What is the Cannabis Scorecard?

The Cannabis Scorecard is a comprehensive tool for investors to judge which Canadian companies are best and worst positioned to capitalize on the recent legalization of cannabis.

A regularly updated scorecard for the quickly expanding list of U.S. operators is also available.

The scorecard is full of important charts and metrics, providing you with a quick way to judge which companies may be worth an investment and which are better left alone or shorted.

Revenue

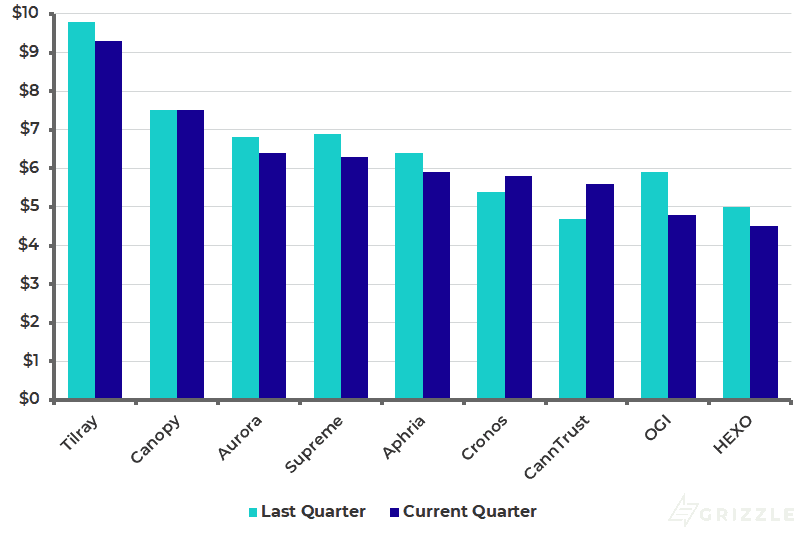

Revenue per gram may seem straightforward, but look a little closer and it can give us some useful information about the pricing strategy of each company.

Does management want to be the premium product in the market, the value brand or something in between?

When supply and demand are balanced a company’s market share often determines what pricing they can get away with. The higher the market share, the higher the price.

We would not put too much stock in current pricing as the market is so new; these companies don’t yet know what consumers are willing to pay.

Companies basically made up prices and submitted them to the government distributor, but are just starting to adjust product pricing based on consumer behaviour.

At this early stage, Aurora, Canopy Growth, Supreme, and Tilray look to be playing for the premium segment while OGI, HEXO, and CannTrust are trying to offer more value to drive higher sales.

[su_panel background=”#C6E1FF” color=”#110076″ border=”px none ” shadow=”px px px ” radius=”4″ text_align=”center” class=”dw-editor-note”]Almost all the companies saw pricing fall in the first quarter of 2019 which likely signals the companies are adjusting to the data coming in from consumers on what they are willing to pay. The companies are still trying to figure out how much of a premium consumers are willing to pay to guarantee the cannabis is free of pesticides and solvents and legally grown. [/su_panel]Selling Price per Gram Equivalent

Growing Costs

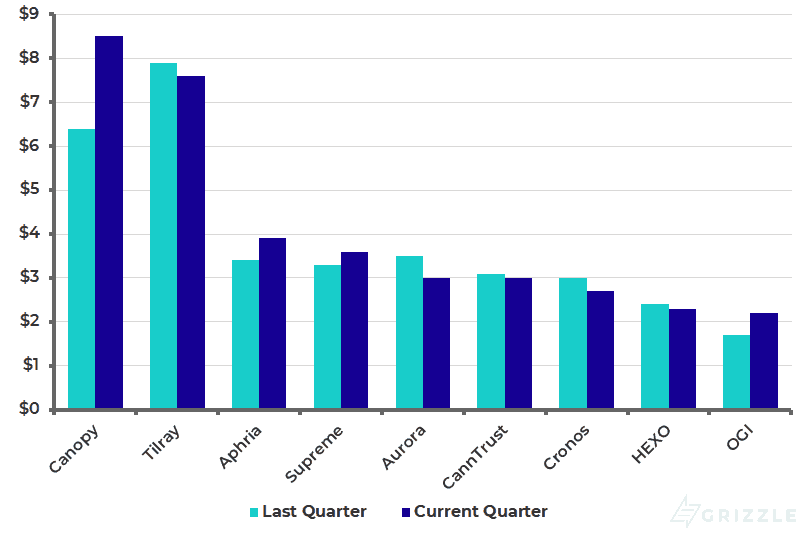

The next piece of the puzzle is growing costs.

