the fastest growing software stocks on the market.

Then the pandemic hit.

Growth has cratered in 2020 and as of October was up only 6% from the prior year.

This is not the type of growth investors expect from a hot tech company.

So why has C3.ai’s growth flatlined while dozens of tech peers have been huge beneficiaries of the pandemic as consumers and employees are stuck in their homes?

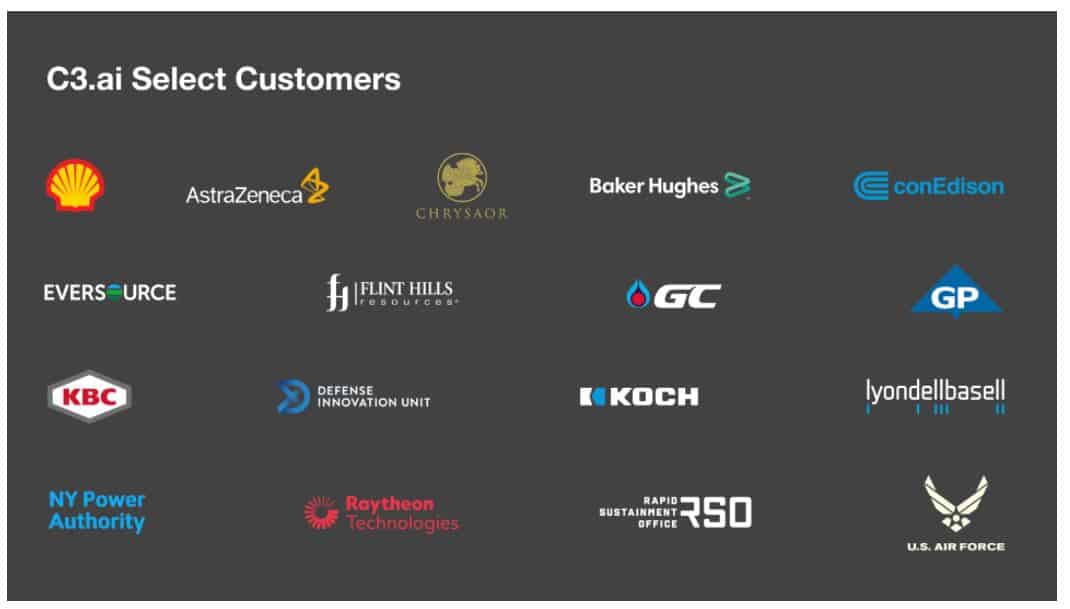

For the answer, look at the customer list.

C3.ai is a tech company but customers are old-economy cyclical businesses.

We have oil producers, utilities, chemical makers and government entities.

No wonder the fall in commodity prices and industrial activity had an effect on C3.

C3.ai is a vaccine play NOT a COVID play.

This presents an opportunity for investors as we expect growth will return as industrial activity and energy prices rebound.

Over the longer term, until C3.ai expands beyond industrial customers revenue is going to ebb and flow with industrial production and commodity prices.

How Do We Price This Kind of Company

Software companies are priced based on how fast they are growing and if they lose money or generate profits.

Looking first at growth, C3.ai’s recent revenue growth of only 6% is far below the median future growth rate for the industry of 20%.

We estimate the company will grow 25% in the coming 12 months as the Coronavirus fades and the economy recovers, but this is still far lower than the 75% growth they were doing prior to the pandemic.

