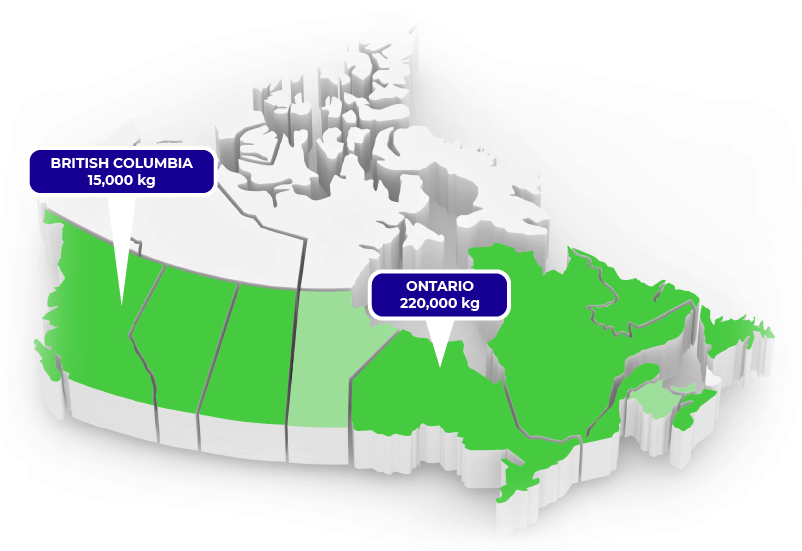

CAPACITY BY PROVINCE IN 2022

APHRIA INC.

Ticker: APH (TSX)

Stock Price (Mar 2018): $14.24

Grizzle’s Future Target Price: $8.00

Current Annual Capacity: 9,000 kg

Future Annual Capacity: 253,000 kg

Aphria is headquartered in Ontario and has plans to be the third largest player in the marijuana space. Volume growth is rapid and will make Aphria the largest producer in Canada in 2019 with 230,000 of capacity ready at the start of the year. By 2022 we expect Aphria will be the third largest producer in Canada with domestic capacity of 235,000 kg a year (23% of Canadian demand).

What is the Canapocalypse?

The wave of marijuana supply is coming. Hundreds of greenhouses are being built across Canada and as harvests begin to flood the market in 2019, the Canapocalypse (aka price collapse) will soon be upon us. Retail prices are going much much lower unless legal producers find other countries to absorb the excess supply.

In this 4-part series we take you through a full analysis of the 4 largest legal producers, explain what assets they own, the potential export opportunities, future growth potential and what the stocks are worth. After reading our report, you will be better able to navigate this exciting, but risky emerging industry.

For some background reading on the coming Canapocalypse, check out Up in Smoke, our deep dive report of the Canadian marijuana sector as well as The Marijuana Export Mirage, an in-depth analysis into global supply and demand of marijuana.

MANAGEMENT TEAM

Vic Neufeld – CEO and Chairman of the Board

Vic Neufeld is the CEO of Aphria and has a background in the vitamin business where he served as CEO of Jamieson Laboratories, one of Canada’s largest vitamin suppliers, for over 21 years. Neufeld was hired by Cole Cacciavillani, the founder of Aphria. He graduated from Western University with a degree in accounting and finance and has an MBA in accounting from the University of Windsor.

Cole Cacciavillani – Co-founder and VP Growing Operations

Cole Cacciavillani co-founded Aphria, Inc. (formerly Pure Natures Wellness Inc.) in 2013 and serves as Vice President of Growing Operations. Cacciavillani has 35 years of experience in the agricultural sector, running the family business CF Greenhouse. In April 2016 he converted all CF Greenhouse property into medical marijuana facilities through a sale to Aphria.

John Cervini – Co-founder, VP Infrastructure & Technology and Member of the Board

John Cervini comes from a long line of produce growers in Ontario. He ran Lakeside Produce in Ontario with his father and brother for many years. Cervini is experienced in hydroponic growing techniques and in the sales and distribution of produce. He is the founding chair of the Ontario Greenhouse Marketing Association.

Domestic Expansion

Aphria sales are 5,000 kg today with total production capacity of 9,000 kg. They are the fastest growing company in the industry right now and with the greenhouse from the Double Diamond JV, 231,000 kg of capacity will be ready to go by January 2019, an industry high.

