https://youtu.be/0La2lH3zYCM

The Corporate Cannabis Field of Dreams

In 2017 Canada was ground zero for the world’s next big investment trend — legal recreational cannabis.

“Corporate cannabis” was sold to retail investors as the opportunity of a lifetime.

A way to tap into a multi-billion dollar market going legal for the first time.

Literally overnight an entirely new consumer category was created and the industry raised billions from investors to fund the rapid build-out of indoor and greenhouse cannabis cultivation facilities.

The irony was that cannabis was the only consumer sector where the vast majority of the management teams and bank analysts had no real connection to the product being sold.

Boomers in suits who didn’t smoke pot selling “alternative realities” to investors who didn’t smoke pot — a comical set up at best.

The absurdity was highlighted in-depth nearly 2 years ago by Grizzle (“Up in Smoke: The Overvalued Haze of Marijuana Stocks“, Feb. 4, 2018).

The industry now finds itself in a crisis of its own making.

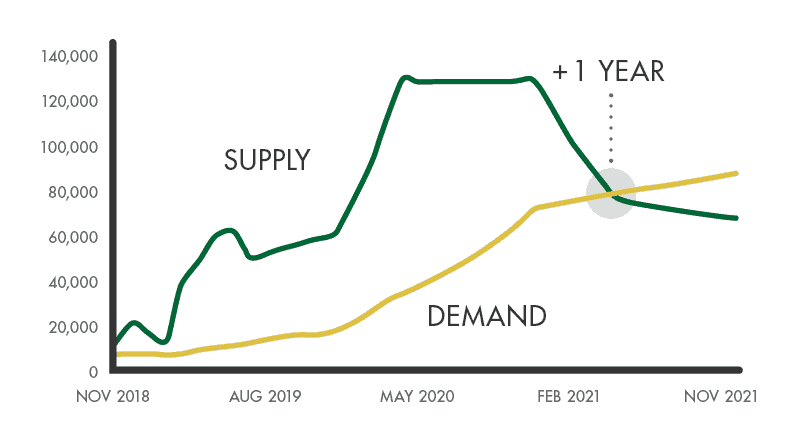

Fast forward to 2019, and the industry is staring at an oversupply of cannabis in excess of 5x legal demand, a lack of access to capital and stock prices down 50% or more.

Now the industry is flooded with cannabis, and prices, profits, and stock prices are set for more rough times in 2020 if the market can’t find a balance.

In this report, we analyze if the rollout of new cannabis products in 2020 will rescue the industry from the problems of its own making.

The Promise of Cannabis 2.0

Current consensus assumes the roll-out of vapes, edibles, drinks, and topicals will save the industry.

Investors believe that with new in-demand products to buy, consumers will ramp up their spending, translating into higher sales and better margins for every pot stock in the industry.

[su_panel background=”#C6E1FF” color=”#110076″ border=”px none ” shadow=”px px px ” radius=”4″ text_align=”center” class=”dw-editor-note”]The thought process goes: if consumers can access the products they really want, they will happily shell out $50/gram for a vape pen instead of $10/gram for flower. As a result profit margins across the industry are going to get much, much better.[/su_panel]This argument is sound, considering edibles and vape pens in the U.S. sell for two to four times more per gram of THC than flower.

Economics of a Vape Pen vs Edibles vs Flower

| Per Gram of THC | Flower | Vape Pen | Edible |

| Wholesale Revenue/Gram | $4.73 | $39.08 | $94.60 |

| Gross Margin | 48% | 43% | 58% |

The other promise of Cannabis 2.0 is to finally provide the products consumers want.

Canadians have been stuck choosing between flower and diluted cannabis oil, but now will finally have access to vape pens, edibles, and other more discreet ways to consume cannabis.