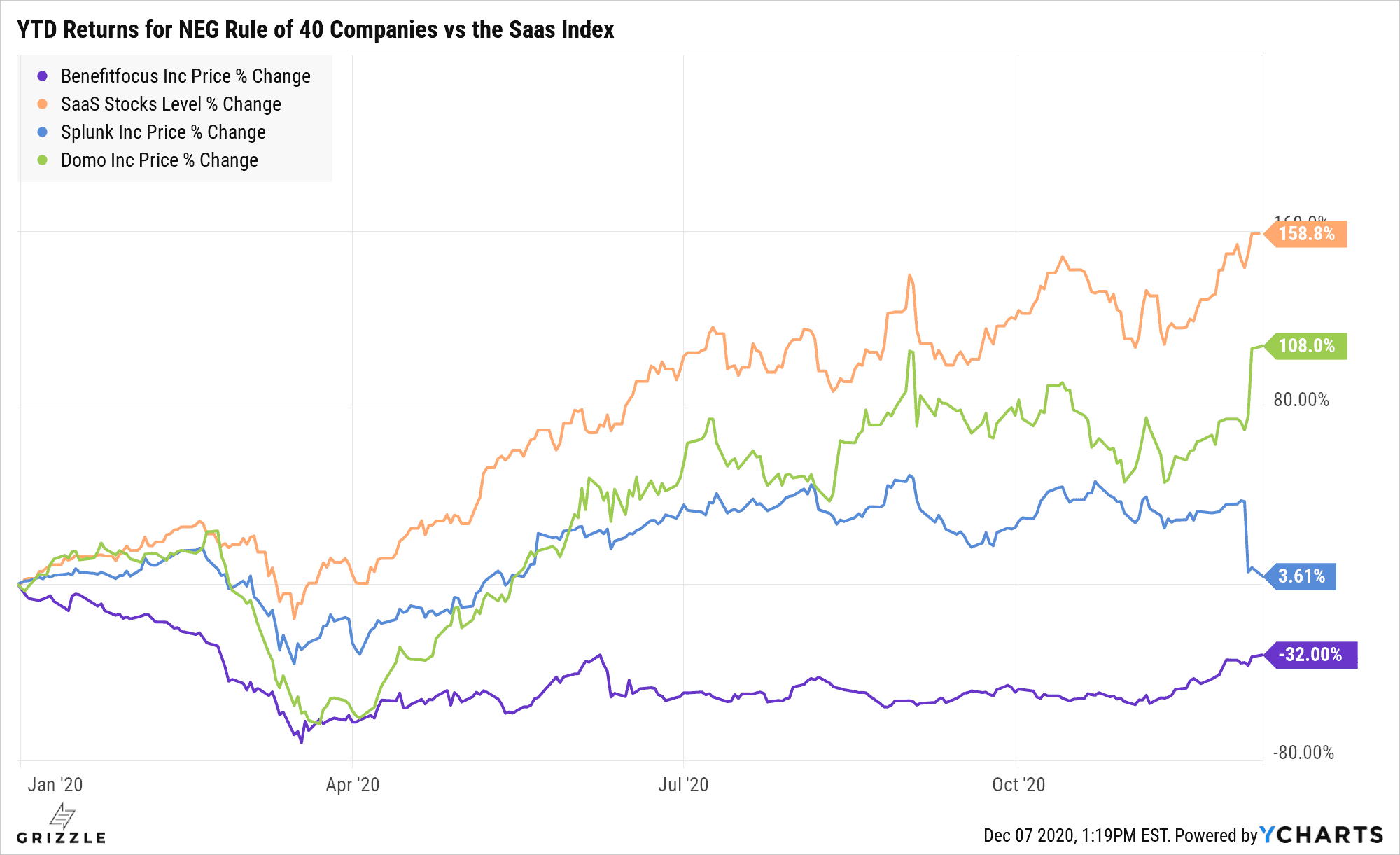

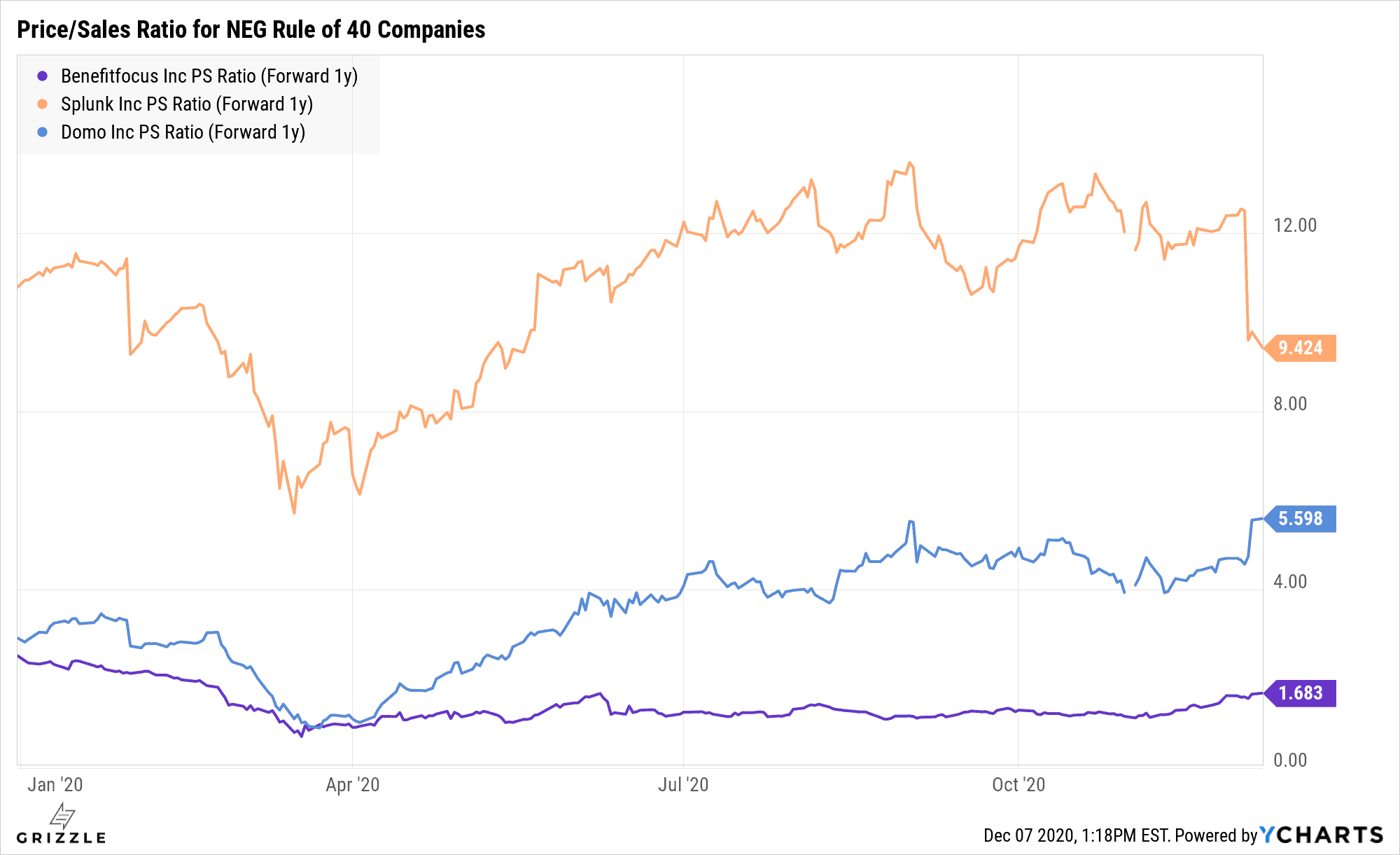

Taking their LTM free cashflow margin of -25% and adding in the LTM growth rate of 15, C3.ai’s Rule of 40, a popular software metric is pretty terrible at (-10%).

Only three other stocks have negative rule of 40s (SPLK, DOMO and BNFT) and they all have underperformed the software group, some quite significantly.

A Negative Rule of 40 = Disappointing Returns

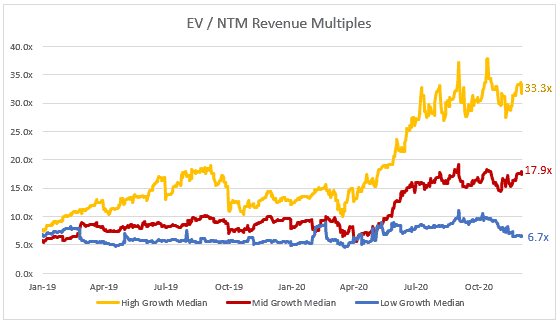

The growth rate and disappointing rule of 40 put C3.ai in the low to mid growth bucket.

Looking at the price to sales multiple for the different growth buckets, the mid-growth bucket has an enterprise value to next year’s revenue of 18x.

Revenue Multiple by Growth Bucket

Even with our expecations that growth rebounds in 2021, C3.ai will be growing ~20% slower than the top end of the mid growth bucket, deserving a 14x revenue multiple.

And 14x revenue doesn’t even penalize the company for worse than average losses and slower than average growth.

With the company still losing money and the growth outlook uncertain, it is pointless to forecast a fundamental value.

A relative multiple to peers is how the stock will trade over the next few years and is the most helpful metric to analyze the company’s attractiveness over the medium term.

Summing it All Up: How to Trade C3.ai

C3.ai is going public with most metrics in the toilet.

However, that also leaves room for results to exceed expectations.

On one hand the IPO price ($42/sh or 15.5x sales) is very expensive compared to others with similar profit margins.

Price/Sales Multiple for Peers with Similar Margins

On the other hand, the company is highly levered to a rebound in industrial activity and energy prices and this rebound will continue as the vaccines roll out in 2021.

