There is no doubt that energy is a core part of the fractious political debate in America in stark contrast to the mushy consensus that prevails on the subject in Europe.

It is also clear that inflation and the price of “gas” at the pump are closely intertwined in the American mind.

For this reason, there is also no doubt that the Biden administration was focused on trying to keep the price of oil down before the mid-term elections.

This explains Biden’s trip to Saudi Arabia in July and the resulting Washington displeasure when OPEC Plus went ahead with production cuts at its meeting in Vienna on 5 October.

It also explains in part the effort in recent months to revive talks with Iran, efforts which seemingly hit an insurmountable roadblock given recent developments in terms of demonstrations in the cities of that country.

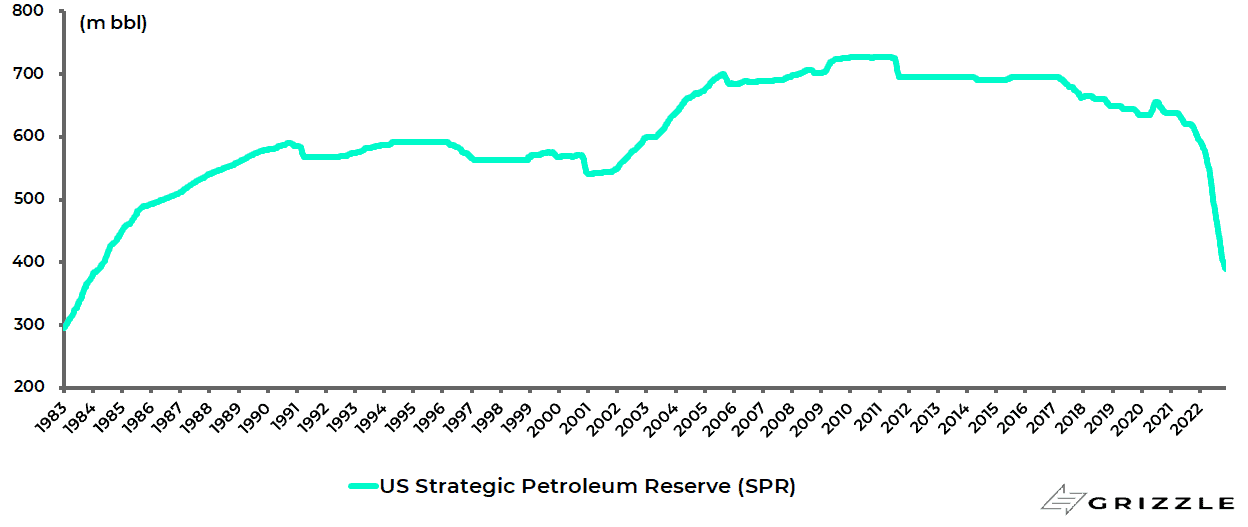

But perhaps the most dramatic manifestation of the Biden administration’s focus on oil has been the accelerating draining of America’s Strategic Petroleum Reserve (SPR) to a near four-decade low.

The US SPR has declined by 204.6m barrels so far this year to 389.1m barrels on 25 November, the lowest level since March 1984.

US ending stocks of crude oil in Strategic Petroleum Reserve (SPR)

This process got a major boost following the invasion of Ukraine with the decision at the end of March to release 180m barrels over a period of six months with sales of the last 15m barrels to be delivered in December.

The result is that SPR reserve, initially set up in 1977 to deal supposedly with national emergencies, has this year seen its largest drawdown ever.

This has the practical consequence of increasing the bargaining power of OPEC and, yes, Russia.

All of the above should be seen in the context of this writer’s longstanding bullish view on oil and energy stocks, which is maintained here on the view that this cycle is different as a result of the lack of investment in recent years by the oil and gas industry.

This in turn is the direct consequence of the intensifying political attack on fossil fuels in recent years manifested in the investment world by the movement known as “ESG”.

This has happened at a time when 82% of world energy demand was still met by fossil fuels in 2021, according to the latest BP Energy Book.