Producers are all ramping up capacity to bring down their growing costs to ensure they generate attractive profits even when the government is paying less than producers were used to with their medical clients.

In general, the lower your growing costs the more cash you generate at the end of the day.

These companies are still scaling and have promised sub $1/gram growing costs so expect production costs to continue falling in coming quarters.

Aurora and Aphria are doing a good job managing costs considering they plan to be a top-three grower by volume and are investing lots of money upfront to build enough greenhouse space.

Aphria, in particular, should see rapidly falling growing costs as it ramps up cultivation in its first large greenhouse and is approved to cultivate in the massive Aphria Diamond facility in the next few months.

Canopy continues to struggle with costs due to crop write-offs and growing space sitting idle from logistical issues. Canopy has a long way to go to be competitive with peers.

Tilray is buying supply from peers, explaining the high production cost per gram making Canopy’s numbers look even worse considering Canopy produces a majority of supply in-house.

Production Costs per Gram Equivalent

Gross Margin

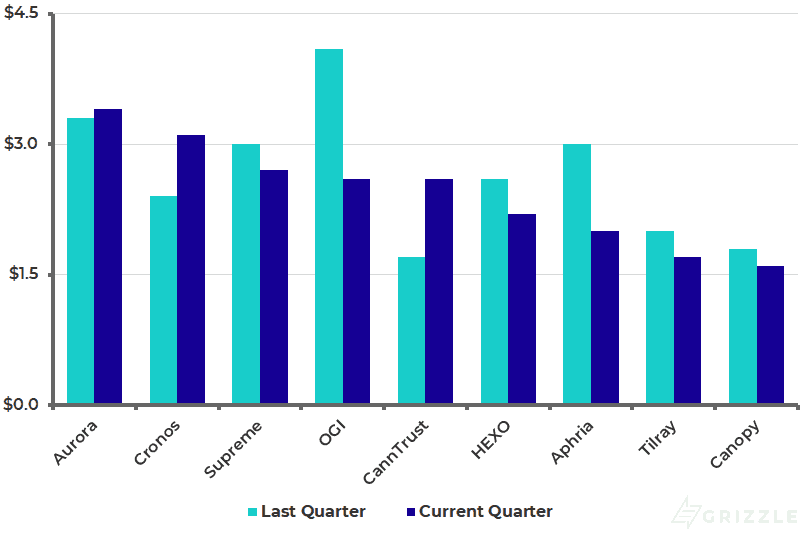

A wrinkle in our statement that lower costs equal higher profits is the fact that more profitable products like cannabis oils and pills are also more expensive to produce.

Just because a company is high up on the cost scale doesn’t necessarily mean they are less profitable than peers.

That is why gross margin is the only number we care about.

[su_panel background=”#C6E1FF” color=”#110076″ border=”px none ” shadow=”px px px ” radius=”4″ text_align=”center” class=”dw-editor-note”]Gross margin is a true comparison of which grower runs the most profitable greenhouses. It takes into account the price, product mix, and cost of what a grower sells.[/su_panel]Canopy Growth sells cannabis for $2.70 more per gram than Organigram, but because Canopy has much higher growing costs, Organigram actually generates $1.00 more margin per gram than Canopy.

This is the power of low production costs. Aurora, Cronos, Supreme, and Organigram have the best gross margins and can undercut competitors to win over more customers while still generating a similar level of profitability.

