There is no doubt that expectations of monetary tightening are accelerating as reflected in the damage done to the profitless thematic-tech segment of the US equity market in the recent past.

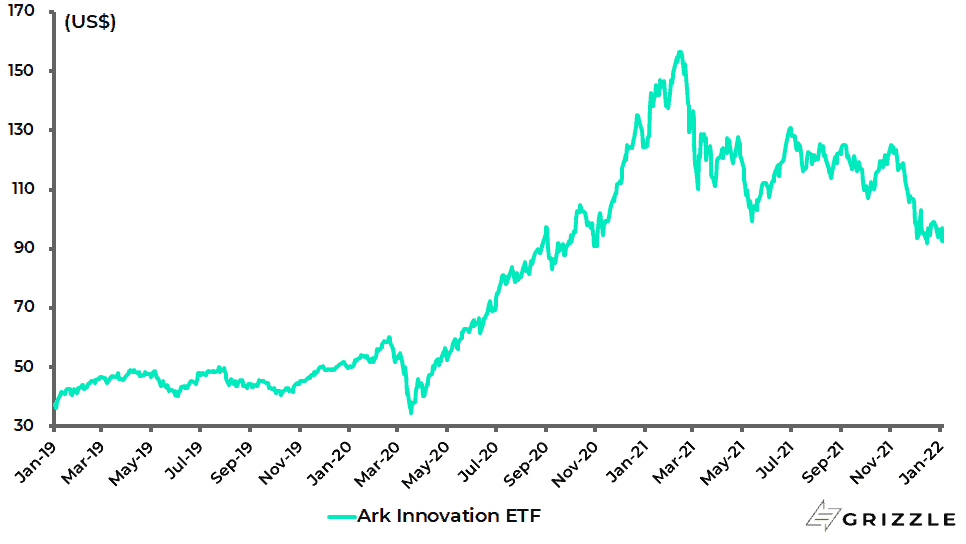

This can be seen in the deteriorating breadth of the US stock market as well as in the hit taken by many of the stocks in the widely followed ARK Innovation ETF (ARKK), save of course for the ultra-resilient Tesla which has continued to confound the shorts.

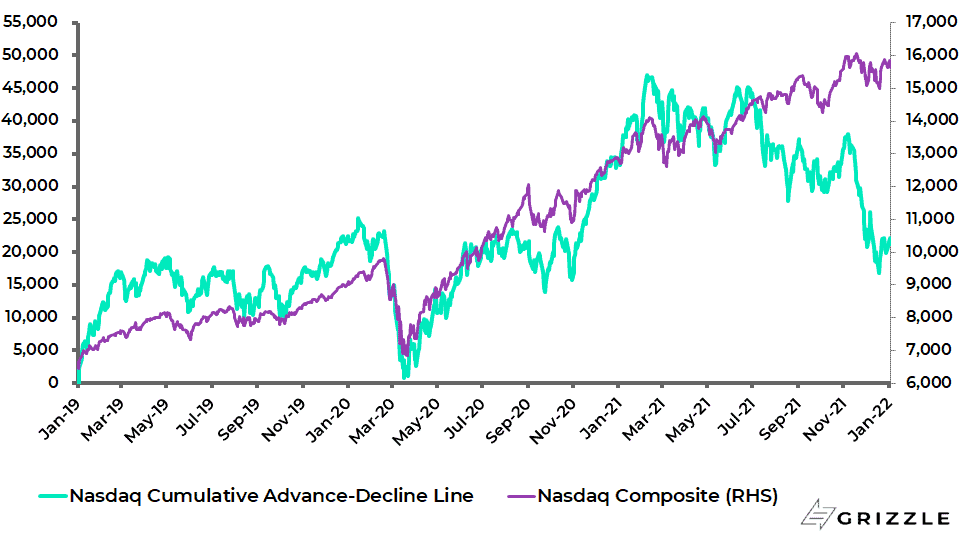

The Nasdaq cumulative advance-decline ratio since 2019 declined from 37,959 on 8 November to 16,759 on 20 December, the lowest level since late October 2020, and is now 21,229 as stocks have rebounded into year-end.