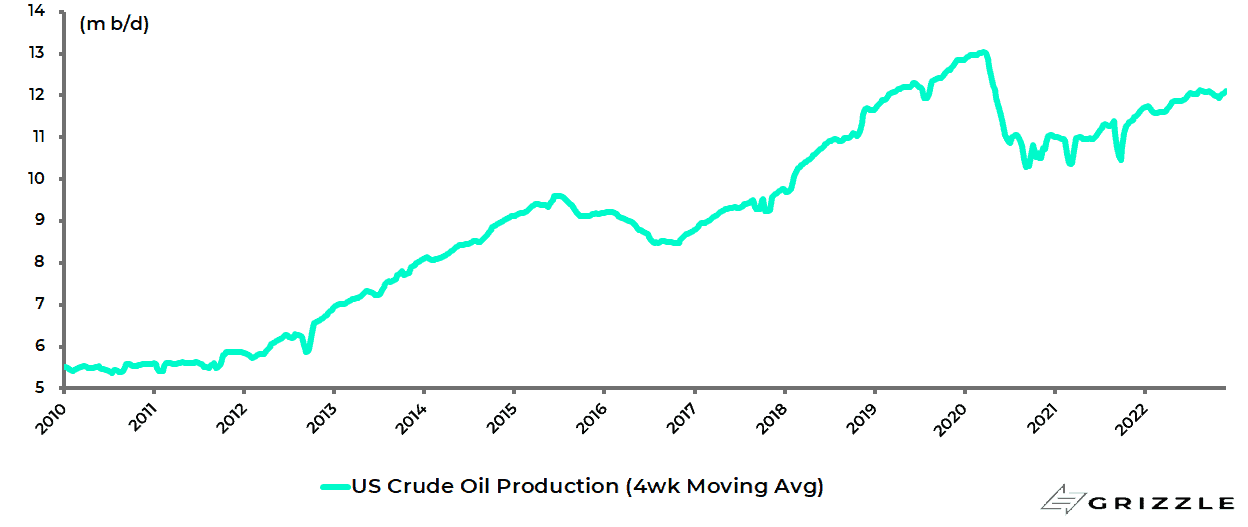

Meanwhile it is also worth highlighting again that American domestic oil production has, for now at least, peaked.

US crude oil production peaked at 13m barrels/day in March 2020 and is now running at 12m barrels/day (see following chart).

US crude oil production

This is in part the response of the political campaign against the industry which is why the Republicans have argued that the Democrats’ regulatory attack on fossil fuels is responsible for higher prices.

But the decline in American production also reflects the geological fact that the best areas of US shale have already been exploited, as previously discussed here (see A third Major Oil Crisis Is On The Horizon, 22 July 2021).

The final but also highly relevant point is that oil and gas executives have in recent years been focused on running their companies for cash flow and dividends, a fact which has been appreciated by those investors allowed to own energy stocks.

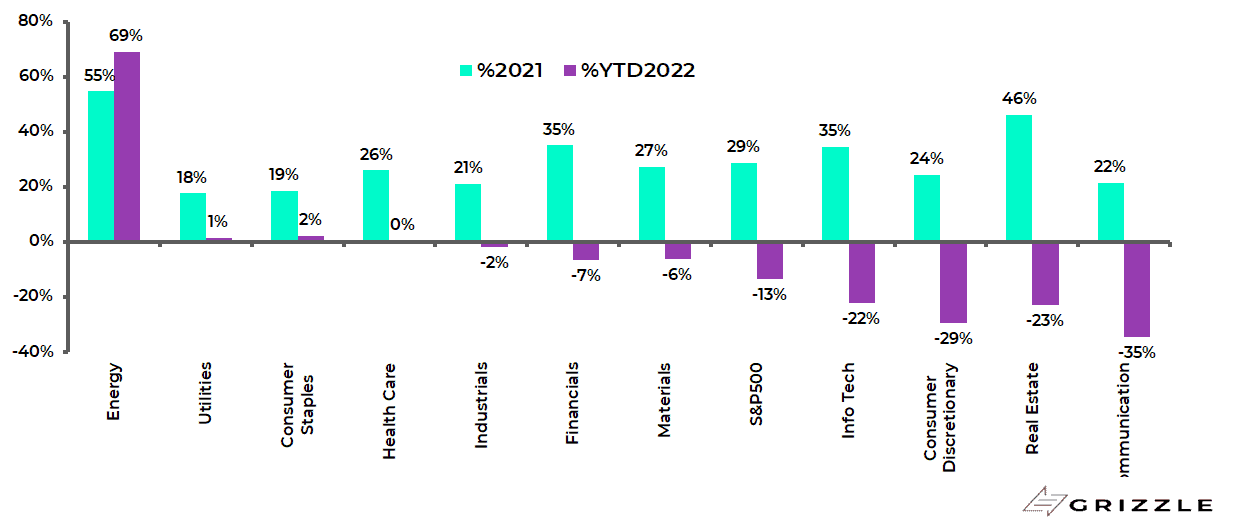

The energy sector was the best performing sector in the S&P500 last year and remains the best performing year to date.