Gross Margin Per Gram

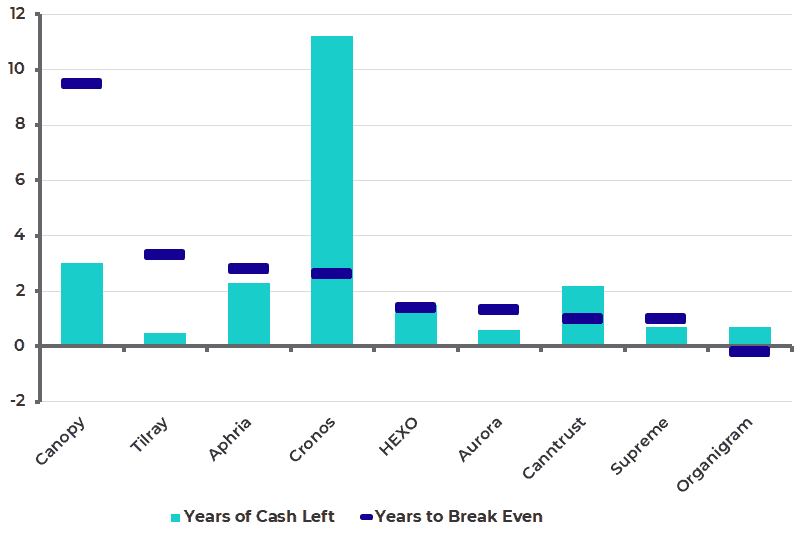

Cash is King: Years to Break-Even vs Years of Cash Left

Investors often forget the importance of cash when they are investing in a high growth industry.

Even though licensed producers are seeing rapid revenue growth, they are far from profitable and still need to spend millions to expand capacity to meet demand. Cash is king.

The chart below looks at each company’s cash balance in the latest quarter and their cash burn from operations plus their spending on construction of new greenhouses.

We exclude cash spent on investments because these can be cut back if the company faces a cash crunch.

[su_panel background=”#150093″ color=”#ffffff” border=”0px solid #cccccc”]Cannabis stocks have continually raised more money from the market so use this chart as an indication of who will be issuing more stock or debt, not an indicator of who may go bankrupt.[/su_panel]Cronos is likely going to buy something in the U.S. or Europe as they have way too much cash just to fund operations.

Canopy actually needs the cash they have just to fund the massive cash burn, but the company has been very aggressive in the past and could spend the money faster buying up additional assets.

Aphria, Tilray, TGOD, and HEXO have adequate cash to potentially make it until they turn a profit in 2020.

CannTrust just did a big capital raise but the recent Health Canada violations may mean the money gets clawed back in lawsuits. We recommend staying away from that stock until there is more clarity on the situation.

The rest of the companies will likely need to raise cash in 2019 or early 2020.

Years of Cash Left at This Quarter’s Spending Rate

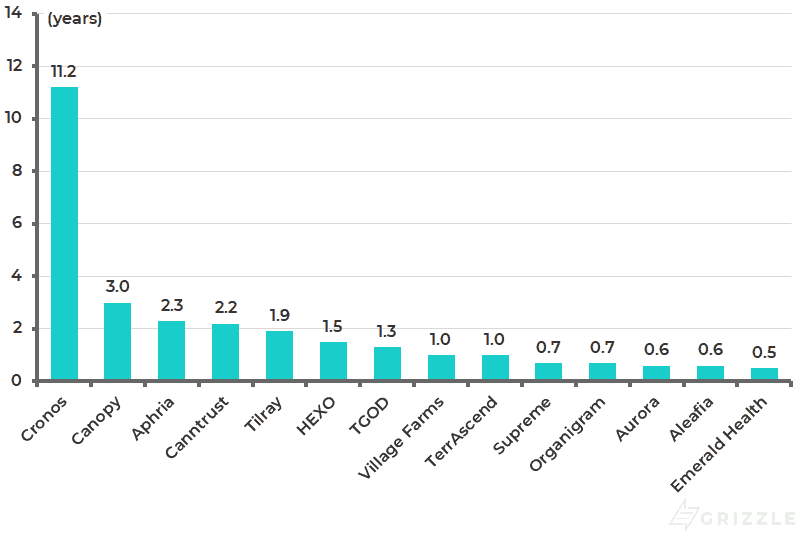

At the end of the day, we want to know which company can turn a profit before their cash runs out.