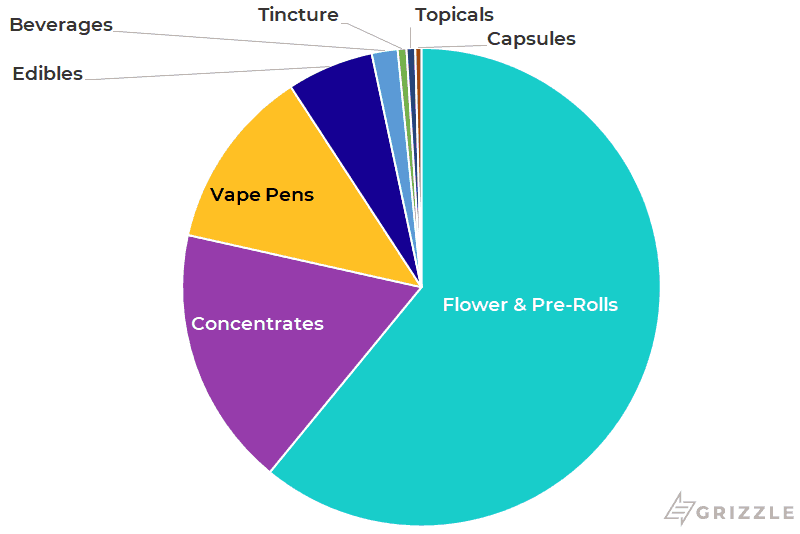

Vape pens and edibles make up close to 50% of sales in other legal markets so the argument can be made that legal sales and volumes could double in Canada once these products are released.

Market Share of Different Formats in the U.S.

The Reality of Cannabis 2.0

Demand is driven by consumers’ budgets and we think consumers generally have a financial limit for vices (alcohol, cigarettes, gambling, cannabis).

Consumers won’t buy more or pay a higher price just because new products are available.

[su_panel background=”#C6E1FF” color=”#110076″ border=”px none ” shadow=”px px px ” radius=”4″ text_align=”center” class=”dw-editor-note”]Realistically, the right way to look at demand growth from 2.0 products is to estimate how much more of a cannabis consumer’s budget can be converted from the black market to the legal market.[/su_panel]From a demand perspective, one of two scenarios must come true to re-balance a severely oversupplied market.

First, we estimate the probability of scenario 1 coming true.

Scenario 1: Will Cannabis 2.0 Spur Enough New Demand?

Our research tells us the simple answer is no, but the longer answer is, it depends on the quality of the weed.

Though the total amount of cannabis coming out of greenhouses will be way too much for the domestic legal market to absorb, even with much higher spending, there will be brands that still do well.

[su_panel background=”#C6E1FF” color=”#110076″ border=”px none ” shadow=”px px px ” radius=”4″ text_align=”center” class=”dw-editor-note”]The market has way too much low quality ‘ditch’ weed, but is more balanced when it comes to supply and demand for premium products.[/su_panel]There will be in-demand producers who have little trouble finding consumers even while the industry as a whole struggles with a glut of low-grade cannabis.

Pricing should hold up better for premium products compared to ditch weed, however everyone will still have to live with falling prices as the industry finds a balance.

It’s All About Per Capita Spending

The reason it’s so unlikely demand increases enough to meet supply in 2020 all comes down to consumers’ willingness to spend on cannabis.

As it stands today, Canadians spend less on legal cannabis than any other market in North America.

[su_panel background=”#C6E1FF” color=”#110076″ border=”px none ” shadow=”px px px ” radius=”4″ text_align=”center” class=”dw-editor-note”]Per capita cannabis spending is only $25/yr in Canada compared to $150 and up in legal U.S. states. This doesn’t mean Canadians smoke less, it means the rest of their spending is in the black market.[/su_panel]

Canada’s lack of legal spending is a huge opportunity for licensed producers.

If they can provide the price points and products people want, consumers will open up their wallets.

But what matters to cannabis investors, is how quickly consumers will ramp up purchases in the legal market.

The rollout of new products will be one catalyst, but just as important is the rollout of retail stores.