Aphria is fully funded out to 2019, but a large equity raise would be required to grow beyond 2019 capacity. The market will already be oversupplied in 2019, so we do not think the economics will justify a decision to build additional greenhouses.

Major Greenhouses

Leamington Ontario

Aphria owns multiple greenhouses on one plot of land in Ontario, some currently producing and others under construction. Phase 1 and 2 are already operational, producing 9,000 kg a year. Phase 3 will add 21,000 kg in May of 2018 and Phase 4 will add another 70,000 kg starting in January 2019.

Double Diamond Joint Venture

Aphria established a JV “Growco” with greenhouse owner Double Diamond farms and owns a controlling 51% stake, but is entitled to 100% of production coming from the greenhouses. The first harvest is expected to be in January 2019. Aphria has an option to purchase another 32 acres of land right next to the current greenhouse which would add another 120,000 kg of capacity.

We don’t expect the additional 120,000 kg of capacity to be built unless management does another large equity raise in 2018. The market will be flooded with marijuana by 2019 and we don’t think producers will blindly keep adding supply if the economics are challenged.

APHRIA GROWTH CAPACITY BY YEAR

International Expansion

Aphria purchased Nuuvera in late January 2018. Nuuvera specializes in exporting Canadian marijuana throughout the world and will provide a complementary sales channel for Aphria’s domestic marijuana supply. In the following analysis we have only included international deals that increase Aphria’s capacity abroad or demand for exports of marijuana grown in Canada. Distribution deals have been excluded because they will not help alleviate the coming marijuana oversupply in Canada.

Italy

Nuuvera is one of nine companies with a license to import medical marijuana into Italy. Medical marijuana demand in Italy could grow to 90,000 kg over time, but for now the Italian government only allows imports of 100 kg per year per license (less than 1% of Aphria’s capacity). Only the military is allowed to grow marijuana domestically and with no comprehensive national regulations around medical marijuana supply, efforts to satisfy underserved Italian medical patients have failed so far.

Africa

Nuuvera signed an offtake deal with Verve Dynamics of Lesotho to buy 3,000 kg of that company’s supply for distribution in Africa or elsewhere. This deal will not increase demand for Canadian growth marijuana or international capacity.

Germany

Nuuvera, subsidiary of Aphria, is a finalist in a government tender to grow up to 6,600kg domestically to supply the German market by 2022. Nuuvera also signed an agreement with a German pharmacy to export 1,200 kg of Canadian marijuana to drug stores in Germany.

Australia

Aphria owns 25% of Althea Pty an Australian importer of medical marijuana. Australian demand for medical marijuana could reach 38,000 kg a year longer term, but even if Aphria captures a third of the market and buys out the rest of Althea, exports to Australia will only be 6% of capacity.

International Growth May Disappoint

Throughout history, when governments or companies want to gain corporate knowledge from competitors the easiest way to do so is to form a joint venture or consulting arrangement and then terminate the relationship once you have absorbed all the intellectual property of the other party. China has basically institutionalized this strategy of knowledge transfer.

Aphria is insulating itself from these risks through its direct ownership of international subsidiaries, which is a positive compared to larger peers.

Keeping seed strains, growing techniques and other corporate knowledge in-house will increase Aphria’s ability to differentiate its product in international markets. Risks remain as international governments commit to cultivate domestic sources of supply and international producers publicly state a desire to import marijuana only until domestic production can be built.

We worry that long term, meaningful international demand for Canadian marijuana may not materialize to the extent expected by the market, leading to much lower retail prices in Canada.

AS IT STANDS TODAY, APHRIA’S INTERNATIONAL PRODUCTION CAPACITY WILL ONLY BE 18,000 KG IN THREE YEARS (7% GROWTH ON TOTAL VOLUMES). NOT THE EXPLOSIVE GROWTH INVESTORS ARE CURRENTLY ANTICIPATING.

Valuation

To value Aphria we look at the steady state cashflow potential of the business, which for our purposes is 2022 when the Canadian market for flower will be largely mature. We then apply a steady state Enterprise Value (EV) to EBITDA multiple to arrive at the future value of the company. Taking the future value and discounting it back to today gives us the present value of Aphria shares.

Enterprise Value (EV)

The value of the entire company taking into account any debt outstanding and cash in the bank. Calculated as the total value of stock outstanding plus the value of debt minus cash in the bank.

EBITDA

Earnings before interest on debt, taxes and depreciation. Similar to the cashflow of the business.