Nasdaq cumulative advance-decline since 2019 and Nasdaq Composite

While the ARK Innovation ETF (ARKK) is now down 42% from the peak reached in February 2021.

ARK Innovation ETF

The amount of money invested in ARKK is now US$15.6bn, down from the peak of US$28.2bn reached in February 2021.

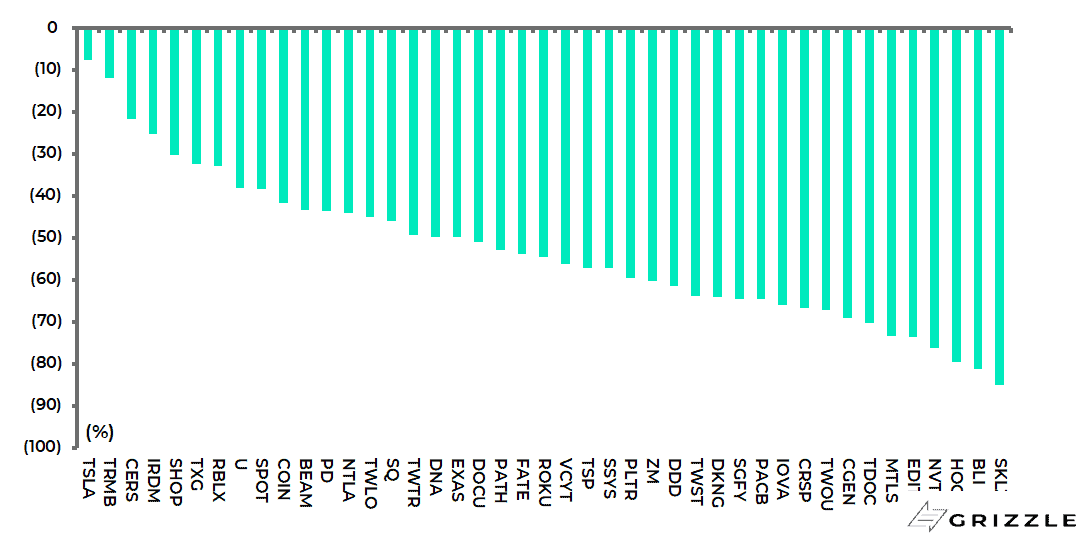

It is also worth noting that within the 43 stocks in the ARKK basket only two stocks have declined less than 20% from their 52-week high.

Stocks in the ARKK basket: % down from their 52-week high

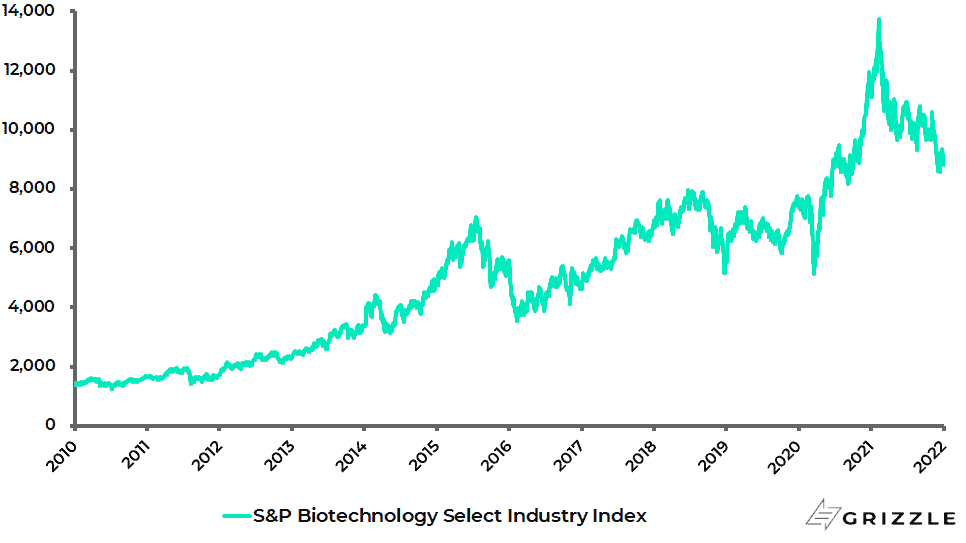

Biotech has been another high beta area of the market which has suffered damage of late. The S&P Biotechnology Select Industry Index has declined by 36% from its peak reached in February 2021.