Even the most profitable business model is worthless if the company runs out of cash before they can get up and running.

The most attractive cannabis stock is the one with more than enough cash to carry the company to profitability.

Unfortunately, there are not many cannabis stocks that fit the bill.

For example, Organigram was profitable last quarter selling 20,000 kg annually and no longer has to worry about running out of cash.

Contrast Organigram with Canopy Growth. Even if annual sales double this year it will be 9.5 years until the company can cover its operating costs, far longer than the three years of cash Canopy has left.

Companies without enough cash to carry them to profitability will at the very least have to issue more shares, which would pressure the stock price and at worst could run into liquidity issues during a market downturn that would crater the stock.

[su_panel background=”#C6E1FF” color=”#110076″ border=”px none ” shadow=”px px px ” radius=”4″ text_align=”center” class=”dw-editor-note”]This analysis assumes legal sales double from the current quarterly run rate due to the rollout of edibles, vape pens, and topicals. Current sales are flat or falling for most producers so the years to breakeven could easily be much higher! Unfortunately for investors, this chart is somewhat of a best-case scenario.[/su_panel]For more details on how we calculated the years to breakeven see the bottom of the report.

Years Until Break-Even vs Years of Cash Left

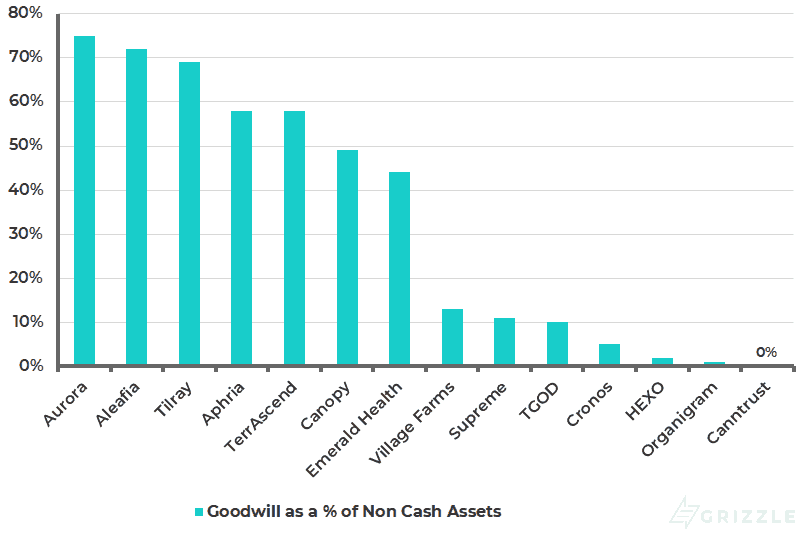

Judging the Risk of Asset Writedowns

Pot stocks have spent millions on acquisitions in the past two years. As usual, acquisitions in fast-growing and potentially overhyped sectors lead to large amounts of goodwill.

Goodwill is created when company A pays $100 for company B yet company B only owns assets worth $60 on the balance sheet. The additional $40 becomes goodwill on company A’s balance sheet.

[su_panel background=”#C6E1FF” color=”#110076″ border=”px none ” shadow=”px px px ” radius=”4″ text_align=”center” class=”dw-editor-note”]The simple way to think about goodwill is the more of it a company has, the higher the risk of a write-off down the road.[/su_panel]Management needs to show more cashflow growth the more goodwill they have on the balance sheet to avoid a costly write-off down the road.

The company’s accounting firm values the goodwill using a forecast of cashflows. If the future cashflow is not high enough auditors will make management write off some of the goodwill, making earnings look worse and demonstrating management is not investing shareholder money wisely.

The cannabis companies doing the most deals have the most goodwill all else equal.

We are confident writedowns are coming for Canopy Growth while the rest of the companies with lots of goodwill must show growing revenue and cash flow soon or they are at risk of writedowns as well.