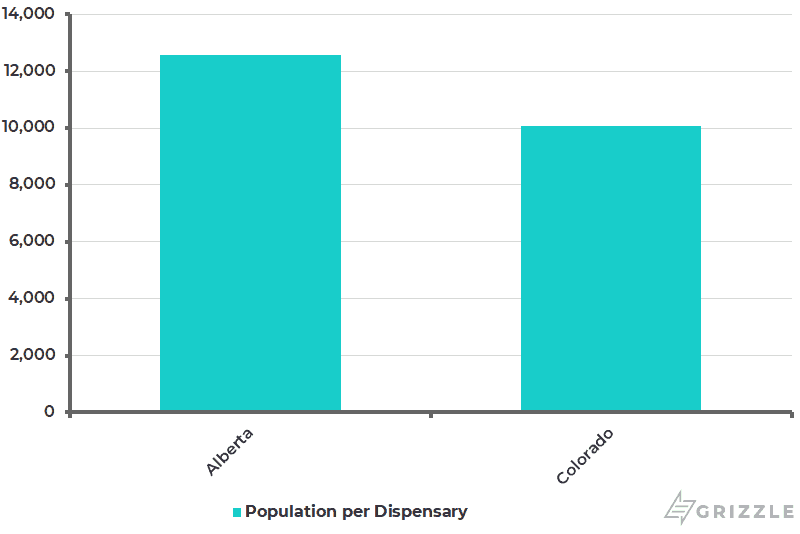

So we went looking for the province with the most advanced retail footprint and ended up in good old Alberta.

Alberta is the poster child for a successful rollout of retail stores.

Alberta is so far along in its retail rollout that the number of customers per store is only 25% higher than mature markets in the United States.

This means Alberta should have enough stores to adequately service the population sometime in the first half of next year.