S&P Biotechnology Select Industry Index

Don’t be Fooled if Inflation Data Cools for a Period

The above market action has occurred as the Federal Reserve has brought forward the end of tapering from June to March while money markets are now expecting 75bp of Fed tightening starting in May whereas three months ago half of the FOMC meeting participants were predicting no rate hikes at all in 2022.

All of the above is the result of Fed chairman Jerome Powell’s abandonment of the word “transitory” in his testimony before Congress on 30 November previously discussed here (see All Eyes are on the Fed’s Favorite Gauge of Inflation, 22 December 2021).

When such a shift in consensus happens it is always useful to ask where the consensus can be wrong. The obvious answer is that, just when the Fed and the consensus of talking heads have finally admitted that inflation is more of a problem than they were previously owning up to, the narrative goes the other way for a period.

On this point, there is indeed the potential for the narrative to go the other way for a while following the November US CPI report which saw the biggest inflation number in a generation.

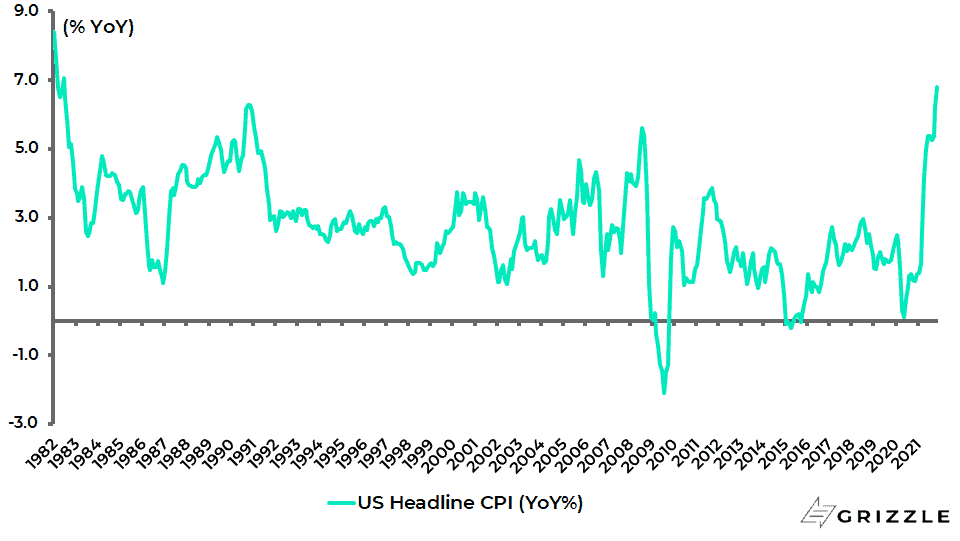

US CPI inflation rose from 6.2% YoY in October to 6.8% YoY in November, the highest level since June 1982.

US CPI inflation

Why is this?

First, there is the base effect which suggests a likely short-term peaking out of inflation in March which is now the same time as the Fed is expected to end its asset purchases by when the Fed balance sheet will be US$8.94tn.

This is because inflation started accelerating last March, up from 1.7% YoY in February 2021 to 2.6% YoY in March 2021.