The S&P500 Energy Index rose by 55% on a total-return basis in 2021 and is up 69% year-to-date.

S&P500 sector performance on a total-return basis (2021 and 2022 year-to-date)

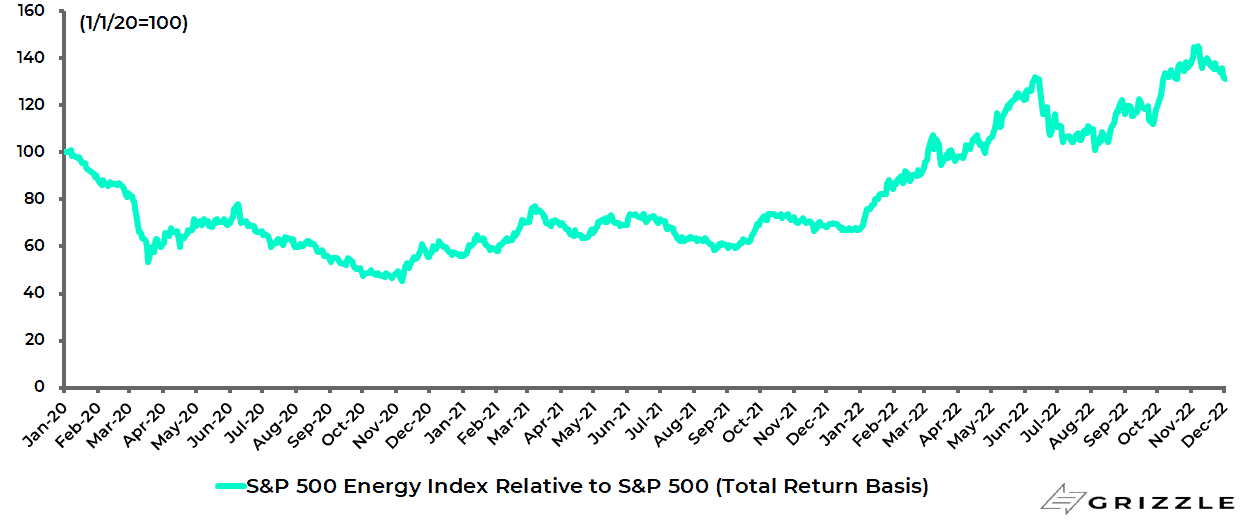

Indeed it has now outperformed the S&P500 by 134% on a total-return basis since the start of last year.

S&P500 Energy Index relative to S&P500 (total-return basis)

Such a performance raises the obvious risk that all the good news is in the price.

True, there are some risks.

One risk is that a sudden end to the Ukraine conflict would cause a sharp correction in energy stocks.

Such a development should be viewed as a buying opportunity given the structural under-investment argument.

Conversely, energy stocks are also a hedge against a further escalation of Ukraine exacerbated, from an oil price perspective, by Europe’s decision to ban the imports of Russian oil from 5 December.

The other risk is demand destruction given the energy sector’s undoubtedly cyclical nature and the mounting risk of a global recession.

But if this is a real risk, it remains the case that the fundamental lack of supply creates a different dynamic from previous cycles.