Alberta Almost Has Enough Retail Stores

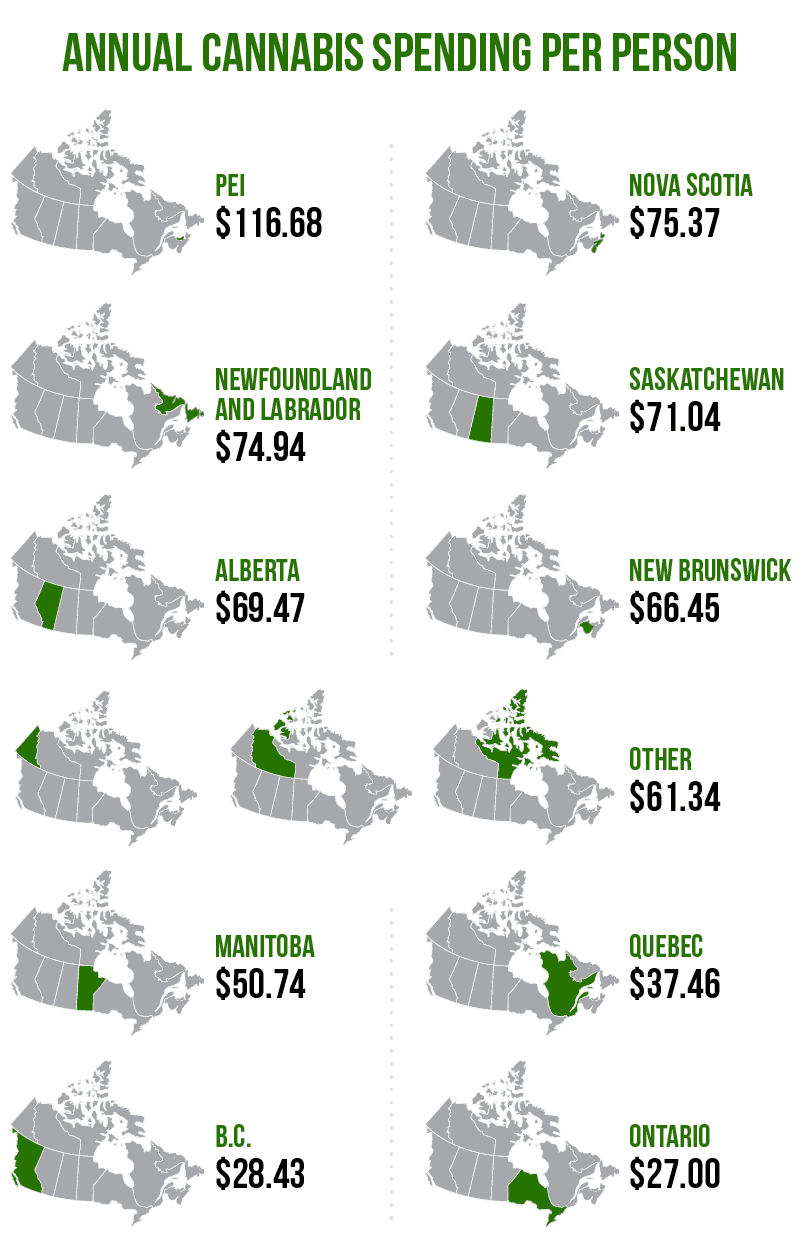

Albertans spend $68/yr on cannabis, 70% more than the average Canadian, largely due to an orderly rollout of private retail dispensaries, now numbering 348.

Even still, per capita spending of $68 in August only fell in line with California, a struggling legal market, telling us Canada still has a lot of work to do to stoke demand.

[su_panel background=”#C6E1FF” color=”#110076″ border=”px none ” shadow=”px px px ” radius=”4″ text_align=”center” class=”dw-editor-note”]Investors blame the slow retail store rollout as the reason for cannabis company woes, but our analysis shows even if every province approaches the stores per person of a mature market like Colorado, the August harvest would still exceed best-case demand by 20%. [/su_panel]We used Alberta as a starting point to estimate the increase in 2020 per capita spending.

To avoid being called too pessimistic we looked at what demand will be in 2020 if consumers go from spending only $25/yr on cannabis to $140/yr in 2020, a 460% increase.

We basically took Alberta’s peak spending rate from August, doubled it, and assumed every Canadian started spending like an Albertan.

This is an optimistic scenario for sure

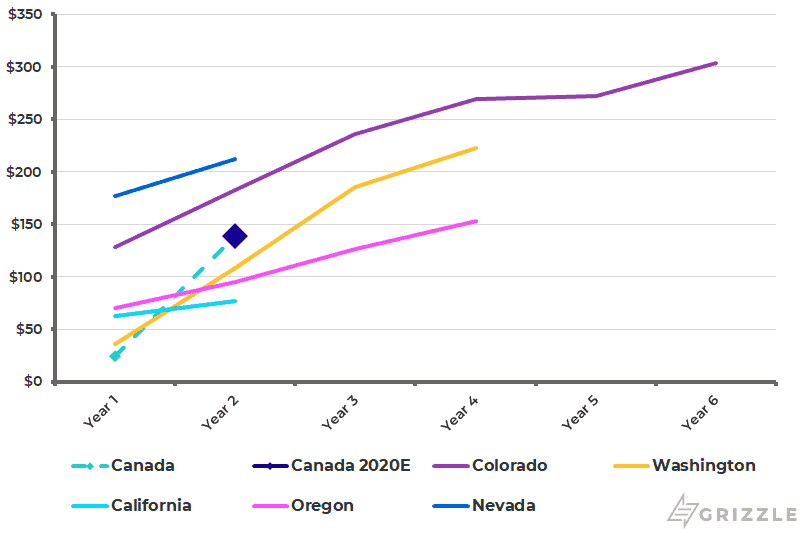

Grizzle 2020 Per Capita Spending Estimate vs U.S. States

In a rosy scenario, legal sales of cannabis rise to $5.2 billion, up 250% from September’s run rate of $1.5 billion and 450% from the 2019 average so far.

For some perspective, the average U.S. state increased per capita spending by 60% in the second year of legalization with a high of 200% in Washington.