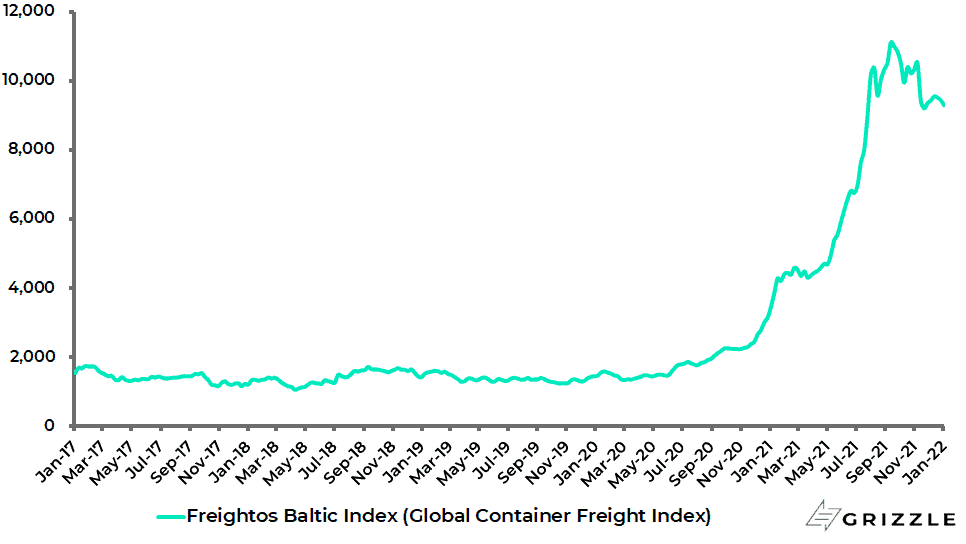

Second, there is likely to be growing evidence this quarter of a peaking out of the lockdown-triggered supply chain bottleneck issues as the pre-Christmas buying demand cools off.

With imports in America typically peaking in October, two months ahead of the seasonal peak in retail sales in December, it is interesting that shipping rates look like they are now rolling over.

The Freightos Global Container Freight Index has declined by 16% since peaking in September.

Freightos Global Container Freight Index

It is also the case that the pandemic, and the related fear of shortages, should have further increased pre-Christmas buying demand this past year.

For the above-mentioned bottlenecks are not the key drivers of the inflationary pressures which so surprised the Fed last year.

Rather they are demand-driven, in significant part, financed indirectly by the Fed and other G7 central banks.

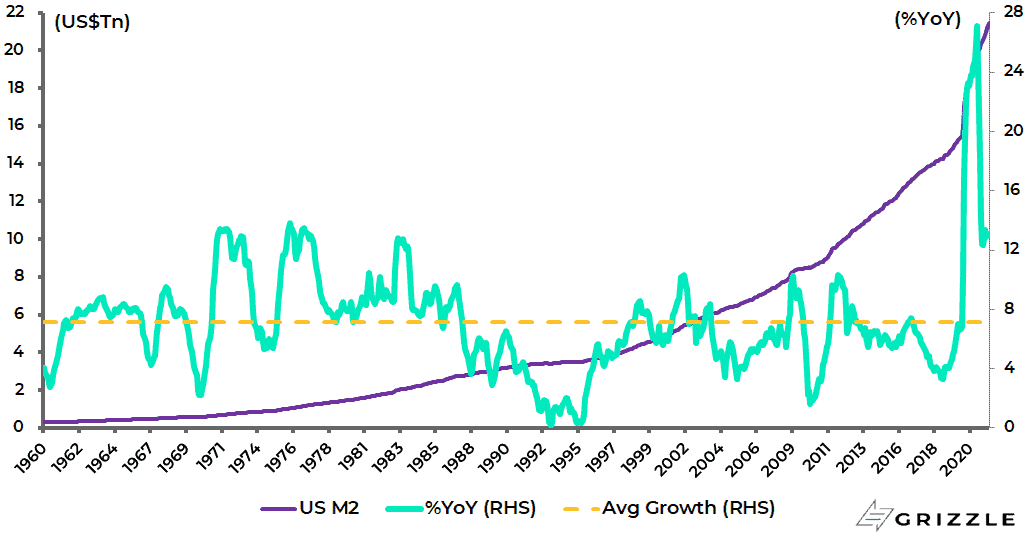

Broad money supply growth remains very high relative to history in America.

US M2 has risen by a huge 39% in the 21-month period since March 2020 and was still up 13.1% YoY in November, which is well above the average growth trend of 7.1% YoY since 1960.

