Cadence Design Systems (NASDAQ: CDNS) released Q4 2019 earnings meeting analyst estimates, but growth began to slow on both the top and bottom lines.

The Electronic Design Automation (EDA) firm brought in sales for the quarter of $600 million which surpassed consensus estimates of $595.5 million.

Revenues for the quarter were 5% higher compared to the same quarter last year. While the top-line growth for the company isn’t eye-popping, that’s not necessarily surprising in the Electronic Design Automation (EDA) software industry given the limited customer base. Overall, Cadence is well positioned with rivals like Synopsys (NASDAQ: SNPS) and Siemens-owned (ETR: SIE) Mentor.

On the bottom line, Cadence reported $0.54 earnings per share which just barely beat Wall Street expectations of $0.53 per share.

The company also updated their guidance for next quarter and the full year 2020. Cadence expects total revenues between $610 million to $620 million in Q1 2020 and $2.545 billion to $2.585 billion for the full year.

Earnings per share for this year are expected to be between $0.53 to $0.55 in the first quarter and between $2.40 and $2.50 for the full year.

The guidance for the first quarter was slightly below Wall Street expectations but the full-year guidance on both the top and bottom line comes in above the consensus estimates. The company also indicated that it expects to use approximately 50% of free cash flow to repurchase shares throughout the year.

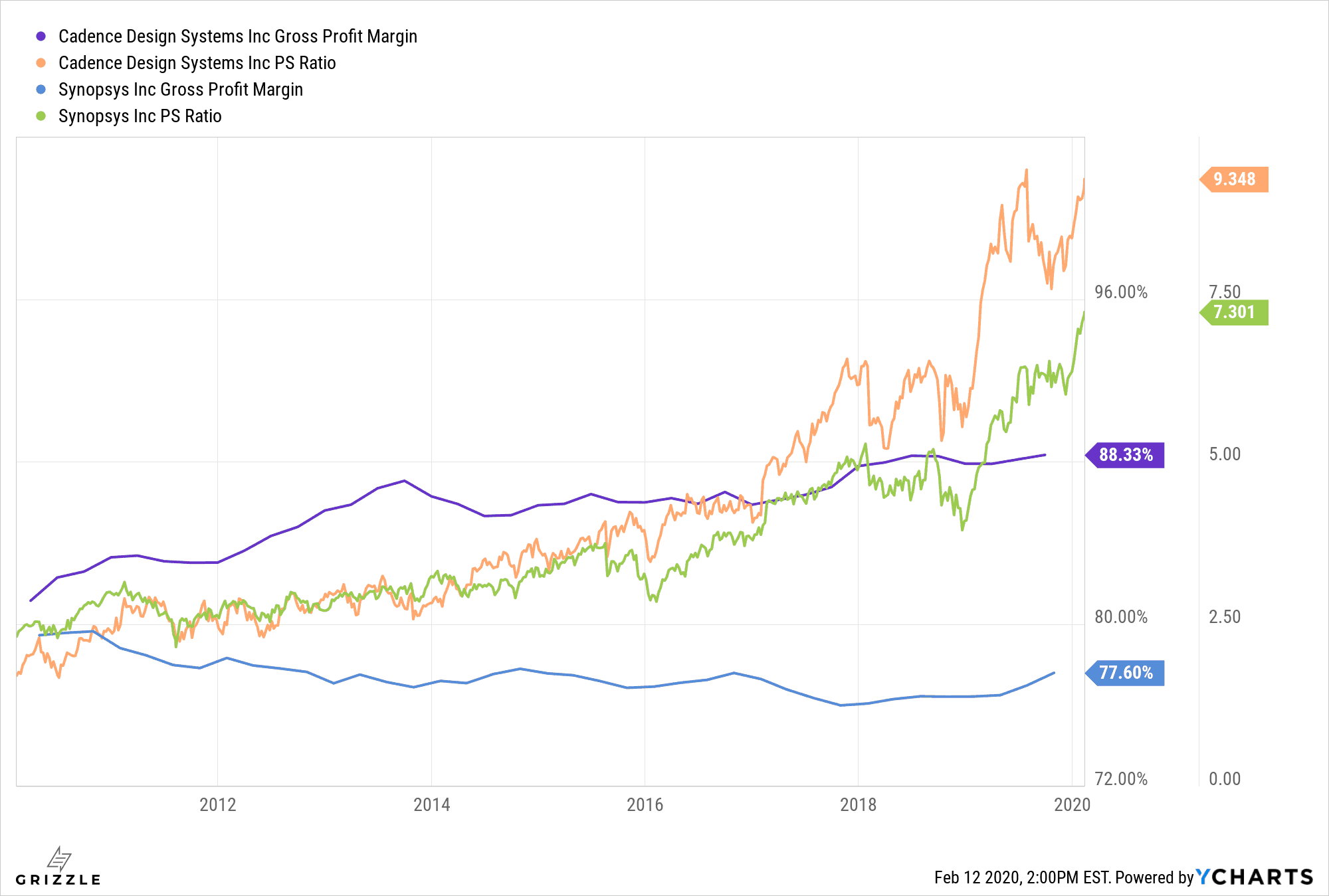

Cadence was the stock that we liked best when we did a screen of software companies late last year for free cash flow yield, revenue growth, and return on equity. While its 10% year-over-year revenue growth has been lacking for a typical software company, the fact that Cadence has consistently been able to push up its gross margins over the long haul has been most impressive.

The market is rewarding those healthy margins despite a typical focus on top-line growth in the tech sector, with Cadence having a 9.3x price-to-sales ratio compared to its closest peer Synopsys at 7.3x.

But when you look at the list of $10B+ tech companies with gross margins over 85% and revenue growth over 10%, Cadence is in select company. A screen for those metrics puts Cadence on par with heavyweights like Adobe (NASDAQ: ADBE), Autodesk (NASDAQ: ADSK), VMWare (NYSE: VMW), Ansys (NASDAQ: ANSS), Constellation Software (TSE: CSU) and Paycom Software (NYSE: PAYC). Those companies trade in a range of 6x – 23x price to sales which makes Cadence seem more attractively priced.

Cadence stock was on a tear in 2019, netting investors a return of nearly 60% over the course of the year and that has continued thus far in 2020 with the stock gaining over 9% year to date, hitting its 52 week high today. After releasing earnings the stock was down 1% in after market trading at the time of publishing.

Full Disclosure: The author purchased shares of Cadence after performing due diligence on the company, prior to the earnings release.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.