In Canada, per capita spending would have to increase 450% just to meet the level of supply from August 2019.

Betting that per capita spending will increase 2x-6x faster in Canada, is a foolish and unlikely bet to make in our view, especially considering Canada had stricter rules around marketing and a slower rollout of retail stores and new products.

Simplistically assuming the average gram continues to go for about $10, Canadians will be buying 540,000 kg in 2020, up from 176,000 kg today, a big increase but still below August’s harvest run-rate of 643,000 kg.

Volume Demand Forecast In 2020

| September 2019 | 2020 Forecast | |

| Canada Population (million) | 37.59 | 37.59 |

| Annual Cannabis Spending per person | $41 | $139 |

| Sales (million) | $1,529 | $5,125 |

| Retail $/gram | $10.00 | $10.00 |

| Max Rec Demand (kg) | 151,494 | 512,529 |

| (+) Medical Demand (kg) | 25,115 | 25,115 |

| (=) Total Demand (kg) | 176,609 | 537,644 |

*Numbers May Not Add Due to Rounding

Even though consumers could be buying 3 times more cannabis, the current harvest capacity in Canada is far higher.

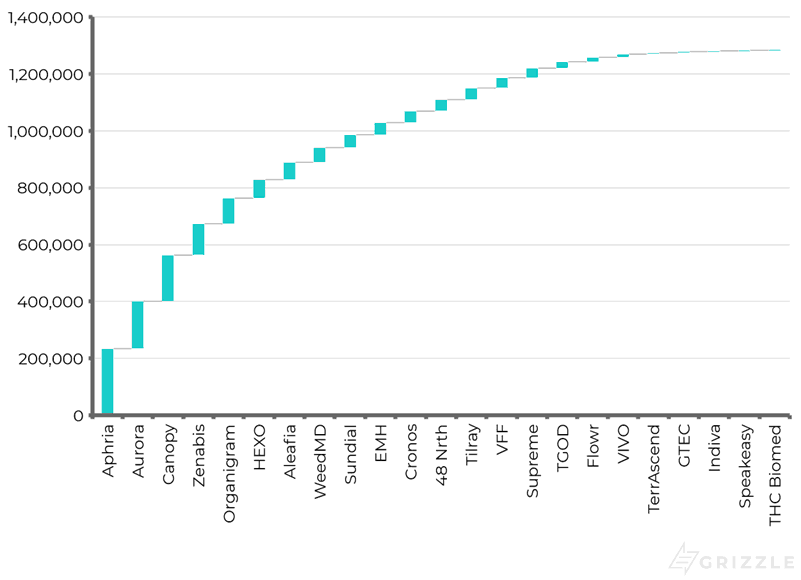

The top 22 license holders together have greenhouses up and running that can pump out 1.3 million kg a year and more capacity is coming.

Current Growing Capacity by Operator

In the bullish scenario, we’ve outlined above, 2020 demand will still be far below the industry’s growing capacity.

[su_panel background=”#C6E1FF” color=”#110076″ border=”px none ” shadow=”px px px ” radius=”4″ text_align=”center” class=”dw-editor-note”]We think it’s safe to say legal cannabis prices will continue to fall in 2020 as producers drop prices and fight among themselves to be the gram that ends up in consumers’ shopping carts.[/su_panel]Cannabis Supply vs Demand Forecast

What About Increased Demand from Cannabis 2.0?

So we know cannabis demand next year is unlikely to match supply from a volume perspective, but what about if new products can juice industry margins.

Could sales of higher-margin vape carts, edibles, and topicals improve margins enough that producers can survive by simply selling more expensive cannabis instead of more cannabis?