US M2 trend

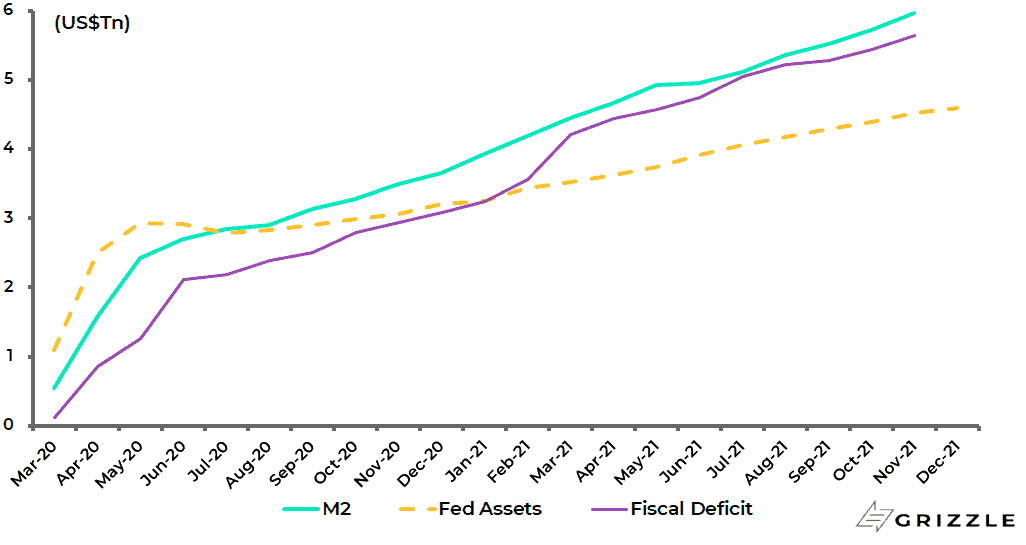

While the pandemic has made a policy of what could best be termed “MMT-lite” politically respectable in the G7 world, to the extent that central banks have funded much of the increase in fiscal deficits and will probably continue to do so.

Consider the example of America. Fiscal deficits have totaled US$5.6tn since the pandemic began in March 2020, while the Fed balance sheet and US M2 have increased by US$4.6tn and US$6tn respectively over the same period.

US cumulative fiscal deficits and increase in Fed assets and M2 since March 2020

A New ETF With a Unique Strategy for Disruption

The above outlook means that growth stocks can get a bid again in coming months, if inflationary concerns ease somewhat, but the markets will remain nervous about the monetary tightening outlook.

This is why the strategy of the recently launched Grizzle Growth ETF (GRZZ)* makes sense. There is no doubt that the spectacular commercial success of the ARK Innovation ETF has served to popularize the disruption theme.

There is also no doubt that network effects and so-called S-curve adoption patterns can create amazing “winner takes all” investment success stories when a sector is disrupted by the arrival of digitalization.

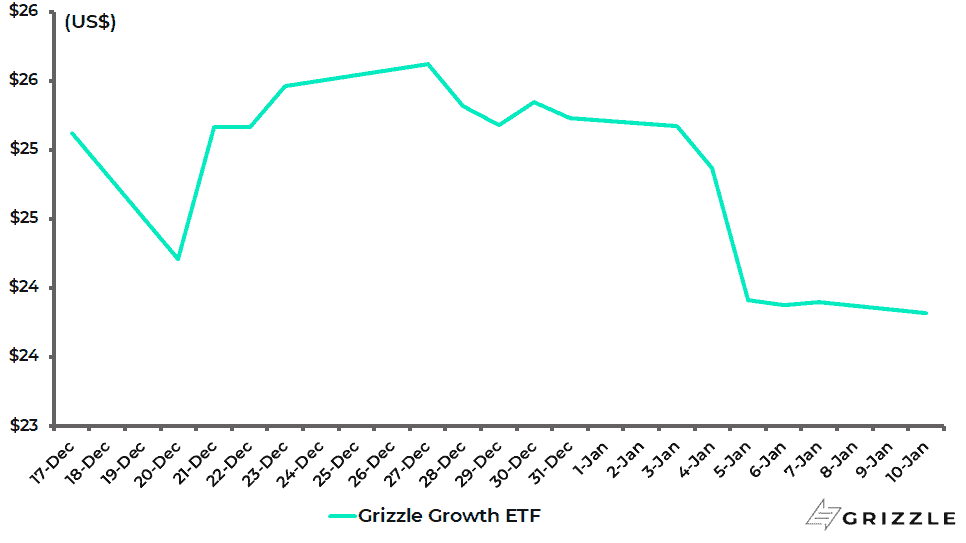

Grizzle Growth ETF

Still, the issue is what price does an investor wants to pay for disruption.