Present Value

To the average person a dollar in your pocket today is worth more to you than a dollar in your pocket one year from now. Therefore the future, higher value of a company needs to be adjusted back to its present value to see what it is worth to us TODAY.

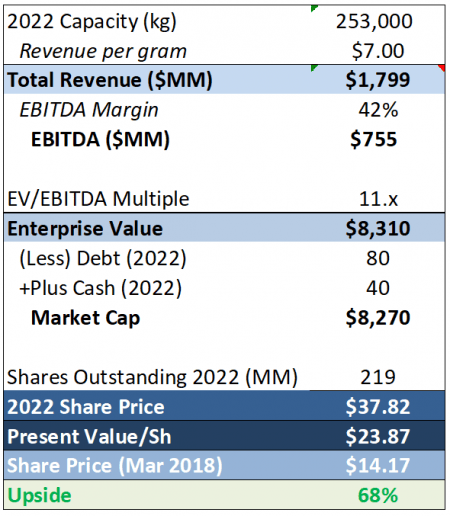

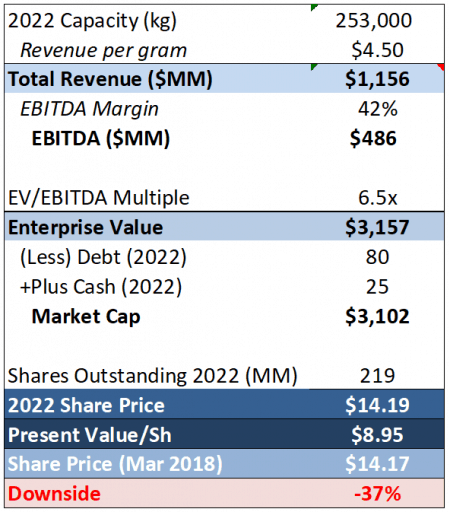

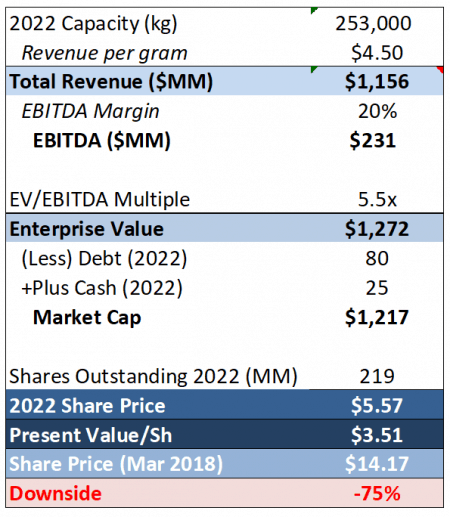

USING A PROBABILITY WEIGHTED AVERAGE OF OUR UPSIDE, DOWNSIDE AND BASE CASE SCENARIOS, THE VALUE OF APHRIA TODAY IS $8.00/SH.

UPSIDE CASE (5% probability)

The upside case looks at what the stock is worth if absolutely everything goes right. Under this scenario, we assume Canadian supply is only adequate to meet growing demand and producers are able to maintain prices through successful branding, new product R&D and other means. The stocks trade in line with global tobacco producers, who have significant pricing power and concentrated market share.

$7/gram retail price, 42% EBITDA margins, capacity in line with management guidance and an 11x EV/EBITDA multiple.

BASE CASE (60% probability)

Canada is flooded with new legal supply and a lack of barriers to entry causes higher cost producers to go out of business, balancing supply with demand. The stocks still manage to maintain margins in line with global tobacco producers through innovation and lower production costs. Stocks trade at the high end of commodity multiples.

$4.50/gram retail prices, 42% EBITDA margins, capacity in line with management guidance and a 6.5x EV/EBITDA multiple.

DOWNSIDE CASE (35% probability)

Canada is flooded with new legal supply and a lack of barriers to entry causes higher cost producers to go out of business, balancing supply with demand. New sources of supply abroad shut down any opportunity to export excess marijuana produced in Canada. Government control over distribution and retail and inflexible excise taxes lead to smaller margins for the producers as prices fall. Stocks trade at the midpoint of commodity multiples.

$4.50/gram retail price, 20% EBITDA margins, capacity in line with management guidance and a 5.5x EV/EBITDA multiple.

Read Up in Smoke – In this deep dive macro analysis of the Canadian marijuana sector, Grizzle lays bare all the inconvenient truths of this highly overvalued sector.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.