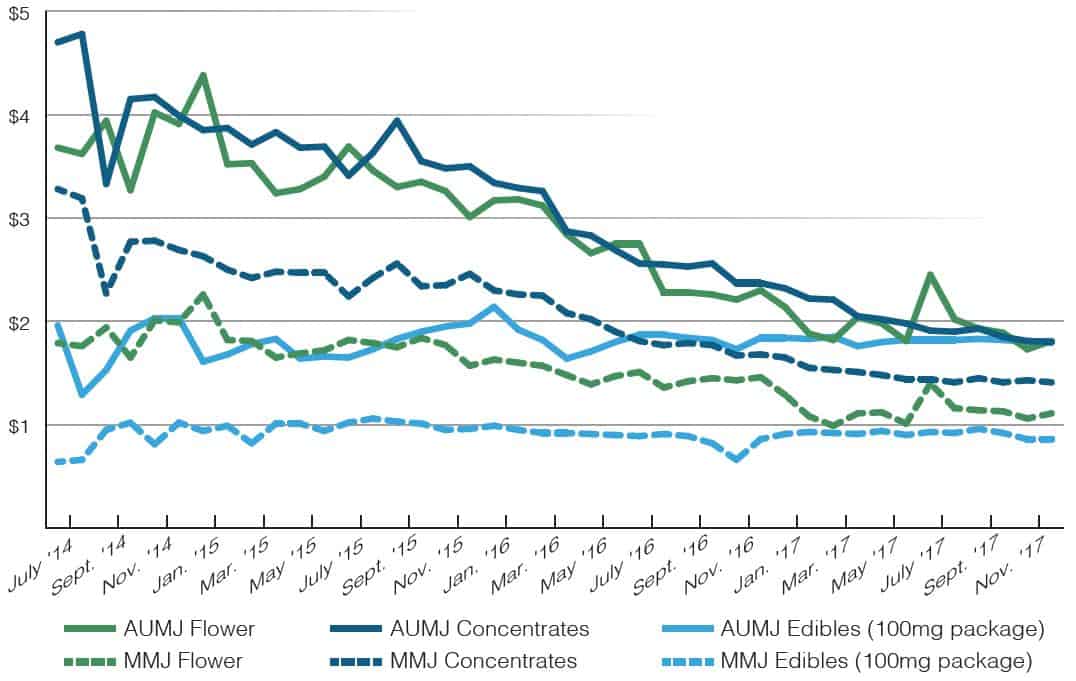

Looking at the effect vapes and edibles had on U.S. profitability we have to say no.

In every state where adequate sales and volume data were available, we found the same trend.

Even though vape pens and edibles started with higher margins, rapid industry-wide price cuts caused the revenue per gram of the industry to fall regardless.