C3.ai was growing 75% before COVID-19 hit.

Where the stock goes from here is simple.

If growth is higher than 40% next year, the multiple and the stock could double.

If growth fails to rebound quickly enough, the stock is going 10%-30% lower.

C3.ai has the backing of Microsoft who is participating in the IPO and big M’s endorsement is probably enough to send the stock higher in the first few weeks of trading.

If you want in on this IPO, putting a fraction of your desired amount in at the start will give you time to see how the stock performs out of the gate.

You can then wait for confirmation through earnings that growth is accelerating before putting in the rest.

If the growth rebound disappoints you’ve minimized your losses through smart position sizing and if management turns things around you will have benefitted from having at least some skin in the game.

Successful investing is just as much about sizing positions and timing your exit and entry as it is about picking the right company.

C3.ai offers a much better solution compared to the old way of writing software code, the question becomes, can they convince enough customers to give them a spin.

A Note on the Share Count

C3.ai has more stock options than any other IPO this month.

Most IPO’s have about 20% more shares if you add in options and warrants. C3.ai’s share count is a whopping 60% higher when we include options and warrants.

More stock options outstanding mean more dilution for current shareholders over time.

It also means C3’s price to sales multiple is really 23x revenue, not 14x.

As these stock options are cashed in and sold they will put relatively more downward pressure on the stock price compared to AirBnB, DoorDash, Affirm and others.

Something to keep in mind as you decide which December IPO to buy if any.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.