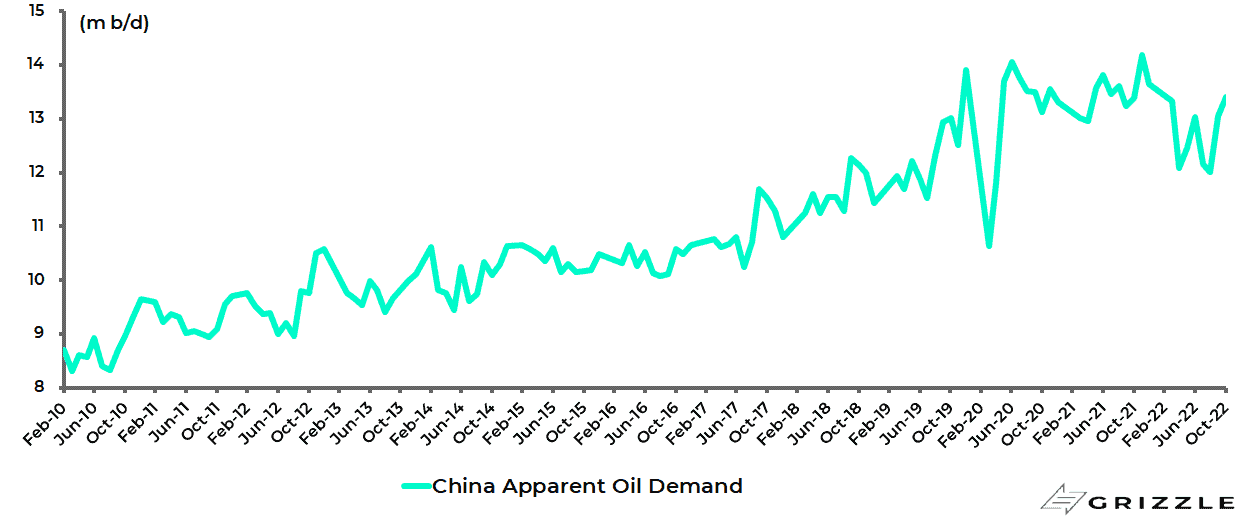

Meanwhile it also remains the case that the one area for now where there is currently concrete evidence of demand destruction is China, not the Western world, because of the impact of Covid suppression on the mainland economy.

Thus, China oil demand declined by 6% YoY to 12.7m barrels/day in the six months to October.