This is because many companies claiming to be disruptive can take a long time before they make money.

This is why the strategy of the Grizzle Growth ETF is to focus on disruptive growth at a reasonable price, and not just at any price.

As a result, the ETF has a strong focus on companies with cash flow generation on a 4-6 year time horizon versus speculative themes like space travel with a 10+ year time horizon.

This strategy is reflected in an aggregate valuation at launch on 17 December of the 58 stocks in the ETF at 3.4x price to sales.

Naturally, it has always made fundamental sense for equity investors to focus on cash flow.

Meanwhile, the Grizzle ETF is timely because it is clear that the profitless tech thematic, which has been so powerful a theme in the Covid-triggered retail-driven stock market rally off the March 2020 lows, is potentially extremely vulnerable in a Fed tightening cycle as recent market action has begun to indicate.

That said, digital disruption is a real phenomenon.

It is also the case that this writer remains skeptical as to whether real monetary tightening is really going to happen, as opposed to what could be best described as token tightening.

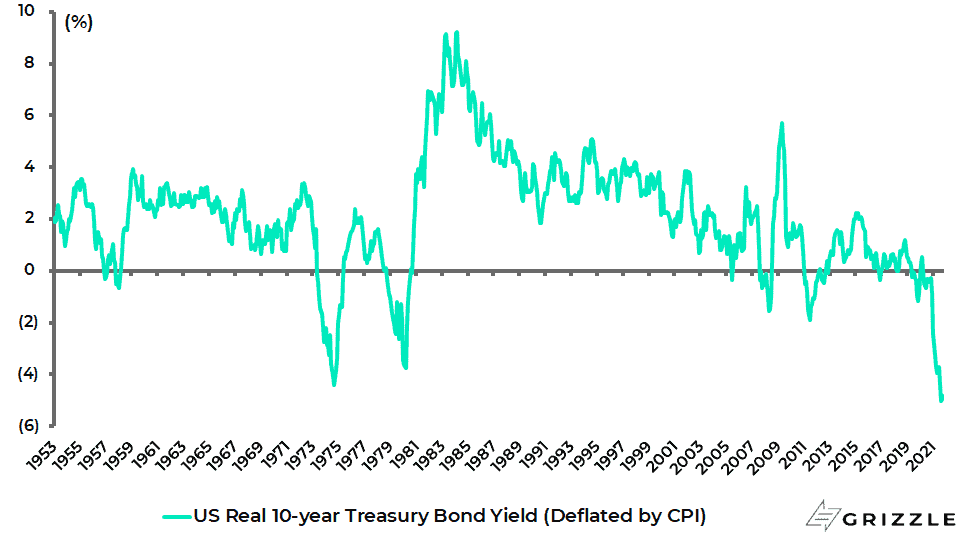

The reality is that 2021 ended with the most negative interest rates in America in more than a generation.

US real 10-yaer Treasury bond yield, deflated by CPI, declined to a negative 5.0% in December, the lowest level since at least the 1950s, and is now a negative 4.8%

US real 10-year Treasury bond yield (deflated by CPI)

That suggests that in many respects investors are already living in a world of financial repression which means that equities have to continue to be favoured over government bonds.

That said, with reported US CPI inflation so high and with opinion polls last month showing that only 28% of Americans approved of Joe Biden’s handling of inflation, the recently re-appointed Powell has to be seen to be doing something about inflation.

For to have stuck with the “transitory” line of argument would have risked his rhetoric turning into self-parody.

*The Grizzle Growth ETF is managed by Grizzle Investment Management LLC, a subsidiary of Grizzle.

The views expressed in Chris Wood’s column on Grizzle reflect Chris Wood’s personal opinion only, and they have not been reviewed or endorsed by Jefferies. The information in the column has not been reviewed or verified by Jefferies. None of Jefferies, its affiliates or employees, directors or officers shall have any liability whatsoever in connection with the content published on this website.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.