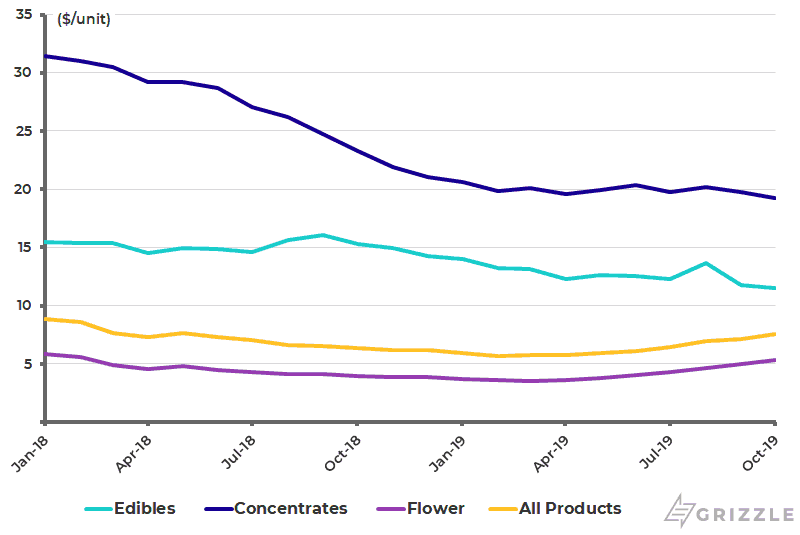

More Expensive Cannabis Products Don’t Lead to Higher Industry Margins

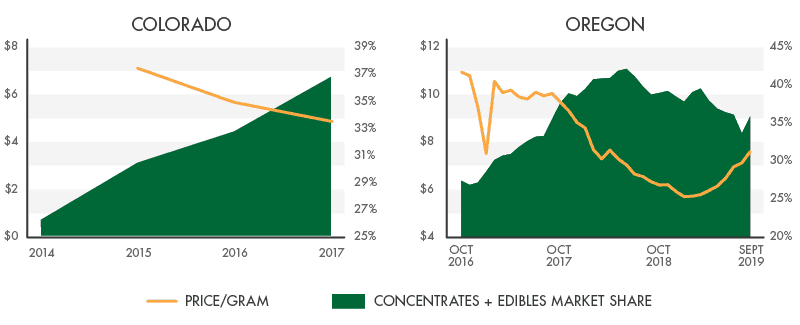

A steep decline in flower prices had an impact, but prices for vape pens fell significantly as well.

In Colorado, concentrate prices fell more than 50% in the three years after legalization as potency increased at the same time the overall price of the product declined, a gut punch to revenue.

Price Per Serving of THC in Colorado

The data above only goes through 2017, but since that time we are also seeing a fall in edible prices as competition and consumer knowledge increases.

Even Edible Prices Are Now Falling in the U.S. (Oregon)

Overall, we expect an oversupply of flower to negatively impact pricing for all cannabis products.

The industry won’t be able to rely on more expensive products to save profit margins.

Some Hard Decisions Need to Be Made

We’ve shown that a massive increase in spending from consumers won’t be enough to balance the market next year.

If we are right, there are only two ways the industry can re-balance:

- Industry conditions will cause enough growers to go bankrupt to take the excess supply out of the market.

- Companies must cut costs to match revenues that are turning out to be far lower than the industry expected.

We’ve seen some cost-cutting from companies facing the worst of the industry cash crunch, but there are still dozens making a risky bet that they can double or triple sales and keep pricing relatively flat.

From all of our research, either volumes or prices have to give, in an oversupplied market you can’t have both.

Cutting costs would be a smart move to ensure survival, but we just don’t see any management teams willing to admit growth just isn’t there.

They would rather throw a Hail Mary and hope they can keep borrowing until sales catch up to the corporate overhead.

Given that management teams don’t seem to want to make the hard decisions, we think the market will decide for them.

[su_panel background=”#C6E1FF” color=”#110076″ border=”px none ” shadow=”px px px ” radius=”4″ text_align=”center” class=”dw-editor-note”]Financial distress will be a continuing theme in 2020 and we believe will ultimately lead to falling supply and potentially a balanced market in 2021. [/su_panel]

A Look at Supply: Why Not Just Cut the Harvest?

In the cannabis industry supply equals revenue.

If a grower cuts their harvest, they are also guaranteeing to see less revenue.

In an industry where almost every company is losing money and running out of cash, growers are desperate to bring in more revenue even if it only makes the oversupply worse.

Yes, the industry would be better off if supply was cut across the board, but who decides which company’s cut and by how much?

The best the industry can hope for without bankruptcies is slowing growth in greenhouses and output.

A fall in supply is simply out of the question unless companies go away.

Even though some growers like Aurora Cannabis and Canopy Growth are already selling off or mothballing greenhouses, it’s far from enough.

For one, supply among the top 22 licensed producers we track is running at 1.3 million kg’s a year with more growth planned for next year.

The current harvest exceeds demand by 5x and we expect will continue to exceed demand by at least 2x next year.

2020 will be another year of re-balancing, but no industry ever stands still so we will see continued growth in demand and an eventual fall in supply.

A healthy market environment is on the horizon, but it will take time to get there, likely in 2021.

Supply vs Demand Forecast

Strategies to Navigate This Market

There are two strategies we would recommend to navigate potstocks in 2020.

- Short or avoid the ditch weed companies running out of cash.

- Tactically gain exposure to companies growing premium cannabis or those who produce mid-grade at cheapest growing costs. These players will be best positioned once the market re-balances.