China oil demand

China Closet COVID Easing is a Go

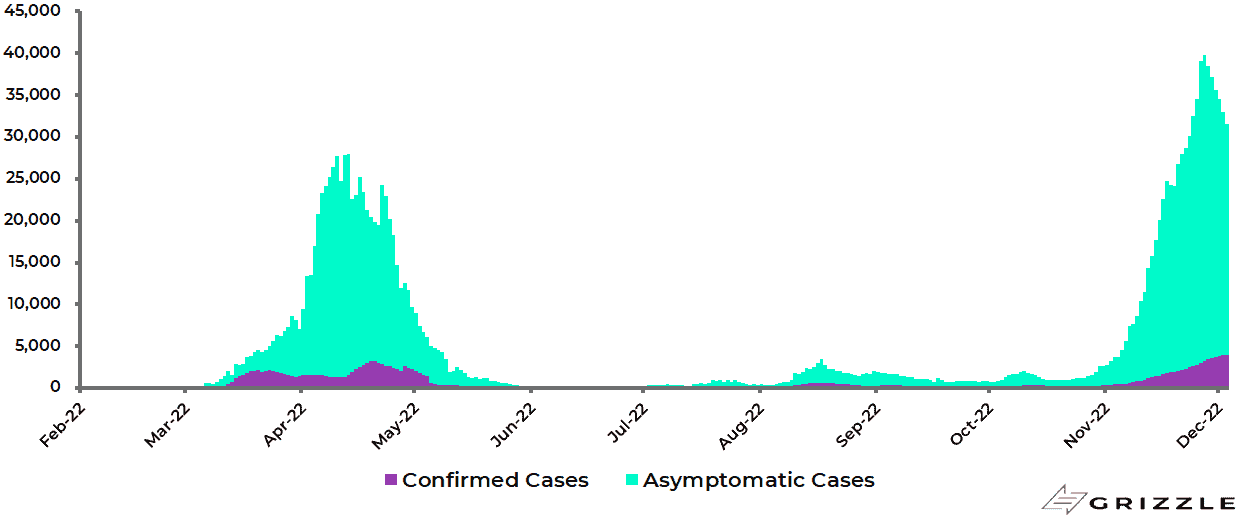

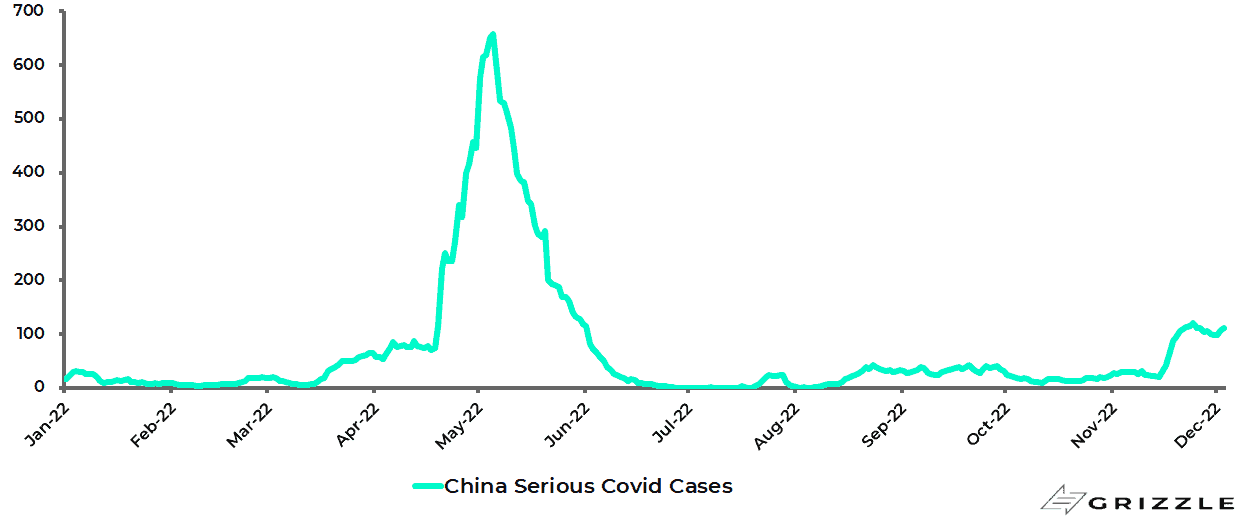

Still China has now commenced a policy of closet Covid easing as evidence grows that it has finally lost control of the virus in the context of the highly infectious Omicron.

Cases surged from 719 on 1 October to a peak of 40,347 on 27 November and were 31,824 on 3 December, though serious cases remain very low at 111.

China daily new Covid cases

China number of serious Covid cases

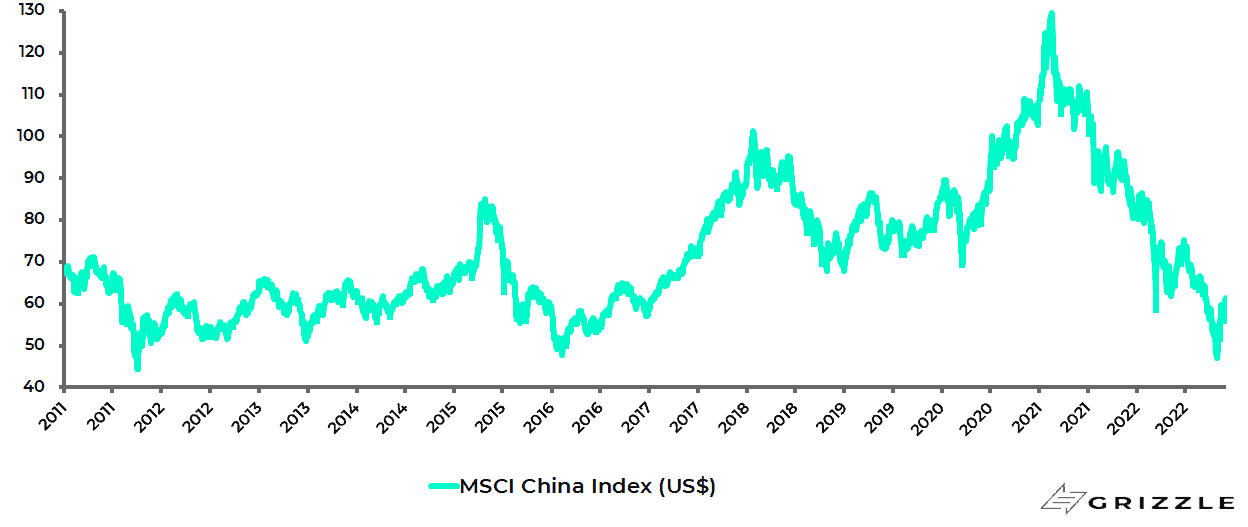

This is causing growing confidence that there will be a de facto opening up of the mainland economy with the MSCI China Index up 30.8% since bottoming at the end of October, a rally also helped by a support package for the residential property market announced on 13 November.

MSCI China Index

Such an outcome would be positive for the oil price.

The views expressed in Chris Wood’s column on Grizzle reflect Chris Wood’s personal opinion only, and they have not been reviewed or endorsed by Jefferies. The information in the column has not been reviewed or verified by Jefferies. None of Jefferies, its affiliates or employees, directors or officers shall have any liability whatsoever in connection with the content published on this website.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.