Goodwill as a % of Non-Cash Assets (Lower is Better)

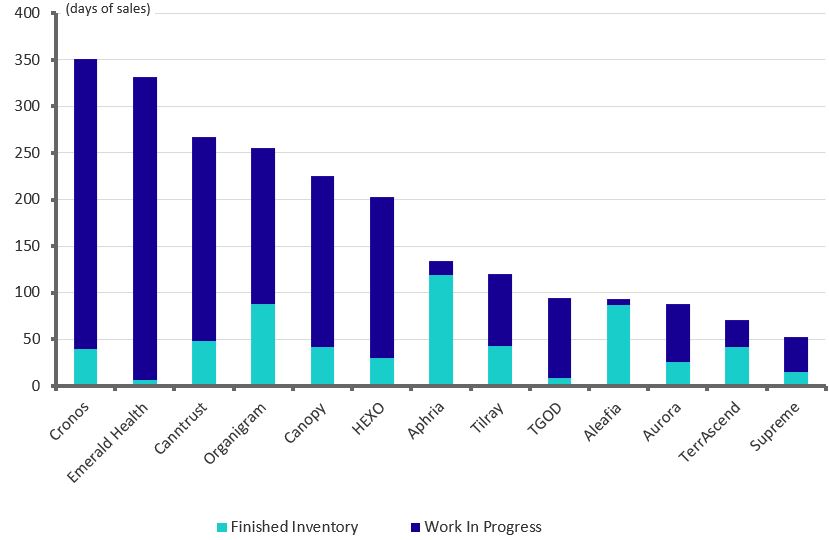

Inventories

Investors and the media continue to argue about whether there is a supply shortage or not. Grizzle thinks the data conclusively shows the problem is not with supply but demand.

There is too much low-quality, high-priced flower floating around that consumers don’t want to buy.

[su_panel background=”#C6E1FF” color=”#110076″ border=”px none ” shadow=”px px px ” radius=”4″ text_align=”center” class=”dw-editor-note”]We estimate the fourteen largest license holders have 124,000 kg of finished and in-process inventory on hand compared to countrywide sales that are running at 121,000 kg a year — more than enough.[/su_panel]It looks to us like some producers have given up on selling most of their raw flower and diluted oils ahead of the legalization of edibles and are now stockpiling to turn the cannabis into oils to go into vape pens, drinks, edibles, and topicals come December 2019.

Cannabis Days of Inventory (At Last Quarters Sales Rate)

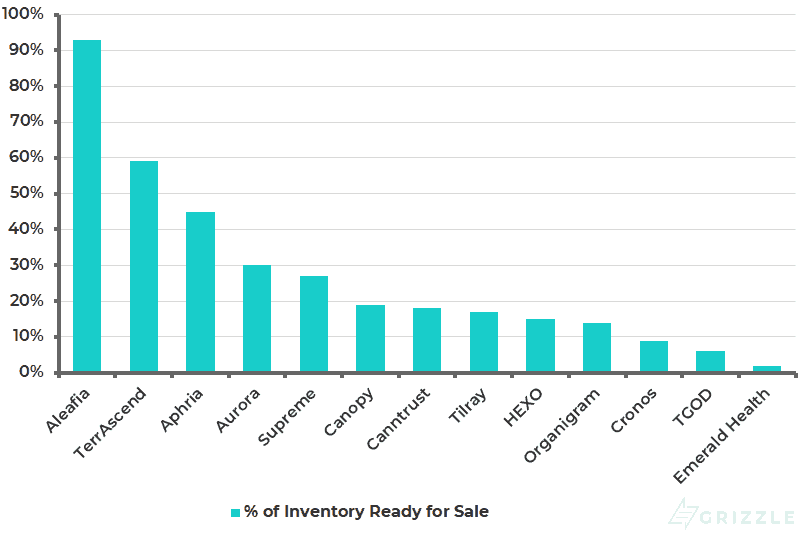

In general, the more packaged inventory you have on hand the better. A company can quickly react to positive changes in demand.