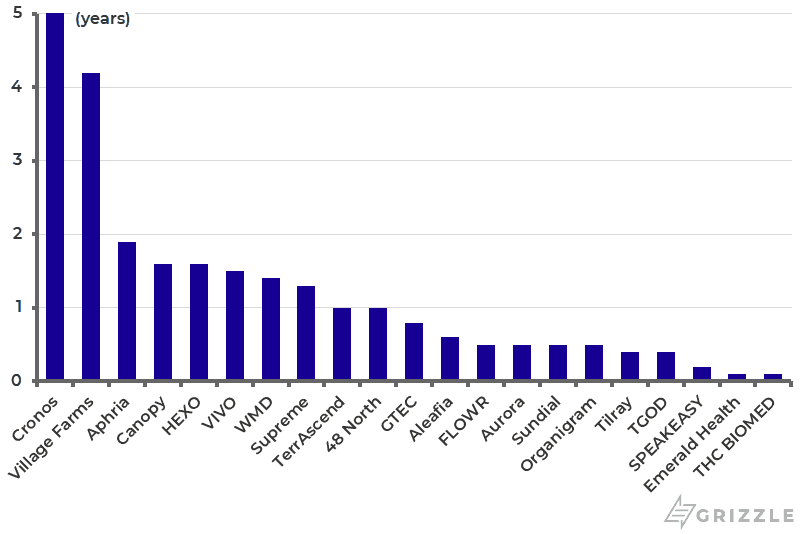

Cash is king in high growth, cash burning industries like cannabis. Those without it won’t be around long enough to see the market turn, regardless of how solid the management team, cultivation expertise or assets turn out to be.

We’ve compiled this list of liquidity so you can see how many years of cash the 22 companies we track have left.

Keep in mind we exclude cash spent on mergers because a company could easily stop doing deals if cash got tight.

However, if a company is particularly deal-hungry they may run out of cash even sooner than our table projects.

Months of Cash Left as of Latest Filing Date

With a difficult 2020 ahead for the sector, investing tactically is critical.

For those who are looking to buy in ahead of a potential rebound in 2021, the focus must be on companies who can either grow premium cannabis or grow mid-grade cannabis at a low-cost.

Everyone else is about to get squeezed.

Premium producers are the only ones building real brand value in the market right now, producing high-quality flower that consumers demand.

In our poll on Twitter (536 votes), Broken Coast (owned by Aphria) was chosen as the best “quality” recreational brand in Canada with 56% of votes, followed by 7 Acres (owned by Supreme) with 28%.

Broad question for the cannabis twitter: Among the LPs available NATIONALLY, who would you pick as the best "quality" brand in Canada?

Obviously not an exhaustive list, please add brands I haven't included (and I'll tally the likes from that). Please retweet 🙏🏾 #potstocks

— Thomas George (@thomasg_grizzle) December 7, 2019

Other notable rec brands available nationally were San Rafeal (Aurora) and Color (WeedMD).

The Lift & Co Canadian Cannabis Awards also provides a good overview of high-quality producers in the market.

- Brand of the Year: 7Acres

- Top Master Grower: Broken Coast

- Top Hybrid Flower: Broken Coast

- Top Sativa Flower: San Rafael

- Top Indica: San Rafael

A Sample of the Award Winning and Most Popular Strains LINK

We also reached out to WhatsMyPot, a respected and prolific reviewer of cannabis strains on Twitter. Their top brands for quality and value are Color and Redecan.

Long View: There is a Real Industry Here

There is a legitimate consumer category in legal recreational cannabis, however, it will be driven by actual growers and consumers of the product — not the present characters in the capital markets carnival sideshow.

It’s going to be a choppy 2020, a year of consolidation and bankruptcy, but this is what needs to happen to balance out this bubble ditch weed market.

Tens of billions are already spent in the black market for cannabis, quality product at competitive prices is what it will take to bring those consumers to the legal market.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.