The fact that most licensed growers have less than 50% of finished inventory tells us either they are ramping up the amount of cannabis they grow rapidly (this is definitely happening) or they plan to do something else with the raw flower like turn it into concentrates.

Our gut tells us it’s a bit of both.

Percent of Inventory Finished and Ready for Sale

Sensitivity Analysis

To help investors put numbers behind the upside and downside for each licensed producer we have provided target stock prices under two different scenarios.

These are two simple starting points and are not inclusive of all possible future scenarios.

If your favourite stock screens as overvalued it means the market is expecting extra sources of revenue beyond the company’s current growing capacity, or they expect much higher selling prices and profitability from the legal market.

All these expectations could come true, but beware that by owning stocks like Canopy Growth, Cronos, or Tilray you are making a bet that the future will be even brighter than the market currently expects.

[su_panel background=”#150093″ color=”#ffffff” border=”0px solid #cccccc”]Owning stocks with potential upside means you can still make money even if cannabis runs into unforeseen challenges on the road to global legalization.[/su_panel]Scenario 1

Licensed producers reach fully funded capacity and sell their products for $5.50 per gram, which is the average wholesale price paid by government distributors. They generate a 30% EBITDA margin on sales. The market is willing to pay a 10x EBITDA multiple, in line with major beer companies like Miller Coors and Budweiser.

| Current Price (CAD) | Implied Value | Upside/ (Downside) | |

| EMH | $2.23 | $13.91 | 524% |

| TGOD | $3.21 | $12.70 | 296% |

| TRST | $4.04 | $12.02 | 198% |

| HEXO | $5.15 | $12.32 | 139% |

| VFF | $13.14 | $23.35 | 78% |

| APHA | $8.52 | $14.02 | 65% |

| OGI | $8.25 | $11.22 | 36% |

| FIRE | $1.37 | $1.74 | 27% |

| ACB | $9.37 | $8.23 | -12% |

| CRON | $19.70 | $10.55 | -46% |

| WEED | $48.45 | $25.34 | -48% |

| TLRY* | $58.75 | $28.46 | -52% |

Prices as of 7/11/2019. * TLRY price converted from USD to CAD.

Scenario 2

Licensed producers reach fully funded capacity and sell their products for $8.00 per gram due to the release of higher-margin infused drinks, edibles, beauty products, and higher-priced exports to other countries. They generate a 30% EBITDA margin on sales. The market is willing to pay a 15x EBITDA multiple, in line with major wine and spirits companies like Diageo and Constellation Brands.

| Current Price (CAD) | Implied Value | Upside/ (Downside) | |

| EMH | $2.23 | $30.30 | 1259% |

| TRST | $4.04 | $24.44 | 505% |

| TGOD | $3.21 | $18.74 | 484% |

| HEXO | $5.15 | $25.72 | 399% |

| VFF | $13.14 | $51.15 | 289% |

| APHA | $8.52 | $29.91 | 251% |

| OGI | $8.25 | $24.81 | 201% |

| FIRE | $1.37 | $3.96 | 189% |

| ACB | $9.37 | $17.92 | 91% |

| TLRY* | $58.75 | $67.26 | 14% |

| WEED | $48.45 | $46.46 | -4% |

| CRON | $19.70 | $15.00 | -24% |

Prices as of 7/11/2019. * TLRY price converted from USD to CAD.

Years to Break-even Calculation

First, we looked at each company’s total overhead costs (salaries, R&D, marketing) and divided by their gross margin (profit after direct operating costs) to arrive at the volume needed to break even.

Next, we looked at production growth last quarter, the first quarter of legal sales, and annualized it by multiplying by four.

Lastly, we took the difference between current sales and break-even sales and divided by the volume growth rate in grams to figure out how many years until each company turns a profit.

Example:

Tilray has a gross margin of $1.66/gram and total operating costs of $86.6 million, implying it needs to sell 52,195 kg a year to turn a profit.

Tilray sold 12,048 kg on an annual basis last quarter and we assume sales double, growing 12,048 kg in the next twelve months.

52,195 – 12,048 = 40,147 / 12,048 = 3.3 years